John Mauldin

Today’s Outside the Box is a little bit different – which, considering that most Outside the Box pieces can be classified as a little bit different, is not that unusual; but this one needs to come with a warning label that you may find it a tad wonkish.

It’s from my friend Chris Whalen of the Kroll Bond Rating Agency. When I want to understand something about banks, Chris is one of my go-to guys.

It’s from my friend Chris Whalen of the Kroll Bond Rating Agency. When I want to understand something about banks, Chris is one of my go-to guys.

In Chris’s latest memo he talks about the push to increase the capital levels of the eight largest US banks. He is critical of that effort in that it doesn’t address the real issues. He highlights the fact that even if we do increase the capital requirements of the largest banks, that doesn’t mean we won’t have problems with them in the next crisis.

It wasn’t insufficient capital that got the banks into trouble the last time around. If we don’t sufficiently address the issues that hurt the banks and the economy then, there can be no assurance that there won’t be problems of a similar nature next time, even with increased capital. This is worth thinking about as you ponder the risks to your portfolio that will come with the next downturn. You can’t assume there will not be problems with US banks. Maybe there won’t be, but I wouldn’t ignore the risk. Good management is more important than capital.

I write this introduction from 32,000 feet, flying back to Dallas. I had several great meetings while in New York; but the highlight was dinner last night with Art Cashin; Jack Rivkin, a longtime PaineWebber partner and now the brains at Altegris; Peter Boockvar of the Lindsey Group; Rich Yamarone, chief economist at Bloomberg; Lakshman Achuthan, the guiding light at ECRI; and Vikram Mansharamani, a Yale professor and author of Boombustology. These are the proverbial smartest guys in the room, and I posed a series of questions to them about the timing of the next recession, their thoughts on the upcoming election, and the economy in general.

I’ll take up their range of predictions and consensus regarding the recession call in this weekend’s letter, and go into some of the risks these gentlemen see, as well as dive into more of my notes from the conference.

My decision to not go to a game three or four of the NBA finals and hope for a game six –knowing that it could be a possible closer and hoping that it would be a win for the Cavaliers while I was down front in a box seat – now looks to be a bit suspect. I may not be making that trip unless Lebron and the Cavs get their act together and sweep the Warriors at home. After those first two games, I think I’ll hold off booking the tickets.

You have a great week. I think I’ll call a few more friends and get some additional takes on a recession. Just for giggles and grins.

Your thinking about portfolio risk analyst,

John Mauldin, Editor

Outside the Box

Large Bank Risk:

Liquidity Not Capital Is the Issue

“Credit means that a certain

confidence is given, and a certain trust reposed. Is that trust justified? And

is that confidence wise? These are the cardinal questions.”

– Walter Bagehot, Lombard

Street (1873)

Summary

·

Kroll

Bond Rating Agency (KBRA) notes that since the 2008 financial crisis and the

passage of the Dodd-Frank legislation two years later, global financial

regulators have been pushing a deliberate agenda to increase the capitalization

of large banks. Despite the fact that the 2008 financial crisis was not caused

by a lack of capital inside major financial institutions, raising capital

levels has become the primary policy response among many of the G-20 nations.

·

KBRA

believes that using higher capital to change bank profitability and,

indirectly, corporate behavior is a rather blunt tool for the task of ensuring

the stability of financial markets. Part of the problem with using capital as a

broad prescription for avoiding rescues for large financial institutions, aka

“too big to fail” or TBTF, is that this approach explicitly avoids addressing

the actual cause of the problem, namely errors and omissions by major banks

that undermined investor confidence.

·

One

of the key fallacies embraced by regulators and policy makers is the notion

that higher capital levels will help TBTF banks avoid failure and, even in the

event, the failure of a large bank will not require public support. KBRA

believes that there is no evidence that higher levels of capital would have

prevented the “run on liquidity” which caused a number of depositories and

non-banks to fail starting in 2007.

Discussion

Since the 2008 financial crisis and the passage of

the Dodd-Frank legislation two years later, global financial regulators have

been pushing a deliberate agenda to increase the capitalization of large banks.

