Can Gold And The Dollar Move Together?

by: Andrew Hecht

- Gold has broken higher: Fear with a Capital F = Divergence with a capital D.

- The dollar remains close to the highs.

- The inverse historical relationship.

- There are no rules in this game -- look at historical volatility divergences.

- Fear can drive both higher in unison.

- The dollar remains close to the highs.

- The inverse historical relationship.

- There are no rules in this game -- look at historical volatility divergences.

- Fear can drive both higher in unison.

The best performing commodity of 2016 has been gold, hands down. The yellow metal closed 2015 at $1060.20 per ounce and on Friday, February 26 it was trading at $1224.90 -- an increase of $164.70 or just over 15.5% on the year. With the exception of high-quality government bonds, silver and platinum, everything else has moved lower. This tells me that we are in an environment dominated by fear. The increased interest in gold in 2016 has been the result of a flight to quality. In 2015, gold lost 10.46% of its precious value. In 2016, it has made all that back and more in the first two months.

The U.S. dollar is the reserve currency of the world. Beginning in May 2014, the dollar embarked on a road that has taken the currency higher. The U.S. dollar index futures contract has moved over 24% higher in less than two years. That is a very big move for the reserve currency of the world over a relatively short period of time. There is a historical inverse relationship between the price of gold and the dollar. In 2015, as the dollar moved higher, gold fell. However, given the current state of markets I can make an argument that even if the greenback continues to appreciate, gold can move higher at the same time. This would create a historical divergence, but 2016 has been the year for divergence in markets so far, so why not one between gold and the buck?

Gold has broken higher: Fear with a Capital F = Divergence with a capital D

Recently, Goldman Sachs told us that "the only thing to fear is fear itself" in terms of markets.

Gold immediately reacted by trading down to $1191.50 on the active month April COMEX futures contract on February 16, but since then, gold decided that fear is really the issue these days. Gold closed last Friday almost $34 higher than the lows after the Goldman dispatch and $39 off the recent highs. When it comes to markets, there is still a lot of fear these days; in fact based on the action in stocks, bonds, commodities and currencies during the first two months of the year, what we have is a case of fear with a capital F.

At the same time there is some real divergence within markets. Last Thursday, even though the Chinese stock market plunged, U.S. stocks moved higher led by crude oil, which seems to have developed a pattern lately. Oil has been falling throughout the day, encouraging shorts to come back to the market, and then it turns around in the last hour of trading and moves higher.

Crude oil closed last week at $32.78 per barrel amidst a sea of bearish fundamental data. It was up 82 cents on the week.

