There Will Be No Economic Boom - Part II

by: Lance Robert

On Tuesday, I presented at the Financial Planning Association (FPA) Conference in Houston at which I discussed the issues surrounding financial planning in an environment of high valuations and low forward returns. After my presentation, a few CFPs approached me to discuss the premise that recent "tax cuts/reforms" will lead to a resurgence of economic growth which will boost earnings and, therefore, negate the overvaluation problema.

This is unlikely to be the case and something that I discussed recently in "There Will Be No Economic Boom." However, that article focused on the impact of the passage of the 2-year "Continuing Resolution" which will lead to a surge in the national deficit as unconstrained spending negates the effect of "tax reform" on the U.S. economy.

But there is more to this story.

When the "tax cut" bill was being passed, everyone from Congress to the mainstream media and, even the CFPs I spoke with yesterday, regurgitated the same "storyline:"

"Tax cuts will lead to an economic boom as corporations increase wages, hire and produce more and consumers have extra money in their pockets to spend."

As I have written many times previously, this was always more "hope" than "reality."

Let me explain.

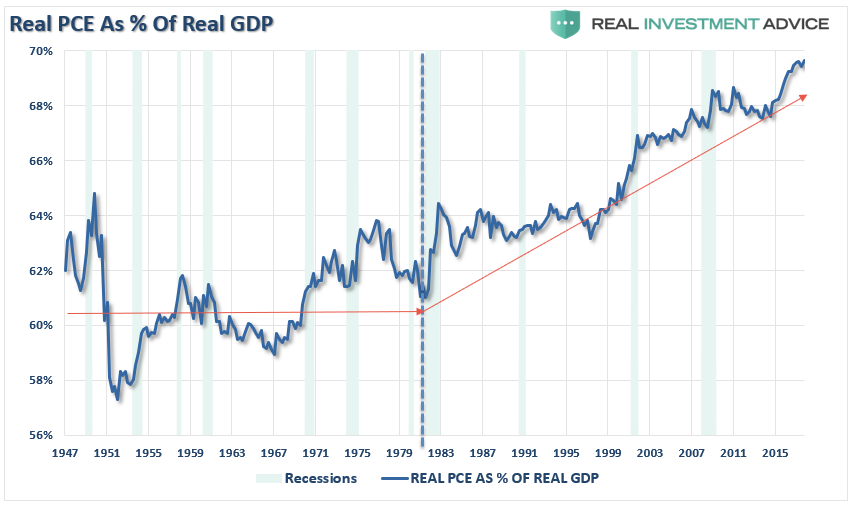

The economy, as we currently calculate it, is roughly 70% driven by what you and I consume or "personal consumption expenditures (PCE)." The chart below shows the history of real, inflation-adjusted, PCE as a percent of real GDP.

If "tax cuts" are going to substantially increase the growth rate of the U.S. economy, as touted by the current Administration, then PCE has to be directly targeted.

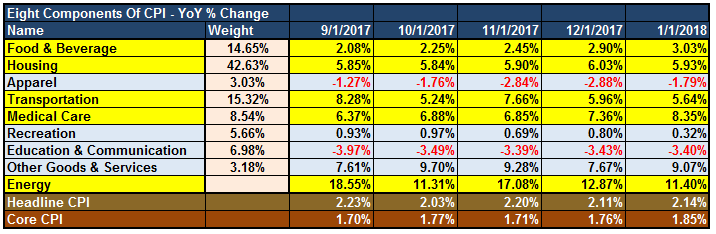

However, while the majority of consumers will receive an "average" of $1,182 in the form of a tax reduction, (or $98.50 a month), the increase in take-home pay has already been offset by surging healthcare cost, rent, energy and higher debt service payments. As shown in the table below - the biggest constituents of the "non-discretionary family budget" are rising the most.

So, since tax cuts, by themselves, are unlikely to offset rising prices of essential goods and services, it's hard to see how they fuel a significant surge in consumer spending.

"No problem. The 'windfall' to corporations (since that is where the bulk of the tax-reform legislation was focused) will lead to a surge in employment, higher wages and increased production.

After all, since corporations can now repatriate those 'trillions of dollars' sitting overseas they will surely be magnanimous of enough to 'share the wealth' with the workers. Right?

Maybe. But anyone who has watched corporate behavior since the "financial crisis" should know that such a belief is heavily flawed.

However, now that we are a couple of months into the New Year, the data is in, and we can see exactly what "corporations" are doing with their dollars.

