Flight Risk

by: The Heisenberg

- I found some great new color that expands on a popular piece published here over the weekend.

- This is a followup to my post on the newfound allure of USD "cash" and the effect that has on multi-asset managers' appetite for risk.

- This is especially relevant going into a week that looks set to feature the most dramatic escalation yet in the trade war between Washington and Beijing.

- At a higher level, though, it's important to understand how the rise of "cash" influences the decision calculus for stewards of capital.

- This is a followup to my post on the newfound allure of USD "cash" and the effect that has on multi-asset managers' appetite for risk.

- This is especially relevant going into a week that looks set to feature the most dramatic escalation yet in the trade war between Washington and Beijing.

- At a higher level, though, it's important to understand how the rise of "cash" influences the decision calculus for stewards of capital.

With inflows drying up and possibly continuing to do so as the rates cycle between US and Europe pushes money out of the latter, liquidity will likely become more challenging.

That's from a BofAML note dated September 12 and it alludes to the same dynamic I described over the weekend in a post for this platform called "I Drink Your Milkshake".

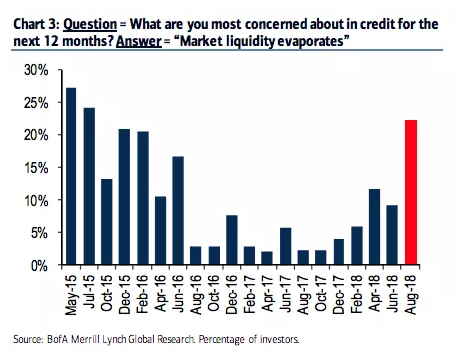

When BofAML asked European credit investors about the outlook for liquidity, the responses betrayed more than a little consternation. In fact, "market liquidity evaporates" was the number one concern for nearly a fourth of respondents, the highest percentage in more than three years.

(BofAML)

(BofAML)

In European credit, the buy-side is concerned about three things: 1) the idea that between the ECB winding down asset purchases and the sell-side being reluctant to lend its balance sheet thanks to the post-crisis regulatory regime, they'll be the only bid in the market for € IG and € HY, 2) deteriorating liquidity metrics (think low turnover and an inability to transact in size), and 3) the idea that higher rates on U.S. fixed income (and especially short-dated USD fixed income) will sap demand for lower-yielding and inherently riskier European debt.

There's a lengthy and important discussion to be had around points 1 and 2 (more on that here), but in the interest of sticking with the theme from my weekend "milkshake" post, I wanted to focus again on point 3.

For those who missed it, here is the key chart which shows yields on short-dated USD fixed income sitting at their highest levels since the crisis:

(Bloomberg)

(Bloomberg)

Basically, that's "cash", as it were.

The allure of USD cash yielding the most since the crisis in an environment where risks are multiplying is obviously high. You'll also note from the chart that you're getting more yield there than you are from the S&P (blue line).

The cloudier the outlook gets in terms of trade frictions, geopolitical risks and domestic political tensions ahead of the midterms, the more attractive that's going to look and the higher the potential for a "flight to safety" to manifest itself in demand for USD cash. This is something I talked about at length earlier this year in a post called "Ray Dalio And The 'Pretty Stupid Cash Holders'". In that post, I cited another BofAML note in which the bank suggested that cash could be a more desirable safe haven asset than 10Y Treasurys in risk-off episodes. Recall this excerpt from a note out earlier this year:

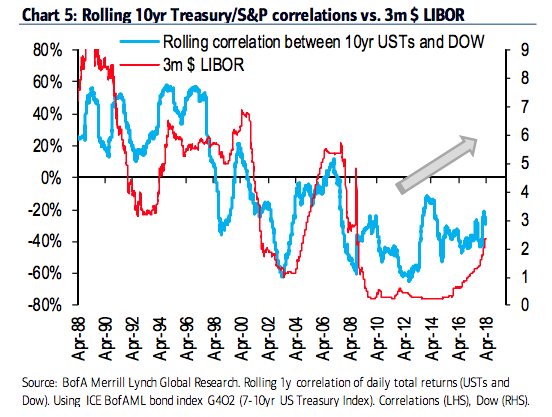

The typical haven characteristic of Treasury debt is being hindered by the appealing rates of return on cash in the US. Historically during periods of market turbulence, money would flow from risky assets (such as stocks) into US Treasury bonds. But with $ Libor at 2.36%, support for Treasury debt is diminishing (consider that 5yr Treasury yields are 2.84%). In other words, the rise of “cash” as an asset class is altering the traditional allocation decisions of multi-asset investors in times of market stress.

Chart 5 highlights this point. We show the rolling 1yr correlation between total returns on 10yr Treasury bonds and the total returns on stocks (daily returns). We overlay this with the evolution of 3m $LIBOR.