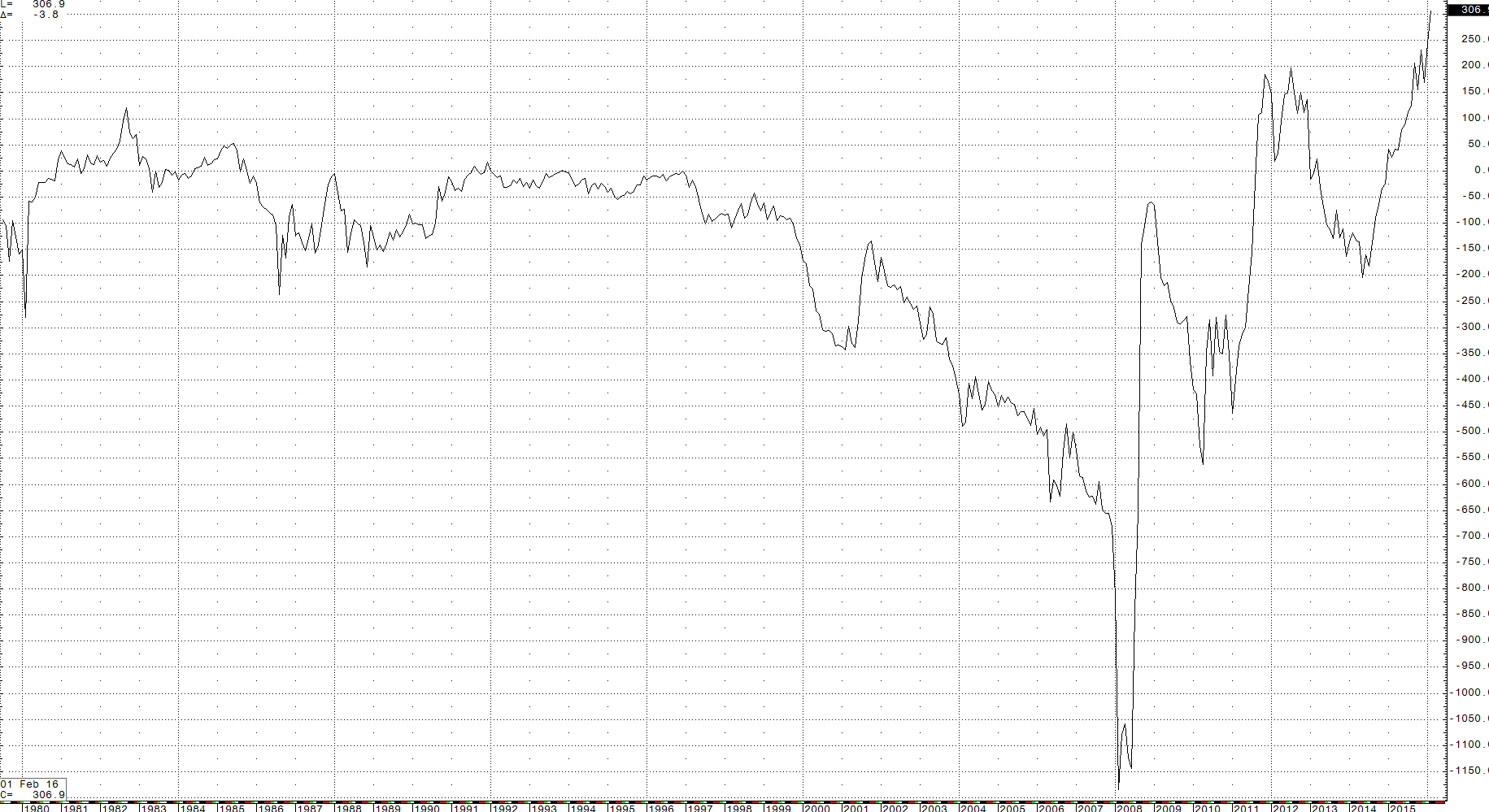

For quite some time, there has been divergence within the precious metals sector. Prior to last September, gold had never traded above a $200 premium to the price of platinum. In fact, in 2008 it was platinum that reached a $1200 premium to the price of the yellow metal. Platinum has always gone by the nickname "rich man's gold," but gold's precious cousin has not traded at a premium to gold bullion since December 2014.

Last Thursday, this spread traded at a new all-time low of a $320 discount for platinum under gold. It is hard to conceive that a precious metal like platinum that is ten times rarer, has a higher production cost and more industrial applications than gold could be trading at such a discount for so long. Perhaps metal is being dumped on the market by Russia, South Africa or possibly a long-term holder disgusted by the price action in what feels like a former precious metal. The current discount of platinum under gold, which closed at around $307 last Friday, qualifies as a long-term deviation from the mean with a capital D.

