10 Years Gone

by: Eric Parnell, CFA

- Then as it was, then again it will be.

- It was exactly ten years ago today that the U.S. stock market reached its pre-crisis peak.

- While the course may change sometimes, the song remains the same.

- It was exactly ten years ago today that the U.S. stock market reached its pre-crisis peak.

- While the course may change sometimes, the song remains the same.

“Then as it was, then again it will be

And though the course may change sometimes

Rivers always reach the sea”

- Ten Years Gone, Led Zeppelin, 1975

Then as it was exactly ten years ago today. The date was July 19, 2007, and the U.S. stock market closed at another new all-time high. The world was awash with liquidity, risk asset prices were steadily rising, and investor worries were few despite evidence of accumulating risks beneath the global financial system. What subsequently followed over the next 18 months was not only the reemergence of downside risk but the near collapse of the global financial system. Could such a fate possibly be again ten years on?

.

The Last Time Rivers Reached The Sea

The skies were once clear and all was supposedly well. Ten years have gone since July 19, 2007.

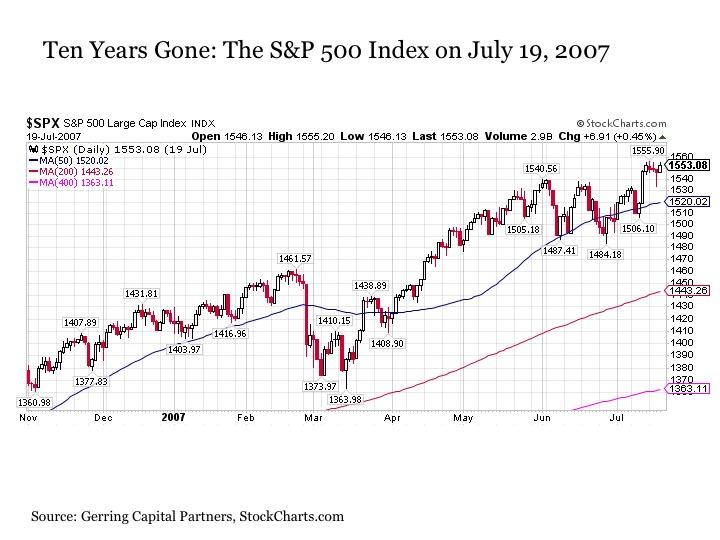

What is so special about this date in particular? It was the date that the U.S. stock market as measured by the S&P 500 Index (SPY) reached its peak before the beginning of the end that soon came to be known as the financial crisis.

Sure, the S&P 500 Index (IVV) closed marginally higher a few months later on October 9, 2007, but by then the die had already been cast, volatility was spiking, and the game was over. When reflecting on the financial crisis and the years that have followed since the deluge of central bank liquidity tamed its flames, the date that I use to mark the beginning of the end is July 19, 2007.

I still remember to this day the mood across capital markets at the time. The summer was hot and stock investors were brimming with optimism. Corporate earnings were steadily rising on both an operating and GAAP basis at the same time that stock valuations were still fairly reasonable in the 16 to 17 times trailing 12-month earnings range. And while 2007 Q1 GDP had been somewhat soft, it was set to rebound to above a +3% annualized rate in the second quarter of the year.

At the same time, inflationary pressures were largely contained at around 2% despite the fact that commodities prices (DJP) including energy (USO) were on the rise. Moreover, the U.S. Federal Reserve was contemplating an easing of monetary policy in order to address some of the pressures that were accumulating in the economy associated with the housing industry. Strong economic growth, low inflation, rising earnings, reasonable valuations, and a potential shift toward more accommodative monetary policy from the U.S. Federal Reserve in the months ahead.

Put simply, what was not to love about investing in risk assets including U.S. stocks (DIA) ten years ago? The subsequent surrender of more than half of total portfolio value over the next twenty months provided the answer.

The Course May Change Sometimes

“Blind stars of fortune, each have several rays

On the wings of maybe, down in birds of prey

Kind of makes me feel sometimes, didn't have to grow

But as the eagle leaves the nest, it's got so far to go”

- Ten Years Gone, Led Zeppelin, 1975

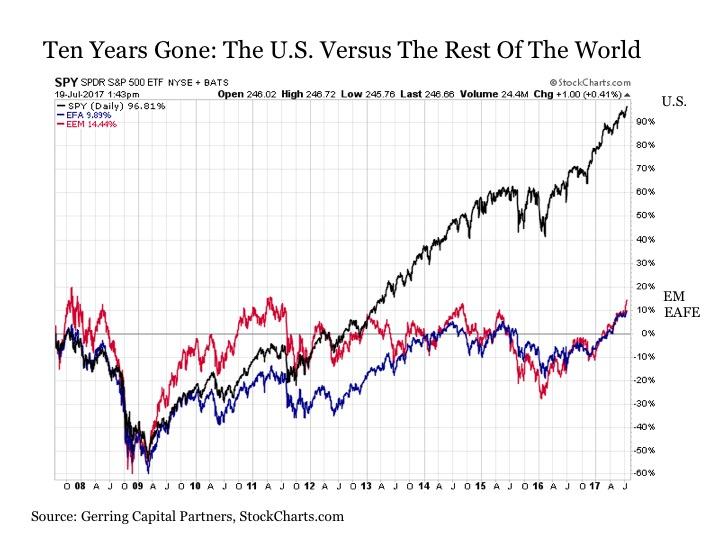

So where are we today, exactly ten years gone from this previous stock market peak? The S&P 500 Index is once again set to close at a new all-time high on July 19, 2017 at a level on Wednesday that is nearly +60% higher than it was ten years ago on a price basis alone. For many investors, it has left them with the understandable feeling that they need not grow from this prior near catastrophic experience. Simply stay the course, endure the short-term volatility that may occur along the way no matter how dramatic, and drift on the rising tide that is the U.S. stock market over long-term periods of time.

