The Green Shoots of 2020

By John Mauldin

Those who lived through the last financial crisis might may recall

the Green Shoots episode. It drew laughs on March 15, 2009, shortly after the

Federal Reserve fired its heaviest artillery and, we now know, launched the

longest bull market in history.

Appearing on 60

Minutes, Fed Chair Ben Bernanke said the recession’s end was in

sight because the Fed’s asset purchases were generating “green shoots.” They turned out to be slow-growing shoots.

The US unemployment rate kept getting worse for seven more months (peaking in

October), and needed five more years to get where it was when that recession

began

Similarly, you can look around today’s economy and see green

shoots here and there. As bad as things are—and make no mistake, they’re

bad—we’ve regained some lost ground since the March/April depths. But the

problem is in the “here and there” part Some parts of the economy are literally

booming even as others are in a deep, dark depression.

That’s kind of where we are. If you are in the right spot, you see

whole forests of green shoots. You might think they are growing everywhere. And

in due course maybe they will, but for now, a significant number of people just

have dirt.

Last June in A Recession Like No Other I described this recession’s

disproportionately hard hit on the service sector. Most lost jobs came from

industries built on personal contact, like restaurants and hotels. The outlook

for those sectors remains grim. Sadly, the industry is overrepresented in the

lower income brackets. But at the same time, some industries aren’t just

surviving; they are thriving.

I want us to notice this because it’s important. The economy is dynamic. It is constantly moving in all directions. We once talked about “cyclical” stocks that outperform when the economy is expanding, and “non-cyclical” stocks that take the lead in recessions. Now the virus has redefined what the “cycle” looks like, so we have a new set of non-cyclical players. My last few letters were generally negative. Today I want to discuss why the economy will recover, how that will happen and what it will look like. It won’t look like 2019, but the recovery will have its own flavor as we fast-forward future industries I think that’s a good thing.

As we all now know, respiratory viruses spread when people are in close proximity, sharing the same air. The best way to avoid infection is to avoid other people.

Hence the urge, and in some places the requirement, to stay

home as much as possible.

Yet even staying mostly home, people need supplies to sustain

themselves. Furthermore, they continue wanting things that, while not strictly

necessary, make life more comfortable. The problem is how to get those things

without exposing yourself to crowds. The answer: have them delivered to you.

Sounds simple, but it’s economically profound. This year consumers

suddenly and sharply increased their demand for home-delivered goods. For the

most part, these aren’t new products. They are the same things people

previously picked off store shelves. But now they want the goods brought to

them. And, as it always does, the market is responding.

Amazon is the most obvious beneficiary. Its e-commerce platform

and massive logistics network already dominated before the pandemic. Now they

are in overdrive. So are the online arms of major bricks-and-mortar retailers.

Even at the local level, stores are remodeling and reorganizing to provide

curbside pickup.

All these changes come at a cost; smaller retailers often lack the scale or technology to provide what consumers now demand. That’s bad news for those business owners and their workers. But the same economic forces are creating new warehousing and shipping jobs to handle all this new demand.

And

it’s still not enough. From WSJ:

The primary reason for this year’s

capacity shortage is that carriers already have been operating near maximum

capacity for months as consumers stayed home, avoided stores and shopped

online. The delivery surge has strained networks and led to longer processing

and delivery times. Carriers can’t quickly boost capacity with new facilities

as it often requires a multiyear planning process.

The carriers have imposed shipping

limits on customers and added fees to offset the increased costs to staff up,

secure protective equipment and other outlays during the pandemic. Pricing

power has quickly shifted to the carriers, which are raising rates and being

pickier about which shippers they want to do business with.

This is staggering to think about. In the middle of the deepest

recession in generations, consumers are ordering so much stuff, shipping

companies are raising prices and telling some retailers, “Sorry, we can’t do

it.”

Yet, given where we are, it makes sense. Driving a truck around to

drop off packages may seem like a simple job, and there are millions of workers

available. But it’s also dangerous in a new way. Drivers have to come in

contact with both packages and people. That limits the supply and raises its

price. Plus, the companies don’t have an infinite number of vehicles, and they

sometimes break.

The recession and recovery vary a lot. Some segments of the economy are in deep trouble. Others are booming at the same time. This confuses sentiment and adds to the uncertainty and apprehension so many feel.

If circumstances cause you to spend most of your time at home, you

naturally want “home” to be safe and comfortable. That may be difficult to

achieve if you live in a crowded city, where simply taking kids to the park is

now an ordeal. But staying locked inside with them probably isn’t much better.

