The local mayoral race will be re-held, but time isn’t on the president’s side.

By Xander Snyder

Despite winning a favorable ruling from the country’s electoral authority, the pressure seems to be mounting on Turkey’s ruling party. On Monday, Turkey’s High Election Council canceled the results of Istanbul’s March 31 mayoral election, which a candidate from the opposition Republican People’s Party had won by a narrow margin. Initially, President Recep Tayyip Erdogan said he and his Justice and Development Party, or AKP, would accept the results of the election. But they quickly changed their minds and challenged the results, claiming voting irregularities, including that individuals with links to cleric Fethullah Gulen, whom Erdogan blames for planning the 2016 coup attempt, had nullified the ballots of up to 15,000 voters. The electoral authority has ordered that the election be rerun on June 23.

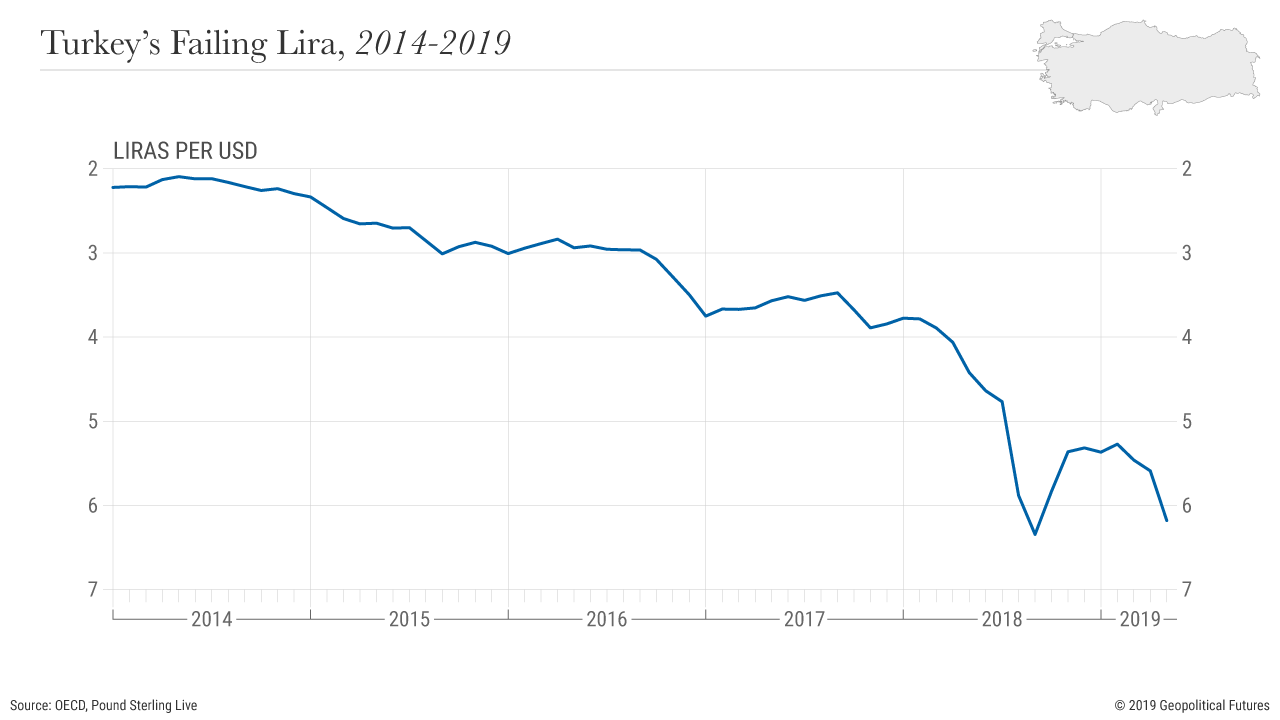

Following the announcement, Turkey’s lira plunged in value, falling to 6.16 liras to the dollar on Tuesday, its lowest point since October 2018. Currency pairs tend to move on even the slightest bit of good or bad news, so one could easily draw the conclusion that the falling lira is a result of the election controversy. But the fundamentals of the Turkish economy that make the lira vulnerable in the first place – namely, high external debt and low foreign reserves – have remained relatively unchanged for a while.

