Renzi’s

Great Gamble

John Mauldin

There

is an extremely important election coming up, and I am not talking about the US

presidential election. The upcoming referendum in either October or November in

Italy may have as much or even more macroeconomic impact on the world as the US

election, but hardly anyone outside of Italy is paying much attention to it –

yet.

I have been saying for some time in interviews

around the country that I think the referendum in Italy has even more potential

impact than the Brexit vote did in the United Kingdom. And just like the Brexit

vote, it is rife with emotion and political turmoil, making the outcome too

close to call.

If you are a voter in Italy, your frustration (or

maybe even anger) is entirely understandable.

The current prime minister,

Matteo Renzi, has basically bet his career on this referendum, which would

allow him to enact what most of us would see as much-needed reforms – in fact

they’re the very Italian reforms that I have written about in my letters over

the last five years and that I talked about in my previous two books. Italy has

about as sclerotic a governmental process as any country in Europe, and that is

saying something. There is no end of corruption and crony politics, with each

faction wanting to keep the status quo and not have to give up any of its perks

but wanting everybody else to give up all of theirs. Not unlike a country close

to where I reside (I say with a smile and a sigh).

Seriously, friends, this needs to go on your

economic radar screen. If the “no” vote wins, Renzi has promised to resign,

which will throw Italy into a political crisis. Then there will be a real

potential to elect parties that would call for a plebiscite on whether to stay

in the European Union – Italexit – and is not at all clear today what the

Italians would decide to do. Know this: the European Monetary Union really does

not work very well, if at all, without Italy, and a “no” vote would be the

death knell of the euro, at least as we know it today.

Nick Andrews, who writes for my friends at

GaveKal, has done an excellent summary of the situation in Italy, and his

latest posting is this week’s Outside the Box. This is not a long

essay, but it is worth every bit of your attention.

I have just about recovered my operational

abilities here at Mauldin headquarters (which is actually my office at home).

We are taking steps to make sure there is never a repeat of this computer

debacle. I can point fingers here and there; but as they say, the buck stops

here.

I hope the weather where you are is as pleasant

as it is here in Dallas. Have a great week. I will be writing this weekend

about why I am so disturbed about the negative interest rates set by current

monetary policy that is in control of the economies of the world. It should be

interesting.

Your wishing he had been in Tuscany for a few

weeks this summer analyst,

John Mauldin, Editor

Outside the Box

Renzi’s Great Gamble

By Nick Andrews and Stefano Capacci

Prime ministers come and go in Italy – four since

the financial crisis – but precious little seems to change. The latest

incumbent, Matteo Renzi, has pursued structural reform more energetically than

his predecessors. But for all the progress he has made, he might as well have

been wading through molasses. Now, in a bid to secure a popular mandate for his

restructuring program, Renzi has bet his premiership on a referendum over

badly-needed constitutional reforms. It is a high stakes gamble. If Renzi wins

the vote, which is due in either October or November, his proposed measures

will streamline Italy’s legislative process, breaking the parliamentary

gridlock which has crippled successive governments, and opening the way to

far-reaching economic reforms. If he loses, Renzi has promised to step down – a

pledge that has turned the referendum into a popular vote of confidence in the

unelected prime minister, his Europhile policies, and by extension Italy’s membership

of the eurozone itself. As a result, a “No” vote in October will not just

precipitate the fall of Renzi’s government; it could throw Italy’s long term

membership of the eurozone into doubt, plunging the single currency area once

again into crisis.

