Gold: A Huge Upside Opportunity And Excellent Bet Against Overprinted Dollar

by: Bull and Bear Investor

- I have made a model of gold price, which explained gold rise after abolition of fixed $35/oz rate in 1970s.

- The main model factor is US monetary base, and others are adjustment for world gold production and for US-only consumption.

- The target gold price is $3,750/oz.

- US dollar is overprinted, as US monetary base shows 2 clearly distinctive trends before and after 2008.

- One of the best ways to bet against dollar is buying gold.

- The main model factor is US monetary base, and others are adjustment for world gold production and for US-only consumption.

- The target gold price is $3,750/oz.

- US dollar is overprinted, as US monetary base shows 2 clearly distinctive trends before and after 2008.

- One of the best ways to bet against dollar is buying gold.

Introduction. There have been many talks that gold (NYSEARCA: GLD) should rise in the long-term. The main reasons are that the USA is using artificial fiat money, as well as Fed's policy, and poor quarterly corporate results. I am going to evaluate gold price in terms of artificially printed dollars.

Such approach has been realized by SA contributor Chris Rutherglen. He started with $35/oz gold price in1934 and then forecasted it forward pro rata US monetary base, discounting it at 1.5% rate to account for change in money supply. Eventually, he concluded that gold price should be equal $5,500/oz. Although I appreciate his idea, I think his approach can be improved. The main reason is that gold price is influenced by global world supply and demand, and US monetary base is about America. But what happens when India and China increase their demand; why should it affect excessive US dollar amount in circulation?

Another way to appraise gold is by US monetary base/US gold reserves ratio. It appears that by using this approach, we can stay inside the US story. However, in my opinion, it would only be true, if the US was going to return to gold standard. Otherwise, I do not see how transfers of bullions to and from Fort Knox should influence gold price. In addition, there has been extensive discussion on reliability of US gold storage data.

When talking about monetary base vs. gold, there is one important point needs to be understood: "gold price" should not be understood in its ordinary way. I mean, when we say "oil price is $50 per barrel", we imply that oil is a variable thing and we measure it in 'fixed' dollars (NYSEARCA: UUP), (NYSEARCA: UDN), (NYSEARCA: USDU). It is not the same for gold in our story: we can either say "gold price is higher than it should be", or "too many dollars have been printed for a value of 1 gold oz". I believe that dollar value of gold is much higher than it should be. And a simple dualistic concept of "dollar value of gold" and "gold value of dollar" is needed; because I do not know whether gold will rise against dollar, or overprinted dollar will fall against gold and other things.

How Model Works. Like Mr. Rutherglen, I started from calculating gold pro rata US monetary base. Instead of 1.5% gold production discount rate, I discounted every gold price by actual share of current year's production to total gold production to date. These discount factors actually vary from 1.16% to 2.25%.

We need to understand the "US part of gold and dollar story", not a "world-level story". For each year, I calculated the share of US consumption in world consumption (actually, I was forced to take world production; see appendix for this and other imperfections of my model). Then, for each year, I multiplied draft gold price figure by US consumption share and divided that by average US consumption (total US consumption since 1934/total world consumption since 1934). By doing that I eliminated consumption effect from other countries. Basically, by multiplying draft gold price by US consumption share I "imagined" that all the world gold mining exists to produce gold for US only.

Then, to normalize the figure from "US contribution to gold price" to actual gold price, I divided that by average US share. So, the basic trend is the same, it only oscillates with changes in US consumption.

(Source: various Minerals Yearbooks, author's calculations).

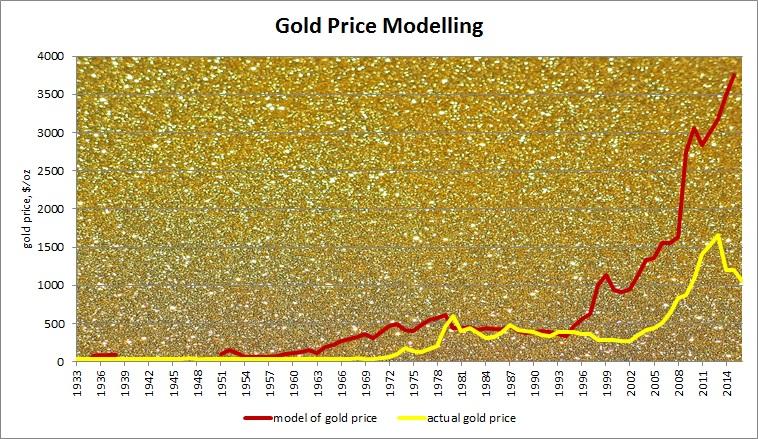

What Model Shows. As we can see, forecasted gold price started to deviate from actual from the very beginning. Since late 1960s-early 1970s it was no longer possible to maintain $35/oz, so gold was left to be priced by a free market. Eventually, gold price started to rise gradually and reached $600/oz. Some people can note that gold price eventually reached its fundamental value, as predicted by my model; others might say that in 1980 there was a gold bubble, and it is just a coincidence. Anyway, one cannot ignore the fact that the model accurately followed gradual gold price decline from $594/oz in 1980 to $350/oz in 1994.

