Rate Cuts Are Coming

by: The Heisenberg

Summary

- Friday's disappointing jobs report in the US likely seals the deal for Fed cuts.

- Markets now see Fed easing from July onward, as the latest data is interpreted as "confirmation" that the US economy is finally decelerating.

- With market pricing and Wall Street now "doved-up" to the max, Jerome Powell will need to cut next month, if not sooner.

If you wanted to, you could point to news that the US will delay the imposition of higher tariff rates on some Chinese products to June 15 as a catalyst for the Friday morning surge in equities (SPY), but it's probably safe to assume that rate cut bets are again playing a big role in propelling stocks.

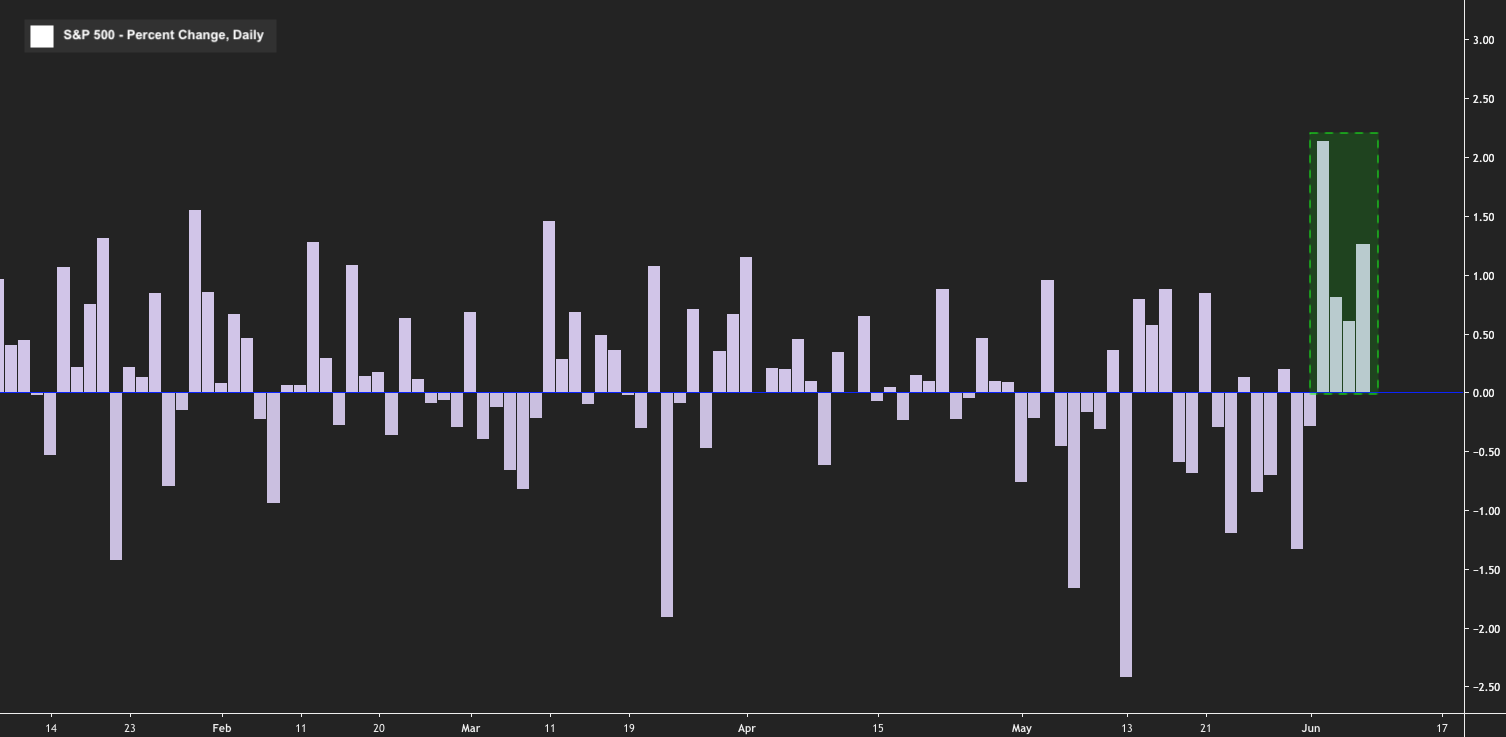

In the wake of the disappointing May payrolls report (top pane in the visual), the market is priced for cuts starting in July - as in, starting next month.

(Heisenberg)

(Heisenberg)

Pressure on Powell to get out ahead of things by, at the very least, signaling imminent easing at the June meeting, is growing. 2-year yields plunged 11bp on Friday morning and are on track for a fifth straight week of declines.

Note the chart in the bottom pane of the visual. As the legend indicates, the purple line is the US 2-year yield minus the funds rate. Both Goldman and David Rosenberg referenced that chart this week in suggesting that rate cuts are probably just around the corner.