Policy no man’s land

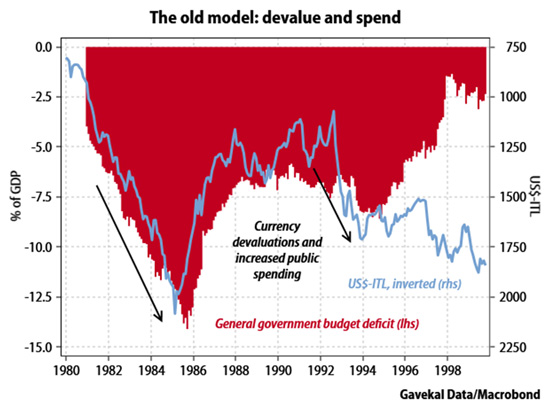

Italy’s fundamental problem is that it is stuck in

a policy no man’s land. Its old economic model, in place for much of the last

three decades of the 20th century, relied on a combination of

currency devaluation to maintain international competitiveness together with

fiscal spending to support the poorer regions of the country’s south.

Signing up to the euro put an end to all that,

preventing devaluations and prohibiting budget deficits at 10% of gross

domestic product. However, the design of Italy’s bicameral parliamentary

system, in which the upper and lower house – the Senate and the Chamber of

Deputies – wield equal legislative power, made it almost impossible for any

government to push through the structural reforms necessary for Italy to

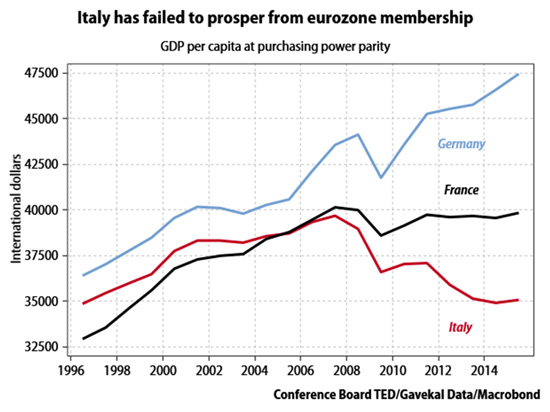

compete and prosper within the eurozone. The result has not just been depressed

growth and relative impoverishment, but an outright decline in living

standards, as Italy’s real GDP per capita has slumped to a 20-year low.

Such a below-par economic performance has led to a

build-up of bad assets on the balance sheets of Italy’s banks, where 18% of all

loans are now classed as non-performing. In turn, this bad loan overhang has

eroded the ability of the banking sector to extend new credit to the thousands

of small businesses which are the engine of Italy’s economy and which normally

power employment growth. The result is stagnation.

To stand any chance of escaping this low growth

trap, Italy needs to enact wholesale structural reforms to enhance its

competitiveness relative to its eurozone neighbors. Notably, it needs to make

the labor market more flexible to encourage job creation, it needs to lower the

barriers to entry that protect much of the country’s service sector, it needs

to overhaul a judicial system so sclerotic that bankruptcy proceedings can last

10 years or more, and it needs to restructure its fragmented and dysfunctional

banking system.

The prescription might be clear, but Italy’s

political system makes enacting reform all but impossible. Renzi has already

tried to overhaul Italy’s labor market by attempting to dismantle the generous

protections that make it difficult and expensive for companies to dismiss

staff, and which therefore encourage businesses to hire only temporary workers,

heightening economic insecurity among the young.

But Renzi’s attempt ran into bruising opposition

from Italy’s powerful and well-subscribed trade unions. The results were a

watered-down reform package that entitles existing permanent staff to a

near-guarantee of lifetime employment, and a severe dent in Renzi’s popularity

from which he is yet to recover. It’s a familiar story in Italy. Entrenched

interests, whether represented by local and regional political leaders, unions,

protected professions, or established private sector companies, exert enormous

influence over the political process. All profit from the status quo, which

promises they will continue to benefit from special protections and payouts.

And because of the equal balance of power in Italy’s parliament, which means

the Senate can block government legislation indefinitely, the consequence is

political – and economic – stagnation.