Wage Increases

Immediately after the passage of the tax reform bill, companies lined up to garner "political favor" by issuing out $1,000 bonus checks to employees. While the mainstream media, and the White House, gushed over the "immediate success" of tax reform, the bigger picture was entirely missed.

A $1000 bonus to an employee is a one-time "feel good" event. Wage increases are "permanent and costly."

The reality is that companies are NOT increasing wages because higher wages increase tax liability, benefit costs, etc. Higher payroll costs erode bottom line profitability. In an economy with very weak top-line revenue growth, companies are extremely protective of profitability to meet Wall Street estimates and support their share price which directly impacts executive compensation.

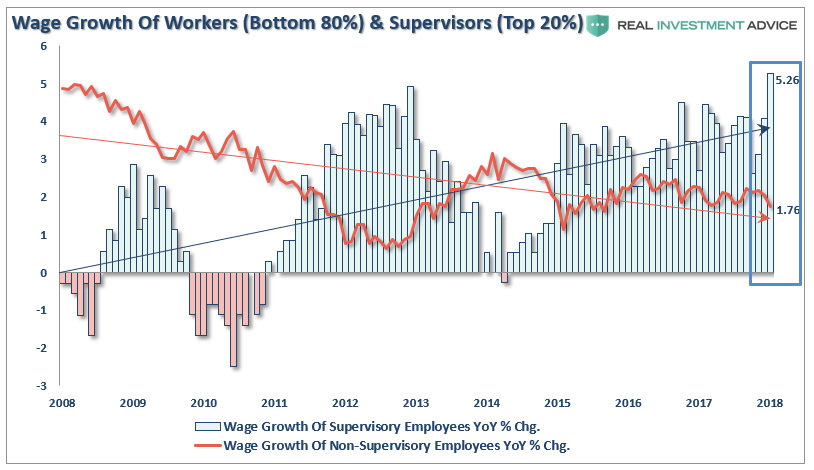

So, while companies are gaining media attention, and political favor, by issuing one-time bonus checks; the bottom 80% of workers are falling woefully behind the top 20%.

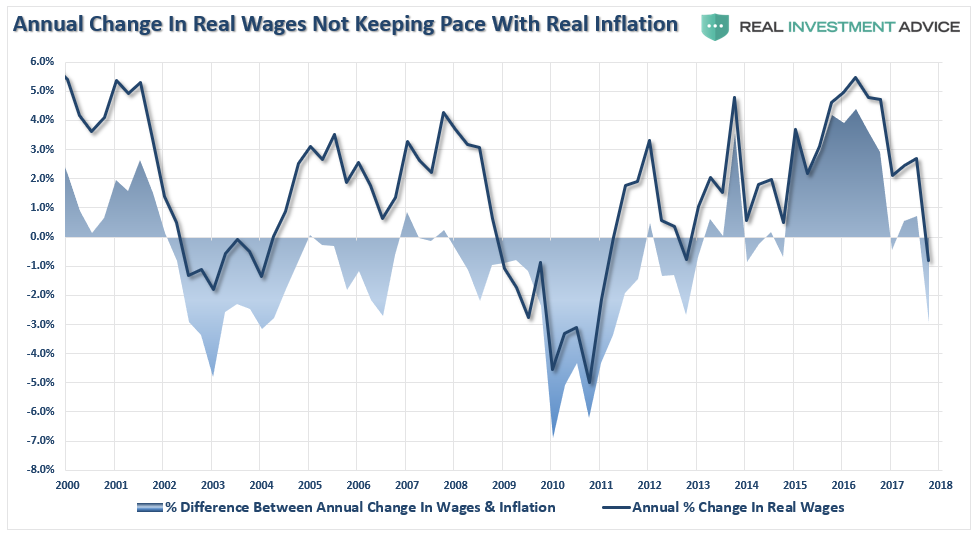

Wages are failing to keep up with even historically low rates of "reported" inflation. Again, we point out that it is likely that your inflation, if it includes the non-discretionary items listed above, is higher than "reported" inflation, and the graph below is actually worse than it appears.