The objective of this increase in capital, we are told, is to make public

rescues of the largest banks less likely and to change their corporate

behavior. Despite the fact that the 2008 financial crisis was not caused by a

lack of capital inside major financial institutions, raising capital levels has

become the primary policy response among many of the G-20 nations and the

prudential regulators who oversee global banks.

Most recently, Federal Reserve Board Governor

Daniel Tarullo revealed on Bloomberg TV (June 2, 2016) that he is

“quite confident” that the eight largest U.S. banks will get hit with an

additional capital surcharge that will translate into a “significant increase”

in capital. However, he noted that there will be “some offsets in other parts

of the stress tests so that it won’t be just a straight addition of the

surcharge.” Tarullo opined that he doesn’t think the charge will go into effect

for the next round of tests, and instead there might be a “phase in.”

Lawmakers and federal regulators have made a number

of other changes in the regulation of US banks that impact asset allocation and

risk taking, including greater emphasis on liquidity and an end to principal

trading. Policy makers have explicitly ruled out direct punishment for

individual or institutional instances of fraud, thus we are left with an

indirect approach that punishes the creditors, shareholders and customers of

the largest banks. President Obama formed a “Financial Fraud Enforcement Task

Force” in November 2009 to “hold accountable those who helped bring about the

last financial crisis,” but the Obama administration has generally chosen to

pursue institutions over individuals when it comes to fraud prosecutions.

“More

equity may get [bank] boards to care more,” argues Dr. Anat Admati of Stanford

University, but KBRA believes that using higher capital to change bank

profitability and, indirectly, corporate behavior is a rather blunt tool for the

task of ensuring financial stability.

Part of the problem with using capital as a broad

prescription for avoiding rescues for large financial institutions, aka “too

big to fail”, is that this approach explicitly avoids addressing the actual

cause of the problem, namely errors and omissions by the officers and directors

of major banks that undermined investor confidence. A combination of poor loan

underwriting, excess risk taking in the trading and investment portfolios,

deliberate acts of deceit, a systemic failure to disclose the true extent of

bank liabilities, and/or acts of securities fraud actually caused the failure

of or need to rescue institutions such as Wachovia Bank, Washington Mutual,

Lehman Brothers, Bear, Stearns & Co American International Group (NYSE:AIG)

and Citigroup (NYSE:C), to name but a few. These rescues or events of default

were driven by a sharp decline in liquidity available to these obligors and led

to the wider financial crisis in 2008 and beyond.

Thus when regulators and policy makers sign on to

the idea of higher capital levels as a solution for TBTF, are we not all

effectively burying our collective heads in the sand? In mid-2008, when

Wachovia was receiving inquiries from bond investors about early redemption of

long-term debt, the bank’s stated level of balance sheet capital was not at

issue. Instead, investors, counterparties, and corporate/institutional

depositors were concerned that they no longer understood or trusted the bank’s

asset quality and financial statements, and therefore backed away from any risk

exposures with the bank. This is also why the Federal Reserve Board and

Treasury chose to conceal the true condition of Wachovia from the FDIC, as

former FDIC Chairman Sheila Bair documents in her 2013 book.

Fed Chairman Ben Bernanke noted in the dark days of 2008:

Meeting creditors’ demands for

payment requires holding liquidity--cash, essentially, or close equivalents.

But neither individual institutions, nor the private sector as a whole, can

maintain enough cash on hand to meet a demand for liquidation of all, or even a

substantial fraction of, short-term liabilities... [H]olding liquid assets that

are only a fraction of short-term liabilities presents an obvious risk. If most

or all creditors, for lack of confidence or some other reason, demand cash at

the same time, a borrower that finances longer-term assets with liquid

liabilities will not be able to meet the demand.

