And Now, Commence The Currency War

by: The Heisenberg

- On Friday, the trade war "evolved" into a currency war, although to a degree, those are two sides of the same coin.

- This is, frankly, all anyone was talking about to close the week, from mainstream media outlets, to analysts, to traders.

- I've included all manner of color from all manner of sources in an effort to shed more light on what's going on and how it's likely to affect markets.

- This is made all the more interesting coming as it does amid the G20 meeting.

On Thursday evening, I went to great lengths to explain the market significance of Donald Trump's landmark interview with CNBC's Joe Kernen, in which the President criticized Fed policy.

In that linked post, I outlined the three key reasons why Trump is concerned about the prospect of further rate hikes from Jerome Powell. Those three reasons are:

- Fed hikes imperil the stock market rally

- Fed hikes have the potential to slow down the U.S. economy

- Fed hikes drive the monetary policy divergence between the U.S. and its trade partners wider, thus pushing up the dollar and softening the blow of the tariffs on America's trade partners

Minutes after I finished that post, the PBoC weakened the yuan fixing by the most in over two years. The offshore yuan immediately plunged, trading through 6.83 to the dollar. The news rippled through markets and the headlines came in fast and furious.

There are times when I feel like it's necessary to convey to readers here that certain things are not open to interpretation and this is one of those times. That fixing was a signal to the Trump administration that China read his comments about the Fed as a sign that he not only understands the extent to which the policy divergence between the Fed and the PBoC is helping to weaken the yuan and thereby shield the Chinese economy from the tariffs, but also that Beijing believes Trump intends to try and ameliorate that situation by expressing his displeasure at Fed policy.

I detailed that extensively in my Thursday evening post, citing the following comment from Trump's CNBC interview:

China's currency is dropping like a rock [and] our currency is going up, and I have to tell you it puts us at a disadvantage [on trade].

On Friday morning, Trump made it explicit. The full version of his interview with CNBC aired and in it, the President said he is "ready to go to $500 billion", a reference to the prospect of imposing tariffs on everything China exports to the U.S. Those are his words, not mine.

Hours later, on Twitter, Trump said this in a tweet:

China and the European Union are manipulating their currencies and interest rates lower, while the U.S. is raising rates while the dollar's gets stronger and stronger with each passing day - taking away our big competitive edge.

Then, in a followup tweet, he said Fed hikes are threatening to derail U.S. economic momentum:

Tightening now hurts all that we have done.

There is nothing ambiguous about that, and it simply isn't possible to interpret it any other way. Donald Trump is advocating for a weaker dollar (UUP) and rate cuts in order to ensure that hawkish Fed policy doesn't end up softening the blow from the tariffs.

"Currency War Erupts, Threatening to Ripple Across Global Markets", the title of Bloomberg's feature story on Friday afternoon reads. Here are a couple of quick excerpts just to kind of drive home what I was trying to say on Thursday evening:

The currency war has arrived.

As the world’s two largest economies open up a new front in their increasingly acrimonious game of brinkmanship, the consequences could be dire -- and ripple far beyond the U.S. and Chinese currencies. Everything from equities to oil to emerging-market assets are in danger of becoming collateral damage as Beijing and Washington threaten the current global financial order.

Obviously, this has massive market implications and the timing couldn't be worse, coming as it does ahead of the G-20 meeting of finance ministers in Argentina. The following headline ran on the Terminal late Friday, and it speaks volumes:

FED'S POWELL DECLINES TO TAKE QUESTION AT G-20 IN BUENOS AIRES

On Friday morning, in the first post of the day over on my site, I used the following chart to illustrate how the offshore yuan was whipsawed by the CNBC interview on Thursday afternoon, the CNY fixing early Friday (in Asia), intervention on the part of a policy bank in China that was seen by traders selling dollars at 6.81 and the "$500 billion" comment CNBC ran some three hours prior to the open on Wall Street:

(Source: Heisenberg)

(Source: Heisenberg)

That was before the tweets excerpted above, which, once they hit, catalyzed a sharp selloff in the dollar.