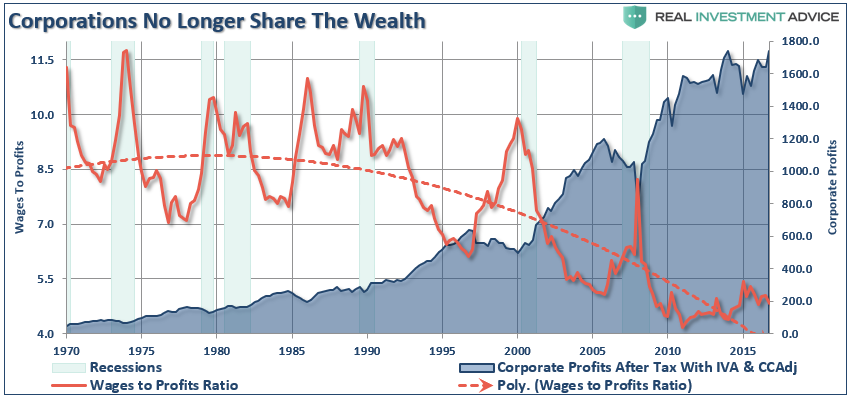

But this is nothing new as corporations have failed to "share the wealth" for the last couple of decades.

Buybacks

The conundrum from "corporate executives" is that if consumers don't have more money to spend, they can't buy the goods and services offered which drives corporate revenue. If revenue does not substantially rise at the top line, profits will be impacted at the bottom line ultimately threatening "executive compensation."

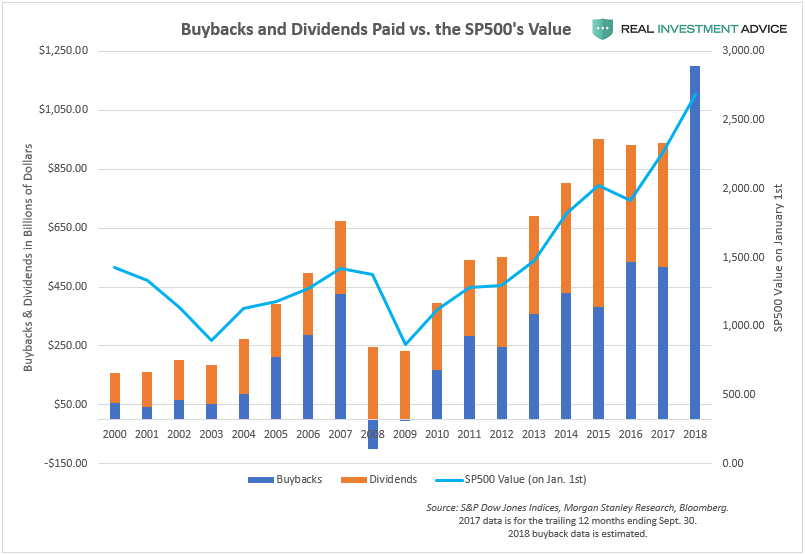

Not surprisingly, the easiest cure for that little problem has been, and remains, share buybacks.

As I discussed previously:

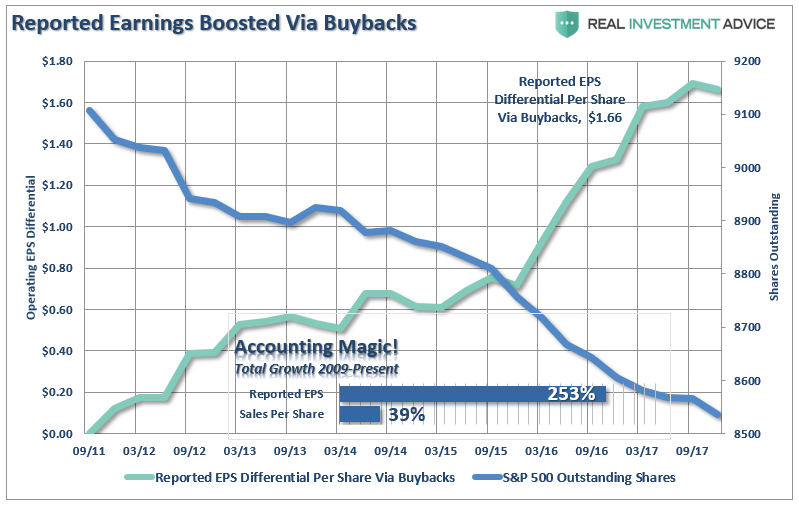

"The use of 'share buybacks' to win the 'beat the estimate' game should not be readily dismissed by investors. One of the primary tools used by businesses to increase profitability has been through the heavy use of stock buybacks. The chart below shows outstanding shares as compared to the difference between operating earnings on a per/share basis before and after buybacks."

I want to draw your attention to the bottom part of the graph Since 2009, the TOTAL growth in sales per share has only been 39% or roughly 3.9% a year, and yet earnings grew at 253% or roughly 25.3% a year. The 21.4% differential has been heavily driven by the reduction in shares outstanding.