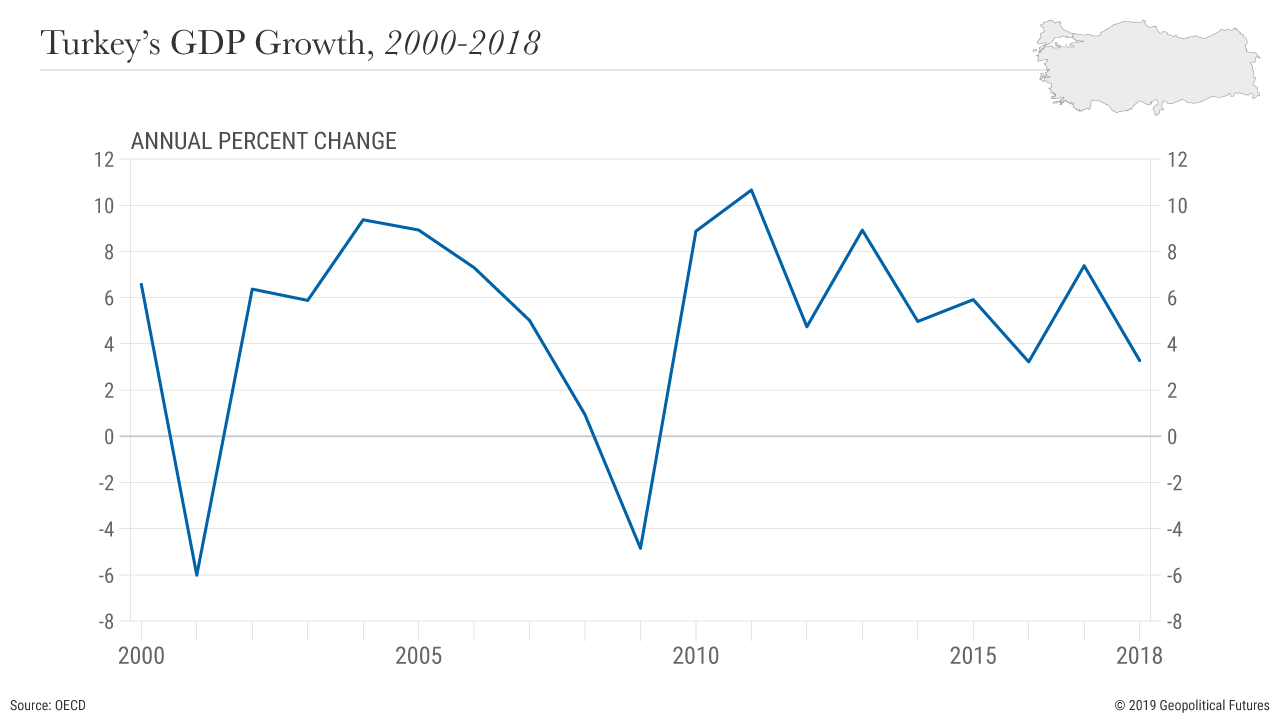

For the most part, Turkey’s economy has performed fairly well under the AKP’s watch. But the country’s relatively high growth rates in recent years have been fueled by debt, much of which was borrowed abroad because of the lack of domestic investment capital. Foreign currency-denominated debt is risky because, if the value of the domestic currency falls, foreign debt becomes costlier to pay off. In such scenarios, foreign currency reserves become very important; they can be used to service foreign debt and avoid using the weaker national currency, making debt payments relatively less expensive.