From that point actual and forecast prices started to diverge very significantly. The model gold price's growth from $350/oz in 1994 to $1000/oz in 1999 is mainly due to US consumption share surging from 3% to 10% respectively. Later, forecasted price rose from $1000/oz in 1999 to $1632/oz in 2008, because of monetary base increase from $550 billion to $850 billion, and lowering world gold production from 2,570 tons to 2,290 tons (lowering of US consumption share to 8% did not help).

So, here comes the most interesting part. As we all know, after 2008 crisis US government started QEs (quantitative easing) and ZIRP (zero interest rate policies). Monetary base increased from $850 billion to $4 trillion in 2015. Quite obviously, model gold price soared and reached $3,750/oz; and neither US consumption decrease, nor production increase could change the trend.

The Investment Thesis. Gold should cost $3,750/oz. There are many factors explaining its high price, but the main one is unjustified dollar amount surge. Overprinted dollars, accompanied by investors' fear, should lead to soaring gold prices. Since 2008, if not before, excessive cash has been flowing to the stock market, causing unreasonably high S&P growth. I showed in my previous article that inadequate S&P growth and its deviation from a long-term pattern of S&P/GDP ratio will lead to S&P adjustment.

Dollar and US Monetary Base. Overall, let's have a look at US monetary base since 1934.

I approximated this chart with 2 exponents: before 2008 it is ~exp(0.07*t), where "t" is time in years; and after 2008 it is ~exp(0.205*t). You can say it another way: in 1934-2008 US monetary base has been growing at 7% CAGR (compound annual growth rate), and in 2008-2015 at 20.5% CAGR. Anyway, even without these exponents and CAGRs it is obvious that before 2008 there has been 1 speed, and after 2008 the growth is much faster. We do not need a chart to show that this does not correlate with the real growth of US economy. This excessive money should be utilized somewhere. What is more, I believe that you can't create value by increasing monetary base; therefore, the system should return to equilibrium. This is a bit tricky, because dollar cannot fall by itself, it can only decline against something. Most of foreign currencies are not that "something", because their central banks also pump their economies with the money.

Gold is likely to be that something, so a long gold position would be a good bet against dollar.

Again, you can say it both ways: gold will rise (3.5x in my model) or dollar will fall against gold.

Conclusión. I forecast gold to be $3,750/oz. The analysis is based on growing US monetary base, also taking into account gold production, and considering US as if this country is the only gold consumer. The model has many imperfections, some of which are discussed in Appendix (see below). However, it explains gold price summit in 1980 after fix $35/oz price abolition in 1970s. I believe that we are likely to see similar gold price rally again. We also saw that US monetary base increased its pace in 2008 from 7% p.a. to 20%, and this cannot pass without consequences. The model does not claim that gold should rise exactly 3-3.5x times, it just shows that gold should rise significantly mainly due to overprinted dollars. Putting it another way, gold is currently measured with an "elastic dollar tape", which is stretched at least 3 times from normal. Or, dollar is valued too high, and buying gold is a good way to short dollar.

Appendix. Data and Model Imperfections. Imagine a drunk man standing under the street lamp and looks for something on the ground. The other man comes by and asks, "What are you looking for?".

"My watch", the first man answers.

"Where have you lost it?"

"Under that tree"

"But why are looking for it here?"

"Because under the tree it is too dark"

This is the story I thought of when I was preparing this article. There is no one place for data, it is all scattered through various mineral yearbooks for different years. Of course, methodologies of data collection are not strictly consistent year after year, and I could focus only on clear and understandable line items. Here are some issues:

1) When calculating US share of world gold consumption, I used world production instead of world consumption in the lower part of the fraction. I tried calculating consumption=production-change in reserves, but it did not give consistent data. World reserves are not available before 1960. Also, from 1963 to 1974 world reserves were calculated in dollars ($42 bln. to $50 bln.). When I divided dollar amount to the growing average gold price, it appeared that from 1962 the reserves decreased from 36,500 tons to 8,000 tons, and then suddenly increased again in 1963 back to 36,500. This just doesn't make sense. In addition, for other years calculated world consumption would have unusual incremental high peaks.

2) I skipped 1939 to 1950, as it relies on US consumption in dollars. These numbers are also unreasonably volatile.

3) I used "consumption in industry and the arts" as a figure for US consumption. "Apparent demand", which is basically an investment demand, would be better, but it is not available before 1970s-1980s.

The readers are welcome to suggest improvements to the model (both from conceptual and data collection points of view).

0 comments:

Publicar un comentario