There are two basic reasons why the current

fixation with higher capital levels should be a cause for concern among policy

makers. First, there is no evidence that higher levels of capital would have

prevented the “run on liquidity” which caused a number of large depositories

and non-banks to fail starting in 2007. Reckless and questionable financial

decisions characterized, for example, by a failure to properly evaluate the

creditworthiness of borrowers were the proximate causes of an erosion in

investor confidence which ultimately caused these firms to collapse. (See

Whalen, Richard Christopher, The Subprime Crisis: Cause, Effect and

Consequences (2008). Networks Financial Institute Policy Brief No. 2008-PB-04. http://ssrn.com/abstract=1113888)

Careful observers of the banking scene in the 2000s

noted that names such as Washington Mutual and Countrywide Financial were

starting to contract in terms of sales volumes and access to liquidity as early

as 2005. The originate-to-sell mortgage production models used by these and

other banks depended crucially on access to stable market funding and a steady

supply of new paper. In mid-2007 when Bank of America (NYSE:BAC) announced a

partial rescue for its largest warehouse customer, Countrywide, the mortgage

bank led by Angelo Mozilo was already doomed because of ebbing loan volumes and

liquidity. More non-bank than commercial bank, half of Countrywide’s balance

sheet was funded by non-deposit, market sources.

Second, significantly higher capital levels and

other regulatory constraints reduce the profitability of banks and limit credit

expansion. The fact that the U.S. banking industry was able to fund the

post-crisis cleanup internally by diverting income is a remarkable achievement,

yet the response from policy makers has been to take deliberate action that

make banks less profitable and less able to fund future losses.

More, higher capital levels have negative effects

on capital formation and credit creation that may work against the broader

goals of financial stability and economic growth. Witness the declining bank

lending volumes in the US residential mortgage market. Banks which cannot

achieve sufficient equity returns to retain investors will, over time, either

shrink or discontinue businesses altogether to survive. Under the current

regulatory regime, banks in the G-20 nations are effectively being turned into

utilities which take little or no credit risk and thus do not support economic

activity.

Not only do higher capital levels and other forms

of punitive regulation reduce the availability of credit from depositories, but

these strictures will tend to force consumers and businesses to seek out credit

from unconventional sources that may actually increase systemic risk to the

financial system. The proliferation of various types of non-bank lenders

purporting to offer “new” business models are a familiar response to increased

regulation and tougher prudential standards. Many of these models have

originate-to-sell business models similar to that used in originating subprime

mortgages in the 2000s. For example, JPMorgan Chase & Co. Chief Executive

Officer Jamie Dimon, says marketplace lenders might find that sources of

funding evaporate during a downturn. (Hugh Son et al, “Dimon Says Online

Lenders’ Funding Not Secure in Tough Times,” Bloomberg News, May 11,

2016.)

Capital

vs. Confidence

One of the key fallacies embraced by bank

regulators is the notion that higher capital levels will help TBTF banks avoid

failure and, even in the event, the failure of a large bank will not require

public support. First and foremost, banks fail not because they run out of

capital, but because a lack of confidence results in a diminution of liquidity

available to the enterprise.

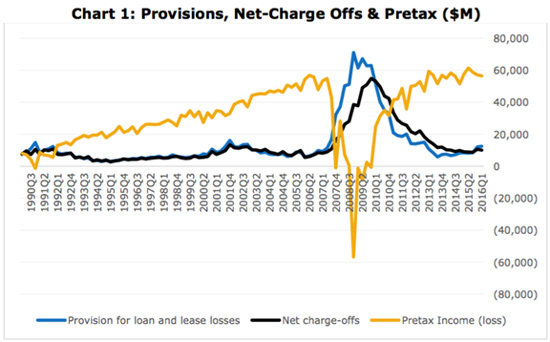

Indeed, during and after the 2008 financial crisis,

with the notable exception of Citigroup and AIG, U.S. banks as a group did not

require government support and consumed little capital in resolving failed

institutions. Instead, banks diverted current income to fund loan loss

provisions and FDIC insurance premiums. Using data from the FDIC, Chart 1 shows

provisions, net charge-offs, and pretax income for all U.S. banks since 1990.