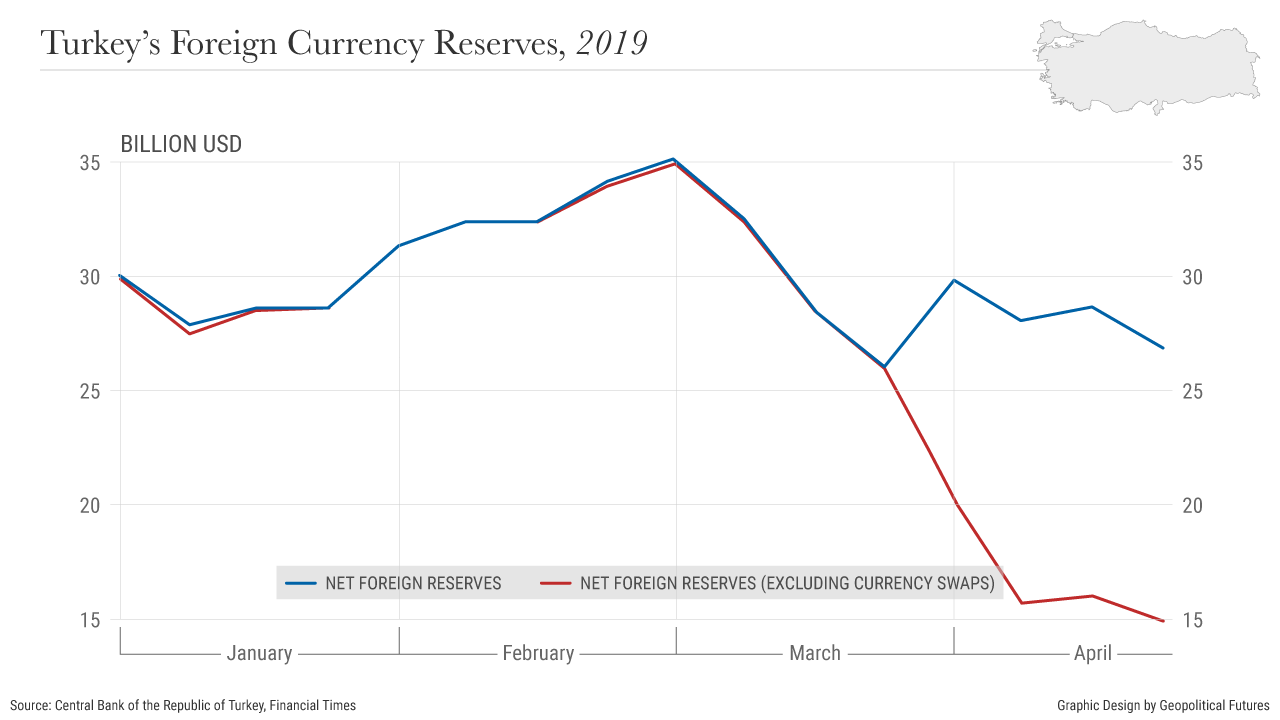

Turkey, however, has not been particularly good at accruing and holding on to foreign reserves. Turkey’s gross foreign reserve assets (excluding gold) have declined over the past five years from a peak of around $110 billion to about $73 billion in late April. But Turkey’s net foreign reserves are only roughly $26 billion. Even this figure, however, is somewhat inflated. In late March, to avoid a potential selloff of the lira in the run-up to municipal elections, Turkey started borrowing foreign currency using dollar-lira swaps. Essentially, Turkey’s central bank’s swap facility provided more liras to investors in exchange for dollars, which, on paper, made Turkey’s net reserves position appear better than it actually was. The problem, of course, is that Turkey doesn’t actually own those dollars – they are just on loan. Taking this into account, Turkey’s actual net reserves are closer to $11 billion. In 2018, Turkey’s imports totaled approximately $223 billion, or $19 billion per month on average, which means its net reserves could cover less than one month’s worth of imports.

Turkey’s central bank has argued that gross reserves, rather than net reserves, are a better indicator of capital adequacy – the minimum amount of reserves a country needs to have on hand – because there’s no generally accepted rule for what liabilities net figures should account for. Considering Turkey’s total external debt burden was roughly $448 billion at the end of 2018, its gross reserves cover about 16 percent of its total external debt. If you factor in Turkey’s approximately $20 billion in gold reserves, the coverage ratio rises to nearly 21 percent. But it plummets to just 2.5 percent when calculated using net reserves, excluding the short-term borrowed dollars. Should Turkey need to buy liras to prop up the currency, its coverage ratio would decline even further.