Bloated and wasteful

Renzi’s referendum aims to change that. The prime

minister is seeking popular approval for constitutional reforms that promise to

cut the size of the upper house from 315 to 100 senators. Under his proposals,

senators will no longer be directly elected, but will instead be chosen by

regional councils, nominated by the mayors of big cities, or – in the case of

five – be appointed by the Italian president. The reform will not only cut the

costs of the notoriously bloated and wasteful upper house, where senators have

traditionally enjoyed lavish expenses and generous pensions. Most importantly,

it will downgrade the political power of the Senate so that it will no longer

be able to obstruct government legislation entirely, but only to propose

amendments that will be adopted at the discretion of the lower house (although

the Senate will retain a say on constitutional ma tters, including the

ratification of European Union Treaties). The objective is to increase the

executive power of the government, and to tackle entrenched interests with

additional measures that allow for new laws to facilitate popular referendums

and to promote citizen participation in the political process.

Unlikely alliance

However, powerful forces are arrayed against Renzi,

and a “Yes” vote is far from assured. The proposed reforms have attracted

opposition not only from establishment voices who benefit from the current

arrangements. They have also drawn fire from constitutional lawyers and

anti-establishment parties, including the populist 5-Star Movement, which

argues the 50% simple majority needed to win the referendum is too low for

constitutional changes that promise a concentration of political power

unprecedented since the formation of the Italian republic in 1946.

Perhaps more importantly, Renzi’s pledge to resign

in the event of a “No” victory has raised the possibility of a protest vote

against the prime minister himself – the third unelected head of government in

succession – from a broad cohort of the electorate which is thoroughly

disillusioned with Italian politics. Increasingly disgruntled, these voters are

sick of the corruption and self interest of politicians, and fed up with

painfully austere policies that they believe to be dictated from Brussels and

Berlin, and which they hold responsible for Italy’s poor economic performance.

The chances of a “Yes” vote in the referendum have

not been improved by the slump in Renzi’s personal popularity following last

year’s attempt to reform the labor market, and a series of small bank

restructurings that saw retail savers “bailed-in” – forced to take losses –

under new European Union banking regulations. From 40% after Renzi entered

office two years ago with optimistic promises of reform, the approval rating of

the prime minister’s PD party has fallen to little better than 30% today, much

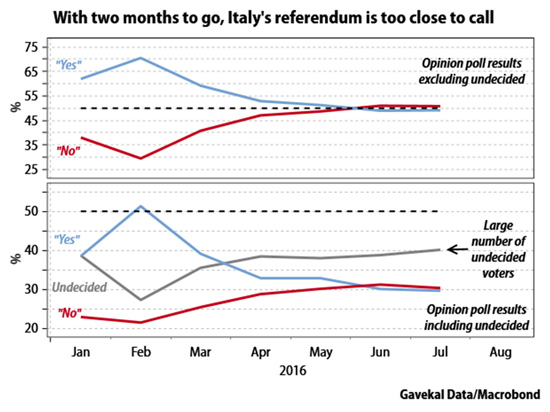

the same as that of the opposition 5-Star Movement. As a result, with two

months to go the referendum is too close to call. Opinion polls indicate the

“Yes” and “No” camps are running roughly equal, with a large proportion of

voters still undecided.

If Renzi loses the referendum, not only will Italy

remain in policy limbo, but it is highly likely his subsequent resignation will

trigger a parliamentary election. Under new election laws passed last year, if

a party fails to win 40% in the first round of voting, the top two parties go

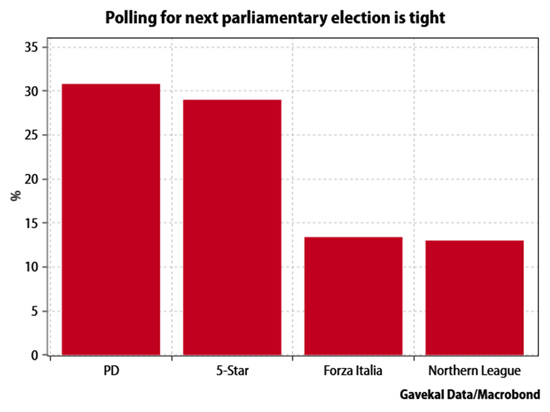

through to a second round. The latest opinion polls put Renzi’s governing PD

party on 31% and the 5-Star Movement on 29%, with the next two largest parties

– Silvio Berlusconi’s Forza Italia and the anti-establishment Northern League –

level pegging on around 13%.