If only investors across much of the rest of the developed and emerging world had been so fortunate as their U.S. counterparts over the past ten years. It also stands to reason whether the U.S. stock market eagle has finished its journey or whether it still flies on the wings of maybe after so many years.

So where do we stand today? The U.S. stock market is soaring just as it was ten years ago.

Of course, just because the U.S. stock market peaked exactly ten years ago does not mean it is about to do the same today. A number of factors are completely different today than they were ten years ago.

Let’s begin with a few indicators on the positive side.

First, whereas volatility had been steadily on the rise from historical lows for many months prior to the July 2007 peak, volatility remains at historic lows today.

This leads to an important point, which is that we will likely need to see a sustained rise in stock price volatility before the S&P 500 Index reaches a final peak. This point was also true leading up to the tech bubble peak back in 2000.

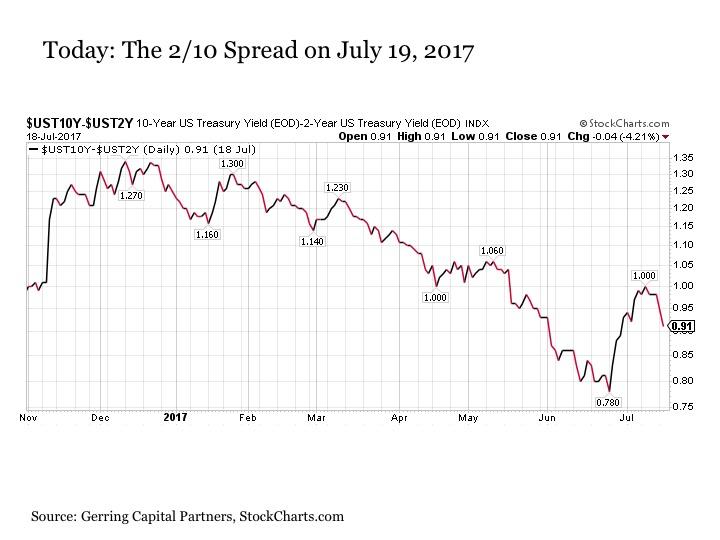

Also, whereas the U.S. Treasury yield curve as measured by the 2/10 spread had already inverted and was starting to steepen again leading up to the stock market peak in July 2007, the yield curve is still flattening and has yet to invert today.

While this suggests the stock market eagle has further to go today, it should be noted that the yield curve was still moving toward flattening and further into inversion at the time when the U.S. stock market first peaked during the tech bubble in March 2000. Nonetheless, the fact that the 2/10 spread is still in the 75 to 100 basis-point range suggests time for further flattening may lie ahead.

Of course, some characteristics of today’s market pale in comparison to July 2007.

The first relates to valuations. For while stocks were trading at around 16 to 17 times trailing earnings back in July 2007, today they are trading in the 22 to 25 times earnings range. While some seek to explain today’s valuation premium away by citing historically low interest rates, it is worth noting that equity risk premiums based on the 10-Year Treasury yield are still at best comparable. Moreover, short-term interest rates are on the rise thanks to the Fed, and according to many (myself not included) are headed higher across the yield curve.

The second relates to monetary policy. Whereas the Fed was headed toward easing monetary conditions in July 2007, it is moving assertively toward tightening monetary conditions today.

Of course, overall monetary conditions remain increasingly easy thanks to the continued liquidity pumping from the European Central Bank and the Bank of Japan, but this is also expected to measurably subside, not expand, in the near term.

The third relates to the economy. Prior to the onset of the financial crisis, U.S. economic growth as measured by real GDP was simply more robust in the 2% to 4% range versus the chronic 1% to 2% growth that we have been experiencing for so many years today. Put more simply, the markets in 2007 still had a decent engine, whereas today it has already been sputtering on liquidity and fumes for years now.

Overall, the course is different today than it was ten years ago. But just as it was, then again it will be that fundamentals will eventually matter as rivers always reach the sea eventually. So too will accumulating systemic risks. This does not appear likely to begin on July 20, 2017 or even over the next couple of months for that matter. But what history from ten years ago reminds us is that it does not take long for the market tides to suddenly turn, for a world awash in liquidity to suddenly turn bone dry, and for the unexpected to turn into the traumatic for those that are not prepared.

Holdin’ On, Ten Years Gone

On a closing note, one thing that has not changed over the past ten years is the blind eyes of central bankers. Read the following and manage your portfolio downside risk accordingly.

"We believe the effect of the troubles in the subprime sector on the broader housing market will be limited and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system"

- U.S. Federal Reserve Chair Ben Bernanke, May 17, 2007

“Would I say there will never, ever be another financial crisis? ... Probably that would be going too far. But I do think we're much safer, and I hope that it will not be in our lifetimes, and I don't believe it will be”

- U.S. Federal Reserve Chair Janet Yellen, June 27, 2017

Oh no, you didn’t! For those investors that are sleeping well at night depending on the omniscience of global central bankers, beware.

The Bottom Line

It has been ten years gone since the last stock market peak and the very beginning of the onset of the financial crisis in the U.S. stock markets. While the course has changed dramatically in the ten years since, and it is likely that today’s market still has time to grow, in many respects the song remains the same. Enjoy the good times while they last, for capital market history has shown that liquidity fuel love inevitably gives way to reality and how things are ultimately meant to be.

0 comments:

Publicar un comentario