Now Turkey is stuck with a menu of bad options to try to solve its economic problems. One option is to continue with the prior policy – keep interest rates as low as possible and access to credit plentiful. Cheap credit helped fuel Turkey’s economy in the past, so it could potentially help keep growth rates up while the government kicks the can of foreign debt down the road.

However, Turkey’s economy contracted in the third and fourth quarters of 2018, and its inflation reached nearly 20 percent in April, indicating that the country may no longer be able to hold off the negative consequences of debt-fueled growth. The second option is to raise rates and attempt to generate organic growth that’s not dependent on foreign borrowing.

Both of these paths carry political consequences. Continuing on the current path could mean higher inflation, which would increase the cost of living and could motivate people to turn away from the AKP. Attempting to fix Turkey’s structural economic problems – in part by raising rates, encouraging greater domestic savings and accumulating more domestic capital with which to lend – would probably prolong Turkey’s economic slowdown and create serious economic pain for many average Turks. Both options could hurt the AKP’s popularity ratings, but the party doesn’t appear to have any better alternatives other than simply managing the fallout from the crisis, which isn’t a particularly inspiring political platform.

The AKP is clearly aware that its management of Turkey’s economic problems could threaten its hold on political power. If the AKP felt secure politically, then losing a local election wouldn’t be a major concern. But knowing that things will only get harder as time goes on, it has to take each vote seriously. Pushing for a rerun of the Istanbul elections, therefore, is, more than anything, an admission that time is not on the AKP’s side.

Xander Snyder is an analyst at Geopolitical Futures. He has a diverse theoretical and practical background in economics, finance and entrepreneurship. As an investment banker, Mr. Snyder worked in corporate debt origination and later in a consumer-retail industry group at Guggenheim Securities, participating in transactions ranging from mergers and acquisitions, equity and debt capital raises, spin-offs and split-offs to principal investing and fairness opinions. He has worked on more than $4 billion worth of transactions. He subsequently co-founded and served as CFO for Persistent Efficiency, an energy efficiency company that used cutting-edge technology to create a new type of electricity sensor for circuit breakers and related data services. In his role, he was responsible for raising more than $1.5 million in seed capital and presented to some 70 venture capital and angel investors in the process. He also signed four Fortune 500 companies as customers, managed all aspects of company accounting, budgeting and cash flow, investor relations, and supply chain and inventory management. In addition to setting corporate strategy, he helped grow the company from two people to a 12-person team. As an independent financial consultant, Mr. Snyder wrote an economics publication for a financial firm that went out to more than 10,000 individuals and assisted in deal sourcing for a real estate private equity fund. He is an active real estate investor and an occasional angel investor. Mr. Snyder received his bachelor’s degree, summa cum laude, in economics and classical music composition from Cornell University.

Following the announcement, Turkey’s lira plunged in value, falling to 6.16 liras to the dollar on Tuesday, its lowest point since October 2018. Currency pairs tend to move on even the slightest bit of good or bad news, so one could easily draw the conclusion that the falling lira is a result of the election controversy. But the fundamentals of the Turkish economy that make the lira vulnerable in the first place – namely, high external debt and low foreign reserves – have remained relatively unchanged for a while.

For the most part, Turkey’s economy has performed fairly well under the AKP’s watch. But the country’s relatively high growth rates in recent years have been fueled by debt, much of which was borrowed abroad because of the lack of domestic investment capital. Foreign currency-denominated debt is risky because, if the value of the domestic currency falls, foreign debt becomes costlier to pay off. In such scenarios, foreign currency reserves become very important; they can be used to service foreign debt and avoid using the weaker national currency, making debt payments relatively less expensive.