Particularly if you also fear domestic violence.

Those simple realities are sparking a major migration. City

dwellers (at least those who can afford it) are looking for suburban homes with

yards, pools, garages and other conveniences. Some are moving further out, to

rural areas. Corporations are enabling this with more flexible work-from-home

arrangements, making it possible to live far from the office. In fact, many

people are moving to new states because they can now work from anywhere.

Like the e-commerce boom, this demand surge is overwhelming supply.

Real estate agents like to say “location is everything.” Now it’s “everything”

in a new way no one expected. An easy commute is less important than being far

enough out to be safe, but close enough to get your groceries delivered.

Existing homes in the right places with the right amenities are

selling at high prices because their supply is so limited. Real estate tells us

the supply of homes for sale is down to the lowest level since 1999. But never

fear; entrepreneurs are responding as they always do. From CNBC:

US single-family homebuilding

surged in September, cementing the housing market’s status as the star of the

economic recovery, thanks to record-low interest rates and a migration to the

suburbs and low-density areas as Americans seek more room for home offices and

schooling.

The report from the Commerce

Department on Tuesday reinforced expectations that the economy rebounded

sharply in the third quarter after suffering its deepest contraction in at

least 73 years in the second quarter. But the recovery from the Covid-19

recession has entered a period of uncertainty, with fiscal stimulus, which

spurred the burst in activity last quarter, depleted.

Single-family homebuilding, the largest share of the housing market, jumped 8.5% to a rate of 1.108 million units last month. But starts for the volatile multi-family housing segment fell 16.3% to a pace of 307,000 units.

The drop in multi-family (apartments, condominiums) reflects both

the move away from urban areas and this recession’s inequality. The

lower-income and middle-income workers who tend to live in those places are

taking the brunt of the pain. Many are behind on their rent already and in no

position to move. Developers have little incentive to build more such

properties.

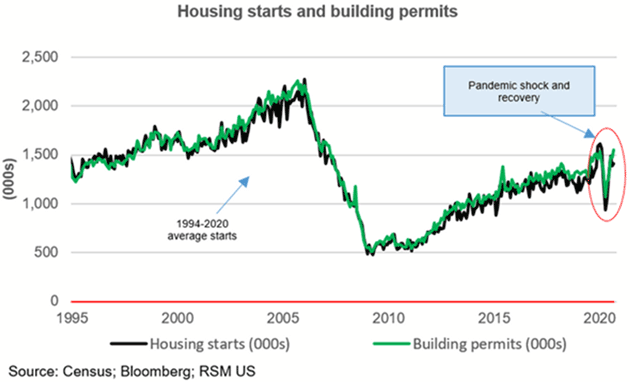

That’s creating an odd dynamic, visible in this chart.

Chart: RSM

In the last two recessions, building permits and housing starts peaked before the economy turned down. And in the Great Recession they kept falling for years.

This time, though, the prior uptrend seems to have resumed

after a brief interruption, even though we are now 8 months into a confirmed

recession.

This wouldn’t be happening in a normal recession. Job losses would be affecting the people who buy single-family homes and builders would be pulling back. Note also, the commercial construction business is in deep trouble even as housing booms, and for some of the same reasons.

People want

houses that let them work from home, but that also reduces demand for office

space. New mall and hotel construction is pretty scarce, too. But it’s a boom

time for skilled workers in the building trades. They are worth their weight in

gold right now, and being paid accordingly.

I talked with demography guru Neil Howe this morning, to get his take on things. One thing that is changing is families are moving back together. He believes this is good as it gets families more involved with each other.

I would note that moving to the suburbs allows you to have more room to work from home and maybe have an extra family member. That is partly why we are seeing a remarkable boom in home remodeling, too.

The items Amazon is shipping, and the materials used to build all

those houses, don’t appear out of thin air. Someone, somewhere makes them. Yet

the pandemic is affecting factory production, too.

It started back in January when China’s massive shutdowns made

much of the world’s manufacturing capacity grind to a halt. Then the same

happened elsewhere. Even if not ordered closed, companies found the new health

precautions and staff shortages both raised costs and reduced output.

The answer to that dilemma is technology. Automation was already

growing simply because paying human workers often costs more than machines that

can do the same work. The pandemic made human workers not just more expensive

but bigger liabilities, too. This increased the incentive to automate.

Meanwhile, new tasks have emerged that are uniquely suited to automation. You can send in a robot to disinfect a room without fear it will get infected itself. But first you need to have the robot, so demand for them is off the charts.