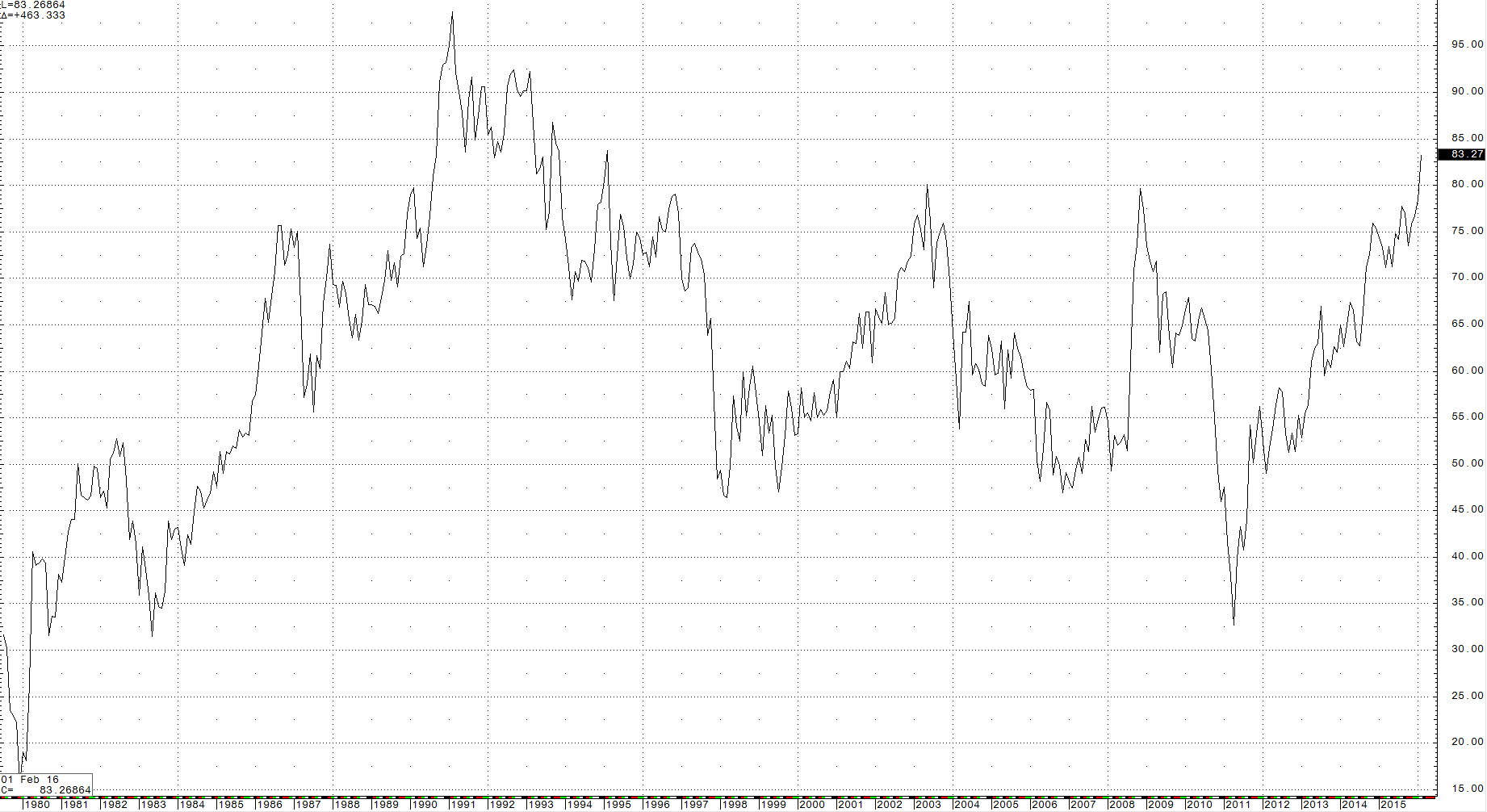

The curious relationship between platinum and gold is validated by gold's relationship with another precious metal, silver. The long-term monthly chart of the silver-gold ratio highlights another divergence in the current saga of the precious metals sector.

Last week silver moved to a new level against gold. The long-term average for this relationship is 55 ounces of silver value in each ounce of gold value. It has now moved above the 83:1 level, closing last Friday at 83.27 ounces of silver value in each ounce of gold value.

Silver closed on Friday at $14.765 per ounce. The current price of gold at $1224.90 suggests a silver price of $22.27 if the relationship were to return to its historical norm. That price is over $7.50 per ounce higher than the current level for silver. And that gold price implies a platinum price of $1424.90 -- $508 over the current price for active month April platinum futures, which are at $916.90 per ounce. These are gross examples of divergence with a capital D. Gold has divorced itself from its precious brethren with yet another capital D.

The dollar remains close to the highs

Meanwhile, the U.S. dollar remains in a trading range for the past year. The dollar index rallied strongly from the May 2014 lows at 78.93 to highs of 100.60 at the end of last November.

As the weekly chart highlights, the dollar index has been in a range between 92.52 and 100.60 for over a year now. It closed last Friday at 98.175 -- closer to the highs of the one-year trading range and its total range since May 2014.

A strong dollar is supported by the fact that the currency pays a rate of interest. The U.S. Fed raised the short-term Fed Funds rate above zero last December. It was the first interest rate hike in the U.S. in nine years. Negative interest rates in Europe and Japan and China's continued interest rate cuts are supportive for the greenback, which at least offers some yield.