Note that the sharp drop in industry operating

income in 2008-2009 included the cost of pre-paying several years of FDIC

insurance premiums. Not only did the U.S. banking industry fund the clean-up of

most failed banks privately and without taxpayer support, but the financial

crisis turned out to be an issue of reduced income rather than capital

impairment. Though hundreds of banks did fail because of loan losses, the

balance sheets of these institutions were marked to market and absorbed by the

surviving banks, which largely used income rather than capital to manage the

resolution process. Indeed, at no point did any major bank “run out of capital”

because the institutions which did fail stumbled long before due to a lack of

cash liquidity and were sold by the FDIC.

Ultimately, market liquidity is a function of

investor confidence, and not capital. Cash flowed into the largest banks in the

weeks after the failure of Lehman Brothers because the banks were big and

investors believed these banks would receive government support. Liquidity is

the key determinant of whether a bank or nonbank fails. Indeed, for most credit

professionals surveyed by KBRA, credit spreads and ratings, and other dynamic

market indicators, are far more important measures of particular counterparty

risk than static, backward-looking measures of balance sheet capital.

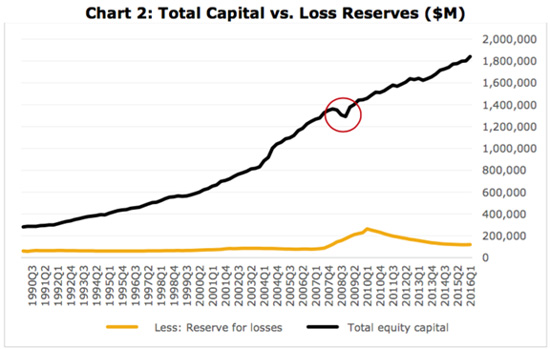

In Chart 2, we show total capital vs. loss reserves

since 1990. Again, aside from accounting adjustments and some large bank

resolutions in the 2008-2009 period (see circle in Chart 2), the U.S. banking

industry has continued to build capital steadily. When Wachovia Corp was acquired

by Wells Fargo at the end of 2008, the target charged off its entire loss

reserve and equity capital in Q3 2008, resulting in a substantial write-down of

doubtful assets and the creation of a loss reserve for the acquirer. As the

FDIC noted at the time, this transaction involving the fourth largest U.S. bank

holding company skewed the aggregate industry data during that reporting

period.

Conclusion

In his famous exchange with attorney Samuel

Untermyer over a century ago, John Pierpont (“JP”) Morgan stated the problem of

bank solvency correctly and for all time. In those days, bear in mind, the Fed

did not exist and JPMorgan & Co was the de facto central bank.

Because Morgan was not a member of the New York Clearinghouse, other banks had

to stand in line inside the bank’s lobby to transact business:

Untermyer “Is not commercial

credit based primarily upon money or property?”

Morgan: “No sir. The first thing

is character.”

Untermyer: “Before money or

property?”

Morgan: “Before money or

property or anything else. Money cannot buy it ... because a man I do not trust

could not get money from me on all the bonds in Christendom.”

The chief flaw with the current regulatory focus on

capital, KBRA believes, is that it ignores important qualitative factors

involved with the ownership and management of banks that ultimately determine

corporate behavior. When banks and non-banks decided to underwrite and sell bonds

based upon subprime mortgages in the 2000s, the level of balance sheet capital

was not at issue. Merely raising the level of capital required for banks may

provide the illusion of progress in the minds of many policy makers, but for

investors the most basic issue involved in any counterparty risk assessment

comes down to trust.

Managing the liquidity of a bank or non-bank

involves not just cash and collateral, but also reputation and transparency.

Measuring the static level of capital on a bank’s balance sheet may provide

some comfort as to enhanced financial stability. Managing liquidity, however,

is a dynamic task that defies easy quantification but is, at day’s end, crucial

to maintaining financial and economic strength. By focusing much of the

attention of regulators and policy makers on the static issue of capital, KBRA

believes, we are not addressing the true qualitative, behavioral issues that

undermined investor confidence in all types of financial institutions and led

to the 2008 financial crisis.

0 comments:

Publicar un comentario