Trump Revealed Something That May Be Huge For The Gold Market, But Investors Are Not Paying Attention

by: Hebba Investments

- Donald Trump recently revealed plans to outdo Hillary Clinton with plans for a massive $500 billion dollar infrastructure plan.

-Based on his background as a real estate developer that heavily used debt financing, we think its very likely this is more than just campaign talk.

- Unfortunately, investors have two very different scenarios on how this can play out and how best to take advantage of this shift in US spending policy.

We are not going to wade into the politics of the upcoming November US elections as it is extremely emotional, but we feel that the gold market is ignoring a major issue that was recently discussed in the campaign talk. In a phone interview last week, Donald Trump emphasized that he believed it is necessary that the US government will need to stimulate via more borrowing and spending. That would help lift economic growth, which is a significant departure from traditional Republican economics.

Just yesterday, Mr. Trump elaborated a bit more to Bloomberg as the plan evidently is massive. Trump wants to spend over $500 billion dollars to rebuild U.S. infrastructure, and that is at least double the amount that Hillary Clinton has floated.

We are not concerned about the benefits of the plan, but rather (1) if these are meaningless campaign promises and (2) what would be the implications of the policy. In terms of answering the question whether this is simply campaign talk, we think it is clear knowing Trump's history as a real estate developer that he isn't afraid to use debt to finance infrastructure. That's how he operates and we have no doubt he would be very comfortable financing infrastructure spending via US debt issuance. Throw in the fact that interest rates are at historic lows, and we clearly think this is a no-brainer for either candidate -- especially Trump.

The Implications

The obvious implications for this are that we will see some major increases in US deficit spending.

As investors can clearly see above, deficit spending has plateaued at around 2.8% of GDP, which is a far cry from the 10% seen during the depths of the GFC and subsequent recovery.

There's plenty of room from a historical and academic point-of-view to increase debt further.

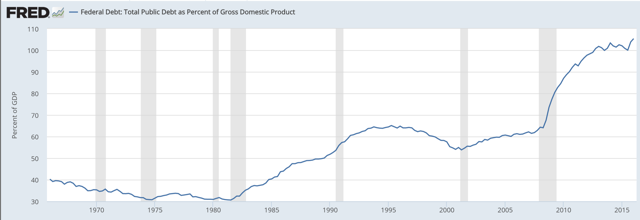

So the obvious consequence of increased deficit spending to the tune of $500+ billion will be an increase in total US debt outstanding and total public debt to GDP.

Source: St Louis Federal Reserve

Source: St Louis Federal Reserve

Quietly US debt has increased despite the drop in deficit spending, and if Trump does enjoy victory come November, we can expect debt to go much higher and the ratio of debt-to-GDP to also increase. Not only that, Hillary Clinton has also pledged to increase infrastructure spending, and even though it isn't as much as Trump, we think that US politics are clearly changing from focusing on responsible spending and budget control to policies geared towards stimulus via direct government spending. It doesn't matter who wins as both candidates are going to open the floodgates to US government infrastructure spending -- is this what commodities have been sniffing over the past few months?

Conclusion for Investors

Increasing the issuance of US treasuries and significantly speeding up the growth of the US National debt should refocus the financial discussion on the sustainability of this debt, which is something that has really been forgotten over the past few years. Maybe this will occur in the run-up to the November US elections or after the elections as infrastructure spending bills are being discussed by the new president and Congress -- it is a matter of when, not if.

The real question is what will investors decide to focus on first -- the inflationary impact of massive infrastructure spending or its impact on the sustainability of debt. If investors focus on the first scenario, then expect a positive impact to stocks as infrastructure companies such as Astec Industries (NASDAQ:ASTE) and United Rentals (NYSE:URI) to have further gains.

Additionally, expect consumer discretionary stocks to also do well as these types of stimulus directly benefit the middle-class and blue-collar workers versus the Fed's current QE programs which primarily benefit Wall Street and those involved in the markets. Additionally, everyday commodities such as copper, steel, and aluminum would clearly benefit further.

For gold and silver, we think the inflationary focus will benefit them, but maybe less than other commodities as gold and silver do best during financially stressful events (inflationary or deflationary). Their protection versus inflation will be beneficial, but excluding hyperinflation, other commodities would offer a similar benefit, and thus they may make better plays in this scenario. Though we would make an argument that silver would be a much better bet than gold because of its industrial nature and the fact that most of annual silver production goes to satisfy industry.

In the secondary scenario where major US infrastructure planning diverts attention back to the sustainability (or unsustainability) of US debt, it's a much different picture for gold and silver.

In this case, we would expect the US dollar to face pressure as treasuries are sold off and the bond vigilantes return and demand higher interest rates. Of course, the Fed will be buying hand-over-fist to maintain current rates, but the additional debt issuance paired with markets focusing back on US debt will make it very difficult for the Fed to control interest rates. This would be extremely positive for precious metals and investors should aggressively accumulate physical gold and the gold ETFs (SPDR Gold Shares (NYSEARCA:GLD), PHYS, CEF) and avoid stocks and commodities.