The inverse historical relationship

When it comes to commodity prices, a strong dollar is a depressive factor. There is a long-term inverse relationship between the dollar and raw material prices. During the dollar surge, that correlation held and commodity prices moved lower. Gold was no exception. The yellow metal was down over 10% in 2015. However, 2016 seems to be a completely new ball game. Increasing volatility in markets has caused a divergence to appear between gold and the dollar. Now, gold is rallying in all currencies, including the dollar, due to the fear that grips all asset classes.

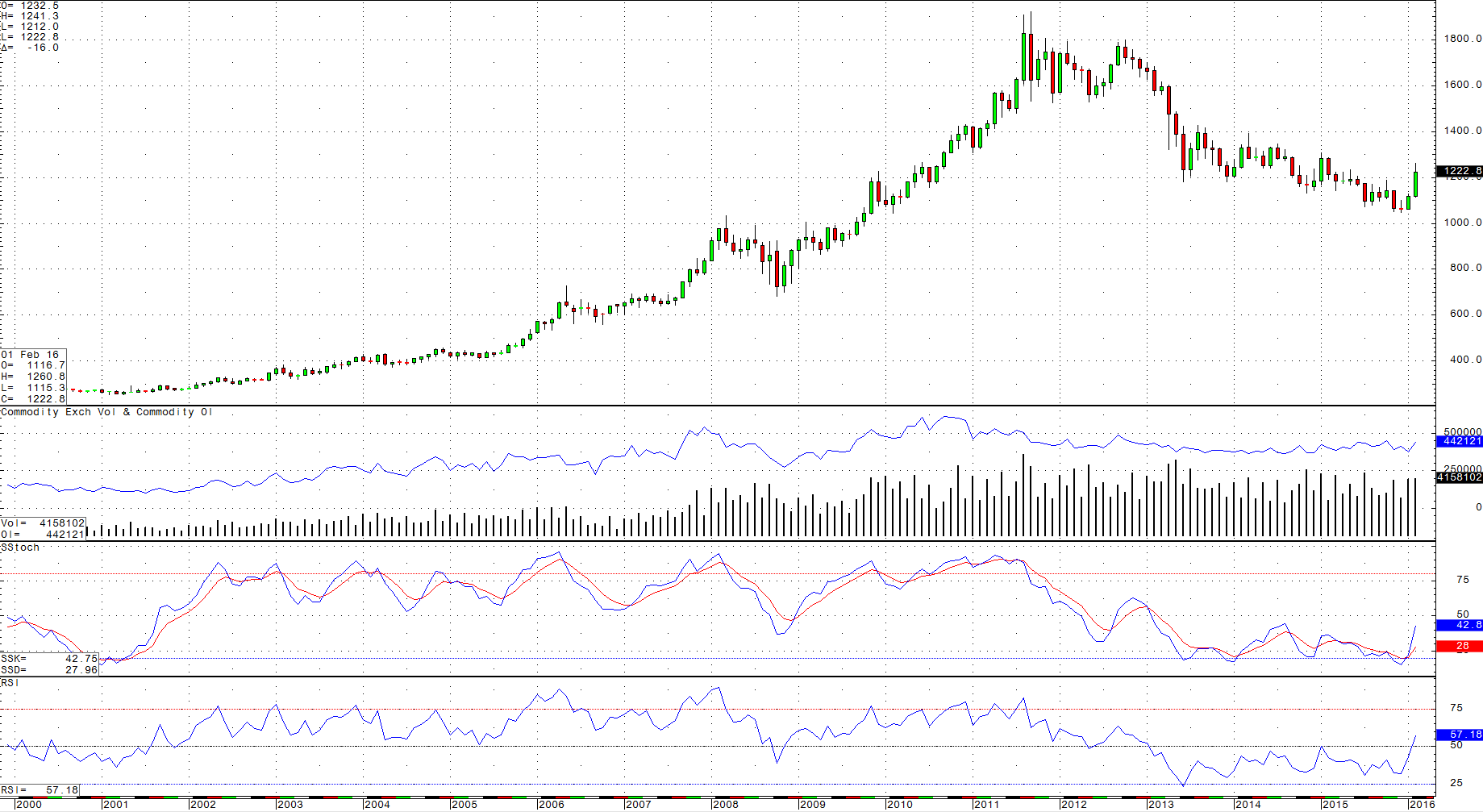

While the daily and weekly charts for gold display an overbought condition, momentum is higher. Additionally, open interest and volume have been rising with price and that is a technical validation of the bullish price action. The real signal that this move in gold is for real on a long-term basis comes from the monthly chart.