"The 2-year rates minus Fed Fund Rate is now close to -40bp and historically from this level the Fed has usually delivered a cut in the following months," Goldman wrote Monday. "Surely if Jerome Powell is a 'markets guy' he’ll eventually understand that when the 2-year T-note yield drifts more than 50 bps below the funds rate, nasty things tend to happen," Rosenberg tweeted, adding that it’s "time to take the blinders off."

To the extent the Fed did in fact have its "blinders" on, the May payrolls report may be the last straw for hawkish holdouts. In addition to the grievous miss on the headline print (75k was below even the lowest estimate from 77 economists) both March and April saw sizable downward revisions. Meanwhile, wage growth came in cooler-than-expected (again), bolstering the subdued inflation narrative.

I'm writing this on-the-fly, mid-morning, so things could always take a turn for the worst (especially considering how volatile the trade headlines have been recently), but as of 11:30 AM in New York, stocks are on track for another blockbuster session. This is quite something considering how dour the outlook is on trade:

(Heisenberg)

(Heisenberg)

In addition to what markets are "saying" (read: pricing), all of the early commentary on the jobs report underscores the rate cut narrative.

"For the Fed, today’s report makes a cut more likely, and supports our view that the trade tensions will ultimately slow growth enough for the Fed to respond in September and December with cuts," BofA said. The bank maintains that June is "too early" for Powell to move and says the Fed may want to "wait after the G-20 meetings to get greater clarity on the current trade negotiations between China and Mexico before altering their outlook for the economy and the path of policy."

That underscores a point I've made both here and on my site time and again over the past several weeks (see here for instance). The Fed is in a bind when it comes to cutting rates amid the trade escalations. Easing policy could very well embolden the Trump administration to pursue a harder line with China, thereby raising the odds of further escalations. Overnight on Friday, PBoC Governor Yi Gang, in an exclusive interview with Bloomberg, said Chinese monetary policy has "tremendous" room to respond to any negative developments. Trump last month called for the Fed to "match" the PBoC. If Powell were to cut rates in June or July, it could potentially be seen as the Fed answering that call.

Although Goldman has yet to adopt rate cuts as their base case (as of this writing, anyway), the bank did acknowledge that the jobs report raises the odds of easing. "The risks of Fed rate cuts have clearly increased, and the outcome of trade negotiations will also be a central consideration," the bank said.

For their part, Credit Suisse (which sees a rate cut at the July meeting) drove the point home on Friday morning. "A Fed cut in June is still unlikely, in our view, but this report increases the chance that we see a clear dovish shift at their upcoming meeting, followed by a rate cut on July 31st," the bank said, in a short note.

Obviously, there is a clear risk that the Fed cannot live up to market expectations for easing. Here's Nomura's Charlie McElligott from a lengthy Friday morning missive:

[There's] a meaningful chance that even if the Fed were to move forward with a preemptive 'insurance cut' of up to 50bps in the next 1-3 months, the market implied potential for 4 cuts before the end of next year looks like a 'stretch,' as it would potentially require the worst case scenario double-whammy of 1) Tariffs and 2) Recession.

Charlie is probably right (and I should note that his Friday piece is an in-depth look at what's behind the "incessant and almost price-insensitive buying of ED$" on the highs). Indeed, it's entirely possible that even if the Mexico standoff ends in an agreement that averts tariffs, the damage to sentiment is done. The fact that the US is increasingly prone to seemingly random tariff escalations heightens fears about the potential for similar action against Europe (Goldman was out this week assigning a 40% probability to auto tariffs at some point) and further tension with China. That, in turn, will likely weigh on survey data and, potentially, hiring. Remember, the May jobs report doesn't capture the Mexico tariff spat.

Going forward, it is all about whether the Fed can engineer a soft landing in the face of what can now be quite appropriately described as wholly unpredictable trade policy and a decelerating US economy.

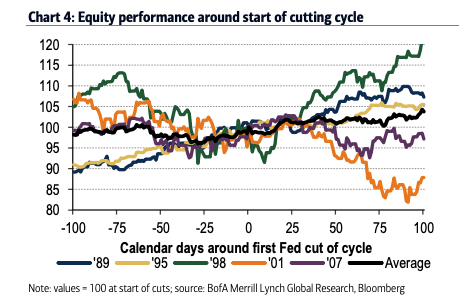

When you think about all of this in the context of what, as of Friday morning anyway, is shaping up to be the best week for US stocks since November, bear in mind that, to quote a BofA note dated Thursday, "Fed cutting cycles are not usually preceded by a sharp equity market selloff [and] in fact, the S&P 500 on average tends to rise modestly into Fed cutting cycles."

(BofA)

Food for thought.

0 comments:

Publicar un comentario