In other words, the rise of "cash" poses a "flight risk" (if you will), not just for emerging market assets (EEM) that are under siege from the surging dollar (UUP), and not just for European credit which looks less attractive as the price insensitive ECB bid wanes, but even for longer-dated US Treasurys (TLT), which could lose some of their appeal in risk-off environments if multi-asset investors decide they'd rather just hold USD cash equivalents.

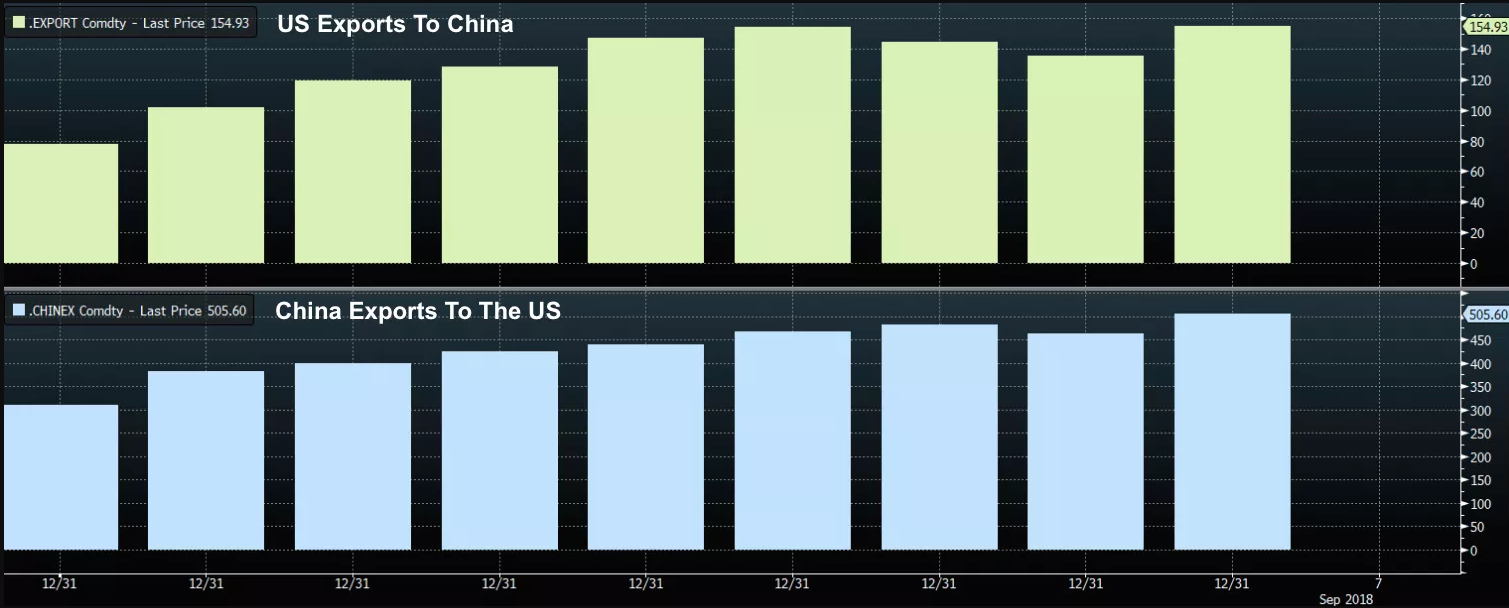

The headlines on the trade front are bad to start the week, and unequivocally so. Over the weekend, multiple outlets confirmed Bloomberg's Friday reporting that cited four sources as saying President Trump will move ahead with tariffs on another $200 billion in Chinese goods this week. According to the Wall Street Journal (out on Saturday), Beijing may decline Steve Mnuchin's offer to hold new trade talks in light of the latest expected escalation. On Monday, an editorial in the state-controlled Global Times said Beijing is "looking forward to a beautiful counter-attack and will keep increasing the pain felt by the U.S." Hours later, Trump tweeted that countries that "will not make fair deals will be 'Tariffed!'"

Obviously, none of that bodes particularly well for risk sentiment this week and you should also note that two Fridays ago, the President suggested that should China move ahead with the promised retaliation involving differentiated duties on $60 billion in U.S. goods, the USTR is prepared to slap levies on yet another $267 billion in Chinese products, taking the total amount of goods taxed to $500 billion or, more simply, the entirety of Chinese exports to the U.S.

(Bloomberg)

(Bloomberg)

I don't want to suggest that some kind of acute risk-off episode is imminent for U.S. stocks (SPY).

After all, U.S. equities have proven resilient this year in the face of trade tensions, even though international equities have most assuredly not (Chinese stocks hit a four-year low on Monday, for instance).

Rather, my point is that hopes of a deescalation on the trade front look to have been definitively dashed and on balance, that's bad for risk appetite. As risk appetite wanes, the appeal of higher rates on USD cash only grows. And wouldn't you know it, Goldman is out with a brand new piece that touches on this subject.