Turkey, however, has not been particularly good at accruing and holding on to foreign reserves. Turkey’s gross foreign reserve assets (excluding gold) have declined over the past five years from a peak of around $110 billion to about $73 billion in late April. But Turkey’s net foreign reserves are only roughly $26 billion. Even this figure, however, is somewhat inflated. In late March, to avoid a potential selloff of the lira in the run-up to municipal elections, Turkey started borrowing foreign currency using dollar-lira swaps. Essentially, Turkey’s central bank’s swap facility provided more liras to investors in exchange for dollars, which, on paper, made Turkey’s net reserves position appear better than it actually was. The problem, of course, is that Turkey doesn’t actually own those dollars – they are just on loan. Taking this into account, Turkey’s actual net reserves are closer to $11 billion. In 2018, Turkey’s imports totaled approximately $223 billion, or $19 billion per month on average, which means its net reserves could cover less than one month’s worth of imports.

Turkey’s central bank has argued that gross reserves, rather than net reserves, are a better indicator of capital adequacy – the minimum amount of reserves a country needs to have on hand – because there’s no generally accepted rule for what liabilities net figures should account for. Considering Turkey’s total external debt burden was roughly $448 billion at the end of 2018, its gross reserves cover about 16 percent of its total external debt. If you factor in Turkey’s approximately $20 billion in gold reserves, the coverage ratio rises to nearly 21 percent. But it plummets to just 2.5 percent when calculated using net reserves, excluding the short-term borrowed dollars. Should Turkey need to buy liras to prop up the currency, its coverage ratio would decline even further.

Now Turkey is stuck with a menu of bad options to try to solve its economic problems. One option is to continue with the prior policy – keep interest rates as low as possible and access to credit plentiful. Cheap credit helped fuel Turkey’s economy in the past, so it could potentially help keep growth rates up while the government kicks the can of foreign debt down the road.

However, Turkey’s economy contracted in the third and fourth quarters of 2018, and its inflation reached nearly 20 percent in April, indicating that the country may no longer be able to hold off the negative consequences of debt-fueled growth. The second option is to raise rates and attempt to generate organic growth that’s not dependent on foreign borrowing.

Both of these paths carry political consequences. Continuing on the current path could mean higher inflation, which would increase the cost of living and could motivate people to turn away from the AKP. Attempting to fix Turkey’s structural economic problems – in part by raising rates, encouraging greater domestic savings and accumulating more domestic capital with which to lend – would probably prolong Turkey’s economic slowdown and create serious economic pain for many average Turks. Both options could hurt the AKP’s popularity ratings, but the party doesn’t appear to have any better alternatives other than simply managing the fallout from the crisis, which isn’t a particularly inspiring political platform.

The AKP is clearly aware that its management of Turkey’s economic problems could threaten its hold on political power. If the AKP felt secure politically, then losing a local election wouldn’t be a major concern. But knowing that things will only get harder as time goes on, it has to take each vote seriously. Pushing for a rerun of the Istanbul elections, therefore, is, more than anything, an admission that time is not on the AKP’s side.

Xander Snyder is an analyst at Geopolitical Futures. He has a diverse theoretical and practical background in economics, finance and entrepreneurship. As an investment banker, Mr. Snyder worked in corporate debt origination and later in a consumer-retail industry group at Guggenheim Securities, participating in transactions ranging from mergers and acquisitions, equity and debt capital raises, spin-offs and split-offs to principal investing and fairness opinions. He has worked on more than $4 billion worth of transactions. He subsequently co-founded and served as CFO for Persistent Efficiency, an energy efficiency company that used cutting-edge technology to create a new type of electricity sensor for circuit breakers and related data services. In his role, he was responsible for raising more than $1.5 million in seed capital and presented to some 70 venture capital and angel investors in the process. He also signed four Fortune 500 companies as customers, managed all aspects of company accounting, budgeting and cash flow, investor relations, and supply chain and inventory management. In addition to setting corporate strategy, he helped grow the company from two people to a 12-person team. As an independent financial consultant, Mr. Snyder wrote an economics publication for a financial firm that went out to more than 10,000 individuals and assisted in deal sourcing for a real estate private equity fund. He is an active real estate investor and an occasional angel investor. Mr. Snyder received his bachelor’s degree, summa cum laude, in economics and classical music composition from Cornell University.

0 comments:

Publicar un comentario