From the Financial

Times:

The pandemic is driving a shift in

companies’ use of technology, both official statistics and business surveys

suggest, making the automation and digitalisation industry one of the few

winners from this year’s economic turbulence.

The spread of the virus “has

accelerated the use of robotics and other technologies to take on tasks that

are more fraught during the pandemic”, said Elisabeth Reynolds, executive

director of the Massachusetts Institute of Technology’s task force on the work

of the future. “It is fair to assume that some firms have learnt how to

maintain their productivity with fewer workers and they will not unlearn what

they have learnt.”

Note that last sentence. If a manufacturer can produce the same number of products with similar speed and quality but fewer human workers, then of course it will do so.

And having made that shift, it will never go back.

That’s why automation is booming and is likely to continue to grow in the

future. Not just robots, but artificial intelligence, virtual reality, and a

host of related areas. And that is reflected in stock prices.

This may be bad news for employment longer term. Employers who install automation will reduce hiring and eventually reduce headcount as well. This will come just as we have millions of unemployed human workers.

And that

is not even counting the coming automation of trucks and transportation. It was

always going to be a problem but might have developed gradually enough to let

everyone adapt. Now the process has accelerated and businesses are more willing

to put technology to work.

But for the moment, recession or not, the robotics and industrial

automation industries are booming. Together with e-commerce and homebuilding,

they are “green shoots” in an otherwise wilted economy.

Another green shoot that is not obvious but will make a very big difference:

We are seeing an increase for the first time in a long time of new business startups. I keep trying to emphasize over the last few months that the very entrepreneurs whose 100,000+ businesses had to be closed (with thousands more coming) won’t just sit on the porch.

They have an entrepreneurial gene in

their DNA that almost forces them to launch new businesses. They can’t help it.

And we are seeing it in the data.

Below I’ll talk about a new business I’m launching. We’ve been working on it for a very long time. It will start with about a dozen jobs. And hopefully grow.

My experience tells me that it will grow slower than I would

like, although I always dream about someday planning a business that would be

like Uber or Airbnb or Amazon, you know, where growth just seems to be

exponential.

Most small businesses start small and grow slow. But some succeed,

and they will create jobs that power the recovery.

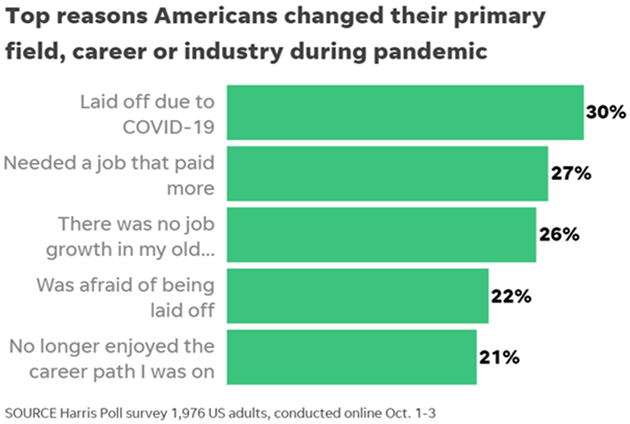

Another interesting development: People are switching jobs and

careers at an unprecedented level. USA

Today has a fascinating story on people switching careers. When you realize your

job will probably not come back, you adapt. We are finally seeing more people

being willing to move outside their local areas to where the jobs are.

Source: USA

Today

Are We There Yet? A Timeline for the Recovery

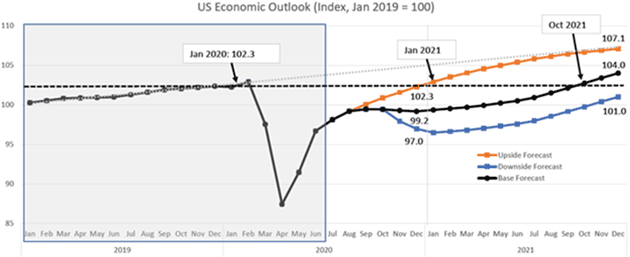

The Conference Board offers us three different recovery forecasts: upside, downside, and the base forecast. Note that in the base case forecast we would be back to January 2020 by October 2021. Color me skeptical. I do think, however, that what they call their “downside forecast” is more realistic.

In that scenario we end 2021 almost back

to January 2020.