In recent years, Renzi’s PD government has represented

the best hope for structural reform and economic modernization. But even if the

PD party were to win a post-referendum election, there is a risk that,

following Renzi’s resignation, the left wing of the party would wrest back

control from the reformist center-right faction, damping hopes for further

restructuring. Such a swing to the left would hardly be unique to Italy. In the

UK, the militant left has captured the leadership of the main opposition Labour

Party. In Spain, Podemos has split the left wing vote, and in France the ruling

Socialists have come under pressure in the polls from the radical and

Euroskeptic Left Party led by Jean-Luc Mélenchon.

At the moment, an election victory for the 5-Star

Movement, which identifies as neither left nor right, appears at least as

probable as a second round win for the PD. The Movement has already scored

significant victories in mayoral elections in Rome and Turin, and enjoys increasing

support across the country. Its broad stance is anti-establishment and in favor

of direct participatory democracy rather than representative democracy, which

it regards – with some justification in Italy – as an invitation to corruption.

Beyond that, however, its platform is so vague that it is hard to pinpoint any

concrete policies, except its call for a referendum on Italy’s membership of

Europe’s single currency.

Leadership vacuum

Perhaps the biggest problem for 5-Star, however, is

that it has no clear leader. Its founder and leading voice, Beppe Grillo, was

found guilty of involuntary manslaughter in 1980 following a fatal road traffic

accident, and so cannot run for public office under Movement rules barring

candidates with criminal records. Without Grillo the parliamentary party would

be leaderless, meaning 5-Star has no obvious prime ministerial candidate even

should it secure a majority in the election.

All this means that the possibility of a “No” vote

in Italy’s constitutional referendum come October or November is the biggest

clear and present danger to the euro’s survival. Both 5-Star and the Northern

League are promising a plebiscite on euro membership should they come to power

in a post-referendum election. That does not mean a vote on Italy’s eurozone

membership would lead directly to its exit – many likely “No” voters in this

year’s constitutional referendum favor continued euro membership. However, a

“No” vote come October would effectively be a vote against the structural

reforms needed to ensure Italy’s economic growth and prosperity within the

eurozone.

In other words, in the event of a “No” vote in

October, the only economic choice for Italy would be between continued

stagnation, or a return to the old economic model of successive devaluations.

The latter course would naturally mean exiting the eurozone anyway. But even if

Italy were to take that path, it would hardly be a less painful way to restore

the economy to health. Whether inside or outside the single currency, Italy

still needs structural reform to ensure future growth. The only potential

benefit to leaving the eurozone would be that deep devaluation of a

reconstituted lira could help to ease some of the transitional pain (although

it is probable the palliative effect would be more than offset by the

additional economic and financial damage wreaked by an exit).

Europe in microcosm

Clearly investors should be concerned. Italy is the

third biggest economy in the monetary union and one of its core members. Its

departure would surely hasten the break-up of the whole euro project. What’s

more, the political and economic tensions within Italy ahead of October’s

referendum mirror those at work across the eurozone as a whole. In Italy the

wealthy north makes up the industrial heartland which drives the economy, while

the south is underdeveloped and poor. There is little enthusiasm for structural

reforms, and throughout the country populist movements which promise to tear

down the self-serving political establishment are rapidly gaining ground.

Italy is the wider eurozone in microcosm. In the EU

as a whole, progress towards creating the political and economic institutions

that could ensure the success of the single currency project have been

comprehensively obstructed by narrow – but deeply entrenched – national

interests. This failure to advance, and the economic hardships and sense of

disempowerment that have resulted, has fueled the rise of populist political

parties from Greece to Finland – parties that are challenging an increasingly

distrusted political elite and questioning not just the status quo, but the

whole European project. If Renzi wins come October, the eurozone has fresh

hope. But if he fails, Italy fails, and very likely the eurozone fails too.

0 comments:

Publicar un comentario