So which scenario do we think is more likely?

We are still debating which way to go here, but currently we are favoring the first scenario (investor focus on inflation) occurring followed by the second scenario (investor focus on US debt sustainability). That means we are looking for fairly priced infrastructure companies (hard to find) and commodities that have failed to benefit from the recent run-up (think agricultural) and the associated companies. This is not a done deal yet and we will be closely monitoring the market's sentiment for clues on which direction we believe investors will go.

Just yesterday, Mr. Trump elaborated a bit more to Bloomberg as the plan evidently is massive. Trump wants to spend over $500 billion dollars to rebuild U.S. infrastructure, and that is at least double the amount that Hillary Clinton has floated.

We are not concerned about the benefits of the plan, but rather (1) if these are meaningless campaign promises and (2) what would be the implications of the policy. In terms of answering the question whether this is simply campaign talk, we think it is clear knowing Trump's history as a real estate developer that he isn't afraid to use debt to finance infrastructure. That's how he operates and we have no doubt he would be very comfortable financing infrastructure spending via US debt issuance. Throw in the fact that interest rates are at historic lows, and we clearly think this is a no-brainer for either candidate -- especially Trump.

The Implications

The obvious implications for this are that we will see some major increases in US deficit spending.

As investors can clearly see above, deficit spending has plateaued at around 2.8% of GDP, which is a far cry from the 10% seen during the depths of the GFC and subsequent recovery.

There's plenty of room from a historical and academic point-of-view to increase debt further.

So the obvious consequence of increased deficit spending to the tune of $500+ billion will be an increase in total US debt outstanding and total public debt to GDP.

Source: St Louis Federal Reserve

Source: St Louis Federal ReserveQuietly US debt has increased despite the drop in deficit spending, and if Trump does enjoy victory come November, we can expect debt to go much higher and the ratio of debt-to-GDP to also increase. Not only that, Hillary Clinton has also pledged to increase infrastructure spending, and even though it isn't as much as Trump, we think that US politics are clearly changing from focusing on responsible spending and budget control to policies geared towards stimulus via direct government spending. It doesn't matter who wins as both candidates are going to open the floodgates to US government infrastructure spending -- is this what commodities have been sniffing over the past few months?

Conclusion for Investors

Increasing the issuance of US treasuries and significantly speeding up the growth of the US National debt should refocus the financial discussion on the sustainability of this debt, which is something that has really been forgotten over the past few years. Maybe this will occur in the run-up to the November US elections or after the elections as infrastructure spending bills are being discussed by the new president and Congress -- it is a matter of when, not if.

The real question is what will investors decide to focus on first -- the inflationary impact of massive infrastructure spending or its impact on the sustainability of debt. If investors focus on the first scenario, then expect a positive impact to stocks as infrastructure companies such as Astec Industries (NASDAQ:ASTE) and United Rentals (NYSE:URI) to have further gains.

Additionally, expect consumer discretionary stocks to also do well as these types of stimulus directly benefit the middle-class and blue-collar workers versus the Fed's current QE programs which primarily benefit Wall Street and those involved in the markets. Additionally, everyday commodities such as copper, steel, and aluminum would clearly benefit further.

For gold and silver, we think the inflationary focus will benefit them, but maybe less than other commodities as gold and silver do best during financially stressful events (inflationary or deflationary). Their protection versus inflation will be beneficial, but excluding hyperinflation, other commodities would offer a similar benefit, and thus they may make better plays in this scenario. Though we would make an argument that silver would be a much better bet than gold because of its industrial nature and the fact that most of annual silver production goes to satisfy industry.

In the secondary scenario where major US infrastructure planning diverts attention back to the sustainability (or unsustainability) of US debt, it's a much different picture for gold and silver.

In this case, we would expect the US dollar to face pressure as treasuries are sold off and the bond vigilantes return and demand higher interest rates. Of course, the Fed will be buying hand-over-fist to maintain current rates, but the additional debt issuance paired with markets focusing back on US debt will make it very difficult for the Fed to control interest rates. This would be extremely positive for precious metals and investors should aggressively accumulate physical gold and the gold ETFs (SPDR Gold Shares (NYSEARCA:GLD), PHYS, CEF) and avoid stocks and commodities.

So which scenario do we think is more likely?

We are still debating which way to go here, but currently we are favoring the first scenario (investor focus on inflation) occurring followed by the second scenario (investor focus on US debt sustainability). That means we are looking for fairly priced infrastructure companies (hard to find) and commodities that have failed to benefit from the recent run-up (think agricultural) and the associated companies. This is not a done deal yet and we will be closely monitoring the market's sentiment for clues on which direction we believe investors will go.

0 comments:

Publicar un comentario