Source: The

Conference Board

Their methodology uses past performance to project future results, and I don’t think the past is relevant to this crisis. That being said, I think it would be completely unreasonable not to expect a recovery. This model gives us some idea of what we can expect. I think it will be a little slower as we really do have to completely rearrange much of our economy. That takes time.

In my conversation with Neil Howe, he said the trend is more

people are doing things for each other and spending less money. If that

continues, we will see less GDP growth. Simple illustration: If you find out

that your friend can help you with your hair color and you can help her, you

don’t visit the hair salon as much. Or neighbors helping each other with home

repairs. Since no one is paid, it doesn’t add to GDP, even though the work was

done.

This is critical to understand: Consumer

behavior has changed more this year than any time since the Great Depression.

That’s why we are not going back to 2019. So much has changed that we will be

entering literally a new world.

The point is we will

recover. The airline and hospitality industries will not look the same in 2022

as they did in 2019, but they will be there in a transformed state. Commercial

real estate will be repriced as we continue to work more from home. It seems so

ancient, but just three years ago we bought more food in restaurants than we

made and ate in our homes. That certainly changed and will continue.

Entrepreneurs will adjust.

Will we travel again? Will we eat out again? Will we go to mass

sports events and concerts? Of course. It’ll just take a while (and a vaccine)

to make people feel safe. And it will look different than it did in 2019. But

that’s okay. The world has gone through numerous changes over the last few

centuries and millennia and been better for the adaptations.

I sincerely hope that Congress can figure out how to pass a “recovery package” to help those individuals that still don’t have jobs and businesses that are barely hanging on. My base case becomes more pessimistic without that. That being said, my good friend Renè Aninao, who is truly wired into the relief package negotiations, believes it will happen this next week if not this weekend.

Essentially, he tells me, the last disagreements being worked

out are that Nancy Pelosi wants more money for New York and California and

Trump wants bigger stimulus checks ($1,500 per person, $1,000 per child) than

Pelosi would like to see. Much of the legislation has been written already.

McConnell has most of the votes he needs to be comfortable (certainly not his

majority) and as many as 50 House Republicans may vote in favor. If this bill

passes, it would be fertilizer for the green shoots all over the economy. Let’s

hope so.

Where Then Should I

Invest?

Given all the volatility and uncertainty, successful investing is

harder today than ever. I have been rethinking and actually reworking the ways

that I can help you get from where we are today to the other side of The Great

Reset. I am happy to announce I have found a simple way to access my best ideas

and my network of relationships.

I have long worked with Steve Blumenthal of CMG Capital Management Group (CMG). In the last few years I closed my own investment advisory firm and moved to CMG, where I am chief economist and co-portfolio manager of the Mauldin portfolios platform.

In addition, through my broker/dealer firm, Mauldin Securities, LLC, I’ve selected a broker/dealer, Amera Securities, LLC, (member FINRA/SIPC) to which I can refer you.

The Amera representatives can

show you various offerings like private fixed income and equity and other

alternative investments. Steve Blumenthal and his CMG financial professionals

are also registered with Amera Securities and will, if appropriate, introduce

select ideas to you. So, while you are technically dealing with two firms, you

are dealing with one professional who has access to both.

We have built what we call a “kitchen” where the ingredients are the numerous strategies and managers representing a wide variety of styles and opportunities, which we can blend into a portfolio to help you get a personalized portfolio tailored to your needs.

That means we need to get to know you and your objectives. I am very comfortable with this team and their ability to help you. To find out more about what is in the Mauldin kitchen click here and find out how my network can help you achieve your goals. Do it now. (In this regard, I am president and a registered representative of Mauldin Securities, LLC, member FINRA and SIPC.)

Needing a Neurologist in Tulsa

The letter is already running on, but before I hit the send

button, a personal request. My youngest son Trey has moved to Tulsa for a new

job and to live closer to his sisters. He began to experience serious pain in

his left arm and the local doctors were not really helping. I put Trey on the

phone with Dr. Mike Roizen at the Cleveland Clinic, who upon hearing the

symptoms said Trey should see a neurologist. The problem is his insurance

company is in Texas and can’t or won’t cover it. Even paying cash, we can’t

seem to find a neurologist available. So, we got him Oklahoma insurance but he

can’t see even a primary care physician, and get a neurologist referral until

December. He is in severe pain today. If you know a neurologist in Tulsa please

write me at business@2000wave.com.

Thanks.

Have a great week!

Your hoping your personal green shoot is growing well analyst,

|

|

John

Mauldin |

0 comments:

Publicar un comentario