BoJ defies global move to roll back crisis-era stimulus

Global bonds rally as changes to Japan’s vast easing programme prove minor

Leo Lewis and Kana Inagaki in Tokyo and Emma Dunkley in Hong Kong

Haruhiko Kuroda, BoJ governor, said the decision would 'counter speculation . . . that the bank is heading towards an early exit or an increase in rates' © AFP

The Bank of Japan made clear it would not join the world’s other major central banks in rolling back crisis-era stimulus policies on Tuesday, announcing it would maintain “extremely low” interest rates for an extended period.

After being forced three times in a week to intervene to cap bond yields amid expectations policymakers would signal a willingness to tighten its easy money regime, the central bank instead declared it was strengthening the framework for “continuous powerful monetary easing”.

Reinforcing its commitment to its programme, the BoJ introduced a forward guidance for policy rates for the first time, saying that the extremely low levels would remain “for an extended period of time”.

“This will fully counter speculation among some market participants that the bank is heading towards an early exit or an increase in rates,” Haruhiko Kuroda, BoJ governor, said at a news conference in Tokyo.

Analysts agreed he had bought himself at least six to nine months before the market again began to speculate about further changes to the programme.

Having been on edge in the days leading up to Tuesday’s announcement, bond markets rallied during the Tokyo trading day, with the yield on Japan’s benchmark 10-year debt falling 5 basis points to 0.04 per cent. In the early European afternoon, the 10-year US Treasury yield declined 1.5bp to 2.9598 per cent and the equivalent German Bund was unchanged, yielding 0.452 per cent.

The yen weakened by as much as 0.5 per cent in the approach to the start of US trade, reaching ¥111.58 per dollar, a six-session nadir. Tokyo-listed banks fell, with the Topix closing down 0.8 per cent, the biggest decline among Asia-Pacific indicies. Banks led the selling, as hopes were dashed for more of a move away from ultra-loose monetary policy, which has hit profits in the financial sector.

The BoJ’s changes announced involved efforts to make its huge stimulus programme more flexible.

The bank repeated its pledge to continue to purchase bonds so that 10-year JGB yields remained “at around zero per cent”, though it added the line that “the yields may move upward and downward to some extent”. Mr Kuroda later revealed that the bank would allow the 10-year JGB yield to move up and down 0.2 percentage points around zero — an informal measure that doubled the previous flexibility.

Analysts were surprised that the BoJ’s forward guidance had a specific reference to uncertainties linked to the planned consumption tax increase next October.

“The phrasing around the forward statement is stronger than we expected. If you read the statement literally, it sounds as if the BoJ is saying they won’t raise rates until 2020,” said Masamichi Adachi, economist at JPMorgan in Tokyo.

The BoJ also said it would alter the balance of its ¥6tn ($54bn) per year exchange traded funds buying programme so that a much greater proportion was focused on ETFs that track the broader, market cap-weighted Topix index. The scale of its Topix-linked ETF purchases would rise from ¥2.7tn to ¥4.2tn per year, the bank said in its statement.

Inflation in Japan remains subdued with prices, excluding fresh food and energy, up only 0.2 per cent in June. That prompted the BoJ to lower its inflation forecasts on Tuesday, which predicted price rises of 1.6 per cent in the year to March 2021 compared with 1.8 per cent that it projected in April.

“The momentum toward achieving the price stability target of 2 per cent is maintained but is not yet sufficiently firm,” the BoJ said in a statement.

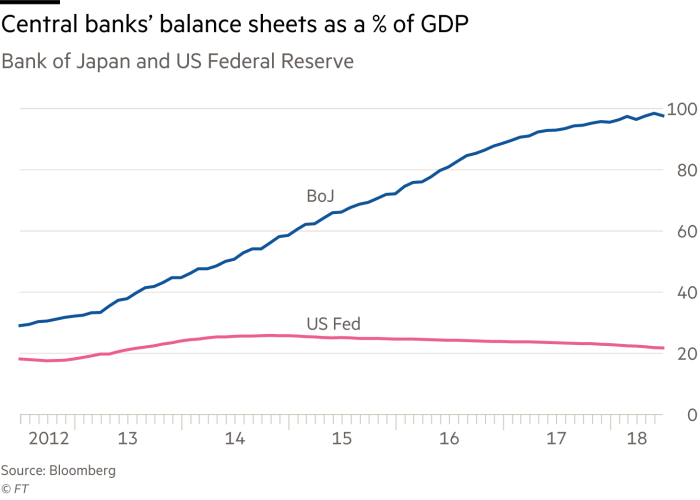

Analysts have warned that the BoJ’s vast monetary stimulus programme might not be sustainable over the long-term. The size of the BoJ’s balance sheet, as a percentage of GDP, is 98 per cent, compared with the US, which is just over 20 per cent.

Kerry Craig, a global market strategist at JPMorgan Asset Management, said: “Five years ago the BoJ said it would get inflation to 2 per cent, and it hasn’t happened, so there were some big questions on sustainability on how much more quantitative and qualitative easing they could do.”

He said the BoJ has created the forward guidance to show that it was committed to reaching its inflation target, to help keep the currency under control. “The longer these QE programmes run, the more likely central banks will run out of things to buy . . . if they tweak it to make it look sustainable, it buys them some credibility.”

Additional reporting by Edward White in Taipei

0 comments:

Publicar un comentario