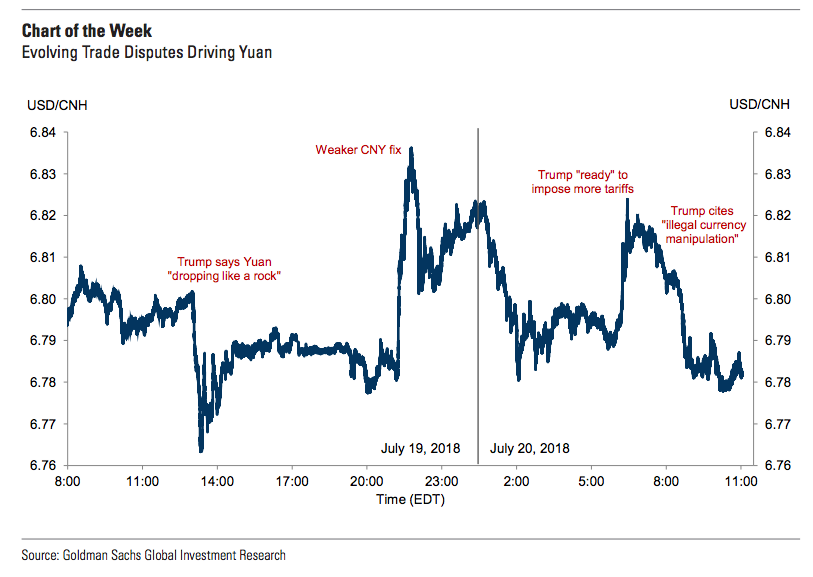

Want to see something amusing? Roughly six hours after I posted that chart, Goldman was out with a new note called "Trade war evolving into currency war" and it contains the following visual which they call "Chart of the week":

(Source: Goldman)

(Source: Goldman)

Does that look familiar to you? Yeah, it looked familiar to me too.

In any event, here's what Goldman's FX team had to say in the note about the market implications of everything that's happened over the past 24 hours:

The evolution of the conflict to more directly focus on FX would be consistent with how major trade disputes have played out in the past—often involving negotiated Dollar weakness—as well as the Administration’s goal of reducing the US trade deficit. We do not think the President’s comments on the Fed affect the outlook for US monetary policy. However, they could impact how other countries are approaching trade disputes, either by bringing them to the negotiating table or affecting currency policy directly. For FX markets, we think the latest developments imply: (i) that the correlation between trade tensions and FX will change, such that an escalating conflict may not result in consistent USD gains; (ii) that other reserve currencies, particularly EUR and JPY, should find support, and (iii) that CNY will be more stable, as the US could interpret further depreciation as a form of retaliation.

Other analysts had varying takes, but they all have one thing in common: skepticism about the durability of the dollar rally in light of Trump's comments and now explicit rebuke of further rate hikes from Jerome Powell. Here's one example from BNP:

Trump’s recent comments about a strong USD putting the US at a disadvantage and accusing China and the European Union of currency manipulation suggest it will be more difficult for the USD to extend gains as trade tensions escalate, unless US officials at the G20 meeting this weekend attempt to dial back his comments and reiterate the United States’ strong USD policy.

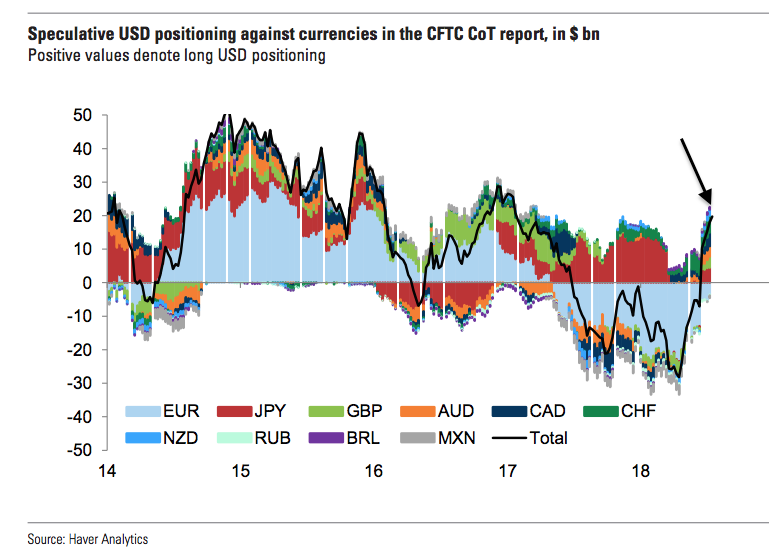

This is made all the more interesting by that fact that in the week through Tuesday, net long positioning in the dollar rose for a fifth straight week to nearly $20 billion:

(Goldman)

(Goldman)

Late Friday, CNBC reported that according to a White House official, the President is "worried" about the prospect of the Fed raising rates twice more in 2018 and in an interview with Fox News, OMB Director Mick Mulvaney said the following about Trump's thinking on monetary policy:

[He’s] frustrated that every time things seem to start getting a lot better, the Fed pumps the brakes.