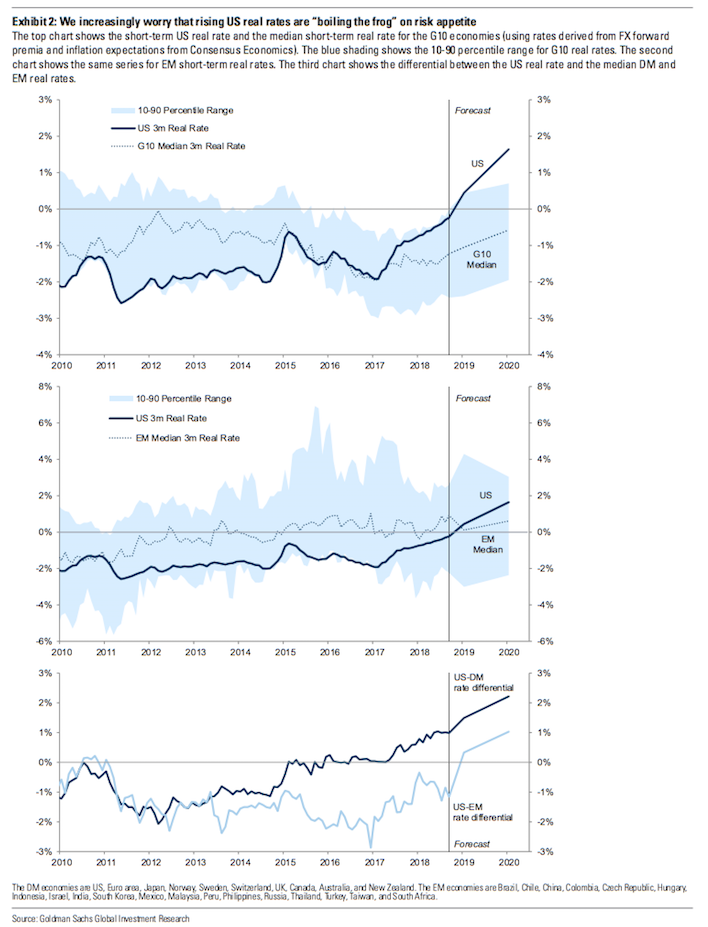

One of the arguments against my contention that USD cash is "attractive" is that real rates are still negative. My knee-jerk reaction to that argument is this: Since when have investors in the post-crisis world cared about negative rates on safe-haven assets? But Goldman has a more nuanced take. Consider the following three visuals from their note:

(Goldman)

(Goldman)

See the "problem" there? For one thing, real rates aren't going to be negative for long for USD cash equivalents and if Goldman's projections are correct, not only will they be comfortably positive going forward, they will be markedly higher than median real rates in G10 and EM.

Here's Goldman (and this is truncated):

Exhibit 2 shows that this divergence in real rates has been brewing for some time, but until recently, its impact on risk assets was offset by mitigating factors. Exhibit 2 also shows just how much this divergence in rates has grown over the past few years, and how much farther we expect it to go. For much of the early post-crisis era, US policy rates (in real terms) were among the lowest in the world. It was only in 2017 that US real rates crossed the DM median. But rise they have, having already risen to the 90th percentile in DM. And according to our forecasts, the divergence in real rates will rise substantially over the next year and a half, with US rates rising relative to both DM and EM.

That is noteworthy to say the least. Don't let it be lost on you that if the U.S. economy continues to outperform global counterparts thereby forcing the Fed to remain hawkish and if the trade tensions finally do manifest themselves in higher consumer prices in the U.S. thus forcing the Fed to lean against an inflation overshoot, the gap shown in those visuals is likely to get larger.

Here's Goldman one more time:

The real rate of return available on “safe” US assets is rising, both in absolute terms and relative to non-US markets. As the rate of return on “cash” rises, the appeal of risky assets falls. The low level of real rates over most of the post-crisis period set a very low bar for risky assets. That bar is now rising, and as long as the US economy continues firing on all cylinders, the bar will continue to rise.

Again, you should think about this holistically. That is, if you want to stay ahead of the game from a big picture perspective, you need to think about the factors that influence the decision calculus of multi-asset managers and other stewards of capital.

If all you care about is where Apple (just to use a random, single-stock example) is going to trade six months from now, well then, obviously you care more about the rollout of new iPhones than you do anything mentioned above. If your investment horizon is "forever", well again, you probably don't care a whole lot about any of this other than maybe reconsidering whether it might make sense to increase your allocation to cash equivalents.

I assume most readers here fall somewhere in between on a scale where one end is labeled "I only care about my Apple shares" and the other end is labeled "my investment horizon is literally 'forever', so the only thing I care about is tweaking my allocation once every 15 years".

If you, like me, fall somewhere in the middle on that hypothetical continuum, then everything said above is pretty important from the perspective of understanding the rationale behind money potentially fleeing to a newly-attractive asset class (USD cash) that just happens to be the safest of all possible alternatives in an environment where the risks are multiplying.

0 comments:

Publicar un comentario