The important point here is that 70% of the economy is driven by consumption and the very weak rates of sales (or consumption) show why economic growth remains weak.

So, are companies using their newfound wealth to boost wages? Not so much. As Jesse Colombo recently showed:

"The passing of President Donald Trump's tax reform plan was the primary catalyst that encouraged corporations to dramatically ramp up their share buyback plans."

Dividends

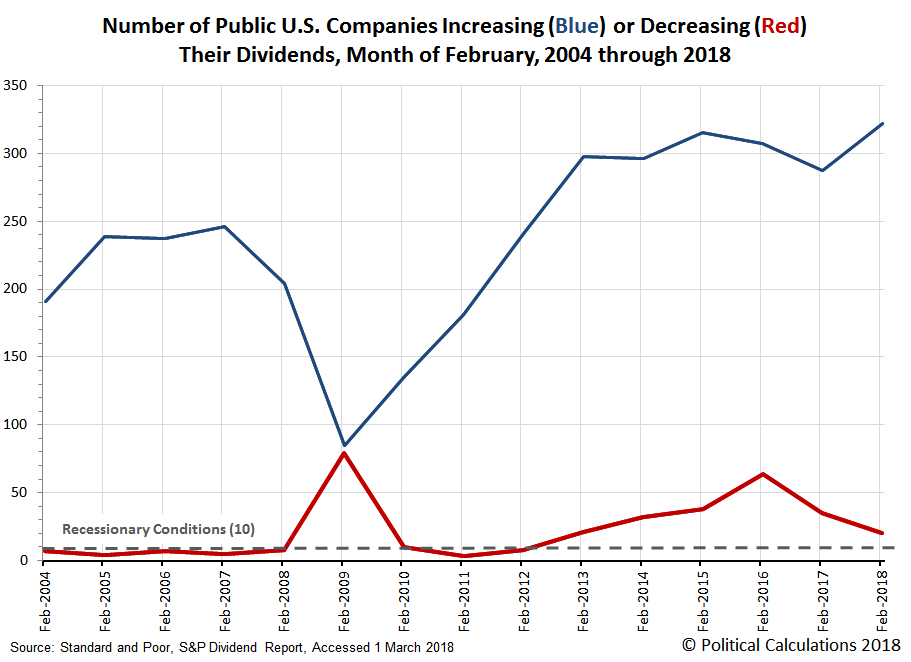

Of course, corporate executives (who tend to own a LOT of company stock and options) can also reward themselves through increases in the dividend payout. Not surprisingly, as noted by Political Calculations, corporate boards have used the recent tax reform to their advantage.

"When it comes to the number of dividend increases declared during a single month, the U.S. stock market just recorded its best February ever."

Conclusion

This issue of whether tax cuts lead to economic growth was examined in a 2014 study by William Gale and Andrew Samwick:

"The argument that income tax cuts raise growth is repeated so often that it is sometimes taken as gospel. However, theory, evidence, and simulation studies tell a different and more complicated story. Tax cuts offer the potential to raise economic growth by improving incentives to work, save, and invest. But they also create income effects that reduce the need to engage in productive economic activity, and they may subsidize old capital, which provides windfall gains to asset holders that undermine incentives for new activity.

In addition, tax cuts as a stand-alone policy (that is, not accompanied by spending cuts) will typically raise the federal budget deficit. The increase in the deficit will reduce national saving - and with it, the capital stock owned by Americans and future national income - and raise interest rates, which will negatively affect investment. The net effect of the tax cuts on growth is thus theoretically uncertain and depends on both the structure of the tax cut itself and the timing and structure of its financing."

While tax cuts CAN be pro-growth, they have to focused on the 80% of Americans that make up the majority of the consumption in the economy. With the benefits of tax cuts being hoarded by the top 20%, which already consume at capacity, there is little propensity to substantially increase consumption as opposed to the accumulation of further wealth.

Furthermore, tax reform does little to address the major structural challenges which provide the greatest headwinds for the economy in the future:

- Demographics

- Structural employment shifts

- Technological innovations

- Globalization

- Pensions

- Financialization

- Debt

These challenges have permanently changed the financial underpinnings of the economy as a whole. This would suggest that the current state of slow economic growth is likely to be with us for far longer than most anticipate. It also puts into question just how much room the Fed has to extract its monetary support before the cracks in the economic foundation begin to widen.

Simply, until you can substantially increase the consumptive capability of the bottom 80%, there will be no "economic boom."

0 comments:

Publicar un comentario