Hopefully, you now understand why I spent so much time walking readers here through this situation in the post linked here at the outset. This is, not to put too fine a point on it, a very big deal.

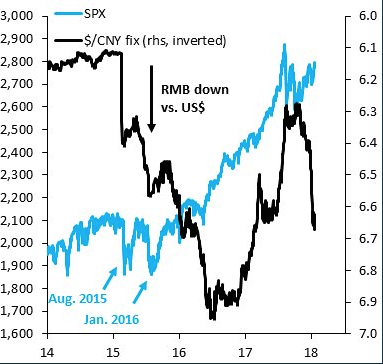

Depending on how China responds, it's possible that we could end up reliving what played out in August of 2015, when the PBoC's overnight devaluation triggered turmoil across the global, culminating in an outright meltdown on August 24. If you don't believe me, just ask former Goldman Chief FX strategist and current Chief Economist at the IIF, Robin Brooks. Here's Bloomberg summarizing his take (this is from the same Bloomberg post linked above):

China’s shock devaluation of the yuan in 2015 provides a good template for what the contagion might look like, according to Robin Brooks, the chief economist at the Institute of International Finance and the former head currency strategist at Goldman Sachs Group Inc. Risk assets and oil prices would likely tumble as worries about growth arise, hitting currencies of commodity - exporting countries particularly hard - namely, the Russian ruble, Colombian peso and Malaysian ringgit - before taking down the rest of Asia.

The question here for China is whether and to what extent they are willing to risk capital flight in order to protect the economy by letting the yuan weaken further against the dollar. The 2015 experience gave Beijing a template for how to control that risk. That certainly seems to suggest they feel more comfortable letting the currency weaken knowing they could, for instance, deploy the counter-cyclical adjustment factor which they rolled out last summer when the yuan was pushing 7.00. One source close to the matter told Reuters the following about that earlier this month:

Currently, the pressure is not as big as in 2015 [and] if the depreciation trend continues like this, they could take some measures, including reviving the counter-cyclical factor, rather than heavy spending of foreign exchange reserves.

Meanwhile, in a Twitter post, the above-mentioned Robin Brooks reminds you that while capital flight is the worry for China, the concern for the U.S. is simply the S&P rally:

China's Achilles heel in a currency war is resumption of capital flight, which in my opinion will become an issue again as $/CNY gets near 7.00. The US' Achilles heel is the SPX, which in 2015/6 tumbled when the RMB fell, on global growth worries. Whose Achilles heel is weaker?

Good question. And it's about to be the question, now that the trade war has, to quote Goldman, evolved "to more directly focus on FX".

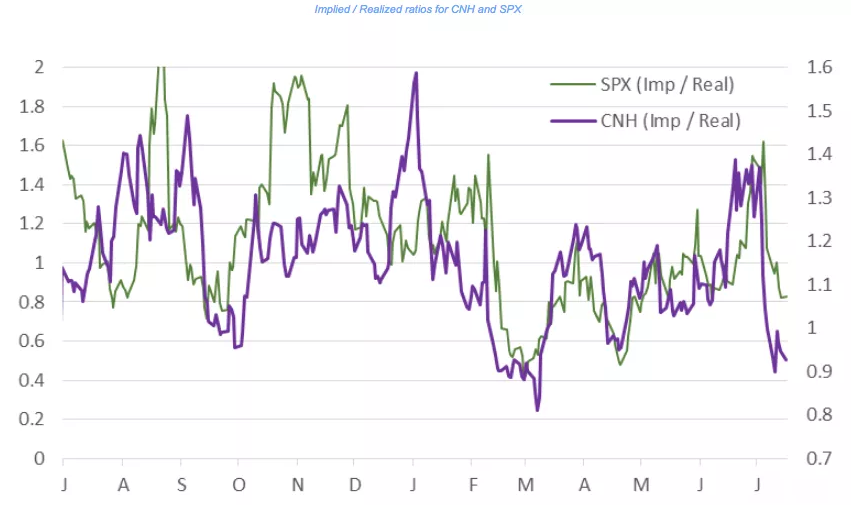

And with that, I'll leave you with one last indelible visual which I highlighted here earlier this week in a post that is looking pretty prescient about now.

(Deutsche Bank)

0 comments:

Publicar un comentario