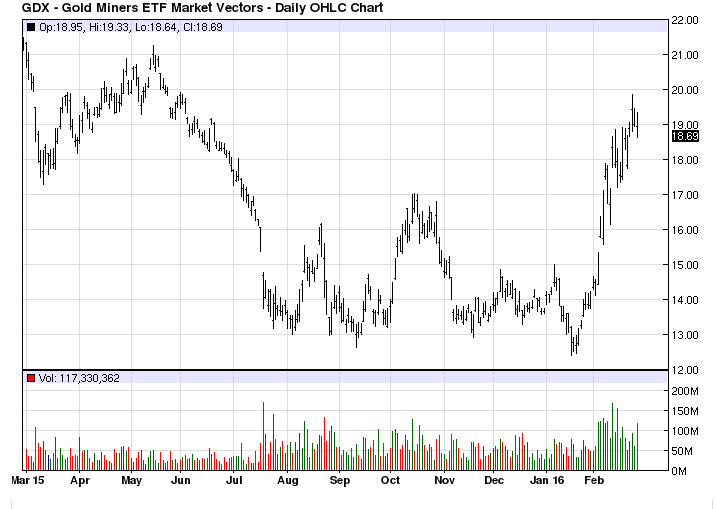

While the rise in open interest and volume is more prevalent on the shorter-term charts, the monthly pictorial of the gold price is compelling in terms of the development of a new trend for the yellow metal. Monthly momentum and relative strength are both positive on this long-term chart. Gold appears to be breaking out of the long-term bear market. In another sign of gold's strength, the equities of gold producers are fast approaching 52-week highs.

The move in the GDX-ETF since mid January has not only been impressive it has been astonishing. Technical strength in the price of gold and gold stocks has been accompanied by a resurgence of demand for physical metal. This is a triad of bullish signals for the yellow metal. All the while, the dollar remains strong and other precious metals, while higher on the year, are not following gold nor are they validating the breadth of the yellow metal's move over the past two months.

There are no rules in this game -- look at historical volatility divergences

I am a huge believer in inter-commodity spreads in terms of their ability to identify value and divergence. It took me a while to come on board the current gold train because of the lack of validation from other precious metals. However, 2016 appears to be a whole new ball game where traditional rules are out the window. After platinum moved to a $320 discount to gold last week, I realized that something much bigger could be unfolding in markets. The flight to quality is clear and Goldman Sachs is wrong about not having fear; gold is telling us to be very afraid.

In an interesting development: as of the close of business last Friday, the daily historical volatility of the price of gold is close to those for platinum and silver. This metric stood at 22.61% for gold, 23.05% for silver and 20.23% for platinum. Under normal conditions, the historical volatility of silver and platinum far exceed the level for gold. In fact, silver tends to trade at 150% of gold's volatility as a norm. Moreover, volatility in the platinum market can be scary at times with gaps and huge intraday moves. This is yet another example of extraordinary divergence within the precious metals sector these days.

When divergences abound, when traditional price relationships move to levels that are extremes and when things do not seem to make sense in markets, this creates a perfect storm for the oldest asset known to mankind -- gold. Right now fundamentals favor both gold and the U.S. dollar. Therefore, given the current environment, both are strong at the same time.

Fear can drive both higher in unison

The current environment of fear is a global phenomenon. In the U.S., moderate growth has caused short-term interest rates to edge higher via the central bank action late last year.

However, the stock market remains at a level that is higher than the norm in terms of price to earnings multiples. At the same time, Europe is an economic mess due to a variety of reasons ranging from unemployment and recessionary pressures to an ongoing immigration crisis. The British currency is falling apart as the nation decides whether to depart from the rest of Europe. Russia, Brazil, Australia and Canada are all suffering economic woes under the weight of low raw material prices. The Middle East is a turbulent region and an economic basket case due to the falling crude oil price. In Asia, Japan continues to show real weakness, while China is slowing, causing a contagious effect on the rest of the continent. Finally, in the U.S., the most contentious presidential election in my lifetime is kicking into high gear.

The bottom line in answer to the question of whether gold and the dollar can both appreciate at the same time? You bet your bottom dollar they can. In fact, given the current state of events around the world and in markets, this is looking more likely every day. Check out my podcasts at Commodix that provide a more in-depth and detailed analysis on the current state of markets.

0 comments:

Publicar un comentario