Markets predictions: 2019 to bring new level of uncertainty

Strategists give their forecasts on what could happen to equities, gold, cash and securities

Robin Wigglesworth

Danish physicist and Nobel laureate Niels Bohr famously quipped that “prediction is very difficult, especially if it’s about the future”. But as 2018 enters its final stretch, Wall Street’s analysts are once again dusting off their crystal balls and attempting to map out what the coming year will look like.

An always tricky task is now nearly impossible. Economists and analysts are actually reasonably good at getting the general direction correct, but awful at anticipating turning points. And as 2018 showed — with virtually every major asset class heading for a loss — markets appear to be entering a new, more uncertain phase. Is 2019 the year when the post-crisis bull run falls completely apart?

“All good things eventually come to an end. But when? Answering this question represents the fundamental 2019 investment challenge for portfolio managers,” David Kostin, chief US equity strategist at Goldman Sachs, wrote in his annual outlook.

Big picture: the median forecast of strategists polled by Bloomberg indicates the US economy will grow 2.6 per cent in 2019, while the S&P 500 will end the year at 3,090 points, with the 10-year Treasury yield at 3.44 per cent. Pretty much everyone expects the dollar to weaken next year, as the Fed interest rate cycle peaks.

But diving into the details of the outlook reports, there are some more interesting predictions. Here are some of them.

Return of the bear

Most analysts, even bearish ones such as Morgan Stanley’s Mike Wilson, think the S&P 500 will end 2019 higher than its current level. But Société Générale’s 2,400-point end-2019 prediction — and for a recession by the first half of 2020 — stands out as the most negative one by far.

It implies another 10 per cent drop from the current level, which would mean a bear market for US equities (typically defined as a 20 per cent drop from the recent high). “We expect a more restrictive monetary policy to push equity valuations lower, while political gridlock and trade tensions will likely be a source of volatility,” SocGen said in its outlook, fittingly illustrated by a waving grizzly bear.

But SocGen is also gloomy on European equities — eyeing another 8 per cent drop to take the Euro Stoxx 50 into a bear market — thinks Japanese equities will tread water and forecasts that the FTSE 100 will tumble by another 14 per cent.

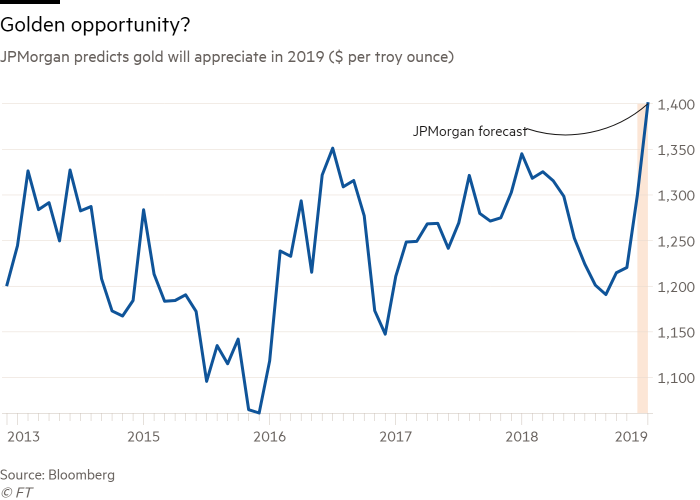

Gold regains its glitter?

Gold bugs have had a frustrating year, as a splurge of Treasury issuance has failed to shake faith in the greenback, and a the strong economy and the Fed’s rate increases have sucked in money from abroad. This has led gold to shed almost 5 per cent of its dollar value in 2018 to trade at about $1,240 per troy ounce.

But both JPMorgan and Bank of America reckon a renaissance is coming, as the US central bank slows its rate increases and financing the US deficit becomes more challenging. BofA sees gold appreciating a modest 5 per cent, but JPMorgan predicts a juicier 15 per cent return, “as US real rates peak and focus turns to financing the US’s twin deficits when the Fed cycle is near an end”.

Inflation in the nation

Most analysts expect US inflation to stay subdued in 2019. The core “personal consumption expenditures” price index — the Fed’s preferred inflation measure — is expected to tick up from 1.9 per cent to 2.1 per cent next year, but some strategists fret that this is complacent.

Macquarie expects core PCE to accelerate a touch faster, to 2.2 per cent in 2019, and warns that even this may be too low an estimate, given the danger of tariff costs being passed on to consumers, a weaker dollar, rising natural gas prices, spendthrift fiscal policy and the labour market reaching a “pinch point” that causes wages to shoot higher.

Given how sensitive financial markets have proven to any hint of accelerating inflation this year, this could be the still-unlikely but most dangerous risk to watch in 2019.

A value renaissance?

Cheap, stolid “value” stocks have been left in the dust by racier “growth” stocks since the financial crisis, but Morgan Stanley reckons that 2019 will see “a major leadership change occurring from growth to value which could be more long-lasting than most appreciate”, pointing to their relatively low prices and how growth stocks are more sensitive to higher bond yields.

After a long bout of underperformance, which by some measures stretches back decades, this is an out-of-consensus call by Morgan Stanley’s analysts. As they noted in a follow-up report: “While pushback wasn’t overwhelming, clients didn’t exactly embrace our views, with the least support for value over growth and international stocks outperforming the US.”

Securitised shocker

The alphabet soup of securitised bonds has done fairly well in 2018, especially products such as collateralised loan obligations and floating-rate asset-backed securities, which benefit from rising Fed interest rates.

However, BofA reckons that the poor performance of “agency” mortgage-backed securities created by Fannie Mae or Freddie Mac — which have faced headwinds from the Fed shedding MBS from its balance sheet — could be a “harbinger of what’s to come in other securitised sectors in 2019”.

“Chances are good that 2019 ultimately sees a major blowout in securitised products spreads,” the bank’s analysts wrote in their outlook. “The key driving factors we see are macro in nature: continued monetary policy tightening, in the form of rate hikes and accelerated balance sheet wind down, further trade war escalation, fading fiscal stimulus and slowing home price growth due to affordability constraints.”

King Cash

Cash has been one of 2018’s surprise performers, with the returns from Treasury bills beating broad bonds and equity and commodity indices — an exceptionally unusual occurrence. Many investors point out that this happening two years in a row is almost unheard of, but JPMorgan warns that they should gird themselves for disappointment once again.

JPMorgan’s chief cross-asset strategist John Normand sees returns of plus or minus 1 per cent for most asset classes, but thinks rising US interest rates will mean that cash will return 2.8 per cent in 2019. Goldman Sachs predicts cash returns will hit 3 per cent. Rate increases from all developed country central banks will also lift global cash returns from zero in 2018 to 1 per cent next year, JPMorgan forecasts.

However, that will weigh heavily on developed market bonds, and inflict another 2.4 per cent loss on investors. That would be the first consecutive yearly loss for bonds since modern bond benchmarks began in the early 1970s.

Size matters

Smaller US company stocks have been pummelled lately, tumbling more than 15 per cent since their summer high to underperform the “large-cap” S&P 500, despite being in theory more immune to any deepening trade wars.

Deutsche Bank’s chief US strategist Binky Chadha reckons this is way overdone, pointing out that small-caps are now pricing in a sharp US economic slowdown and are unusually cheap compared with large-caps. Given the relative positioning — traders are now net short the Russell 2000 small-caps index but long the S&P 500 — he recommends investors look for opportunities there instead.

0 comments:

Publicar un comentario