The Future of the Global Economy

If you establish a democracy, you must in due

time reap the fruits of a democracy. You will in due season have great

impatience of public burdens, combined in due season with great increase of

public expenditure. You will in due season have wars entered into from passion

and not from reason…

– Benjamin Disraeli, prime minister of England, novelist

In any bureaucracy, the people devoted to the

benefit of the bureaucracy itself always get in control, and those dedicated to

the goals the bureaucracy is supposed to accomplish have less and less

influence, and sometimes are eliminated entirely.... In any bureaucratic

organization there will be two kinds of people: those who work to further the

actual goals of the organization, and those who work for the organization

itself. Examples in education would be teachers who work and sacrifice to teach

children, vs. union representatives who work to protect any teacher including

the most incompetent. The Iron Law states that in all cases, the second type of

person will always gain control of the organization, and will always write the

rules under which the organization functions. [Pournelle's law of Bureaucracy]

– Jerry Pournelle, prolific science-fiction writer, August 7, 1933

– September 8, 2017

This letter will be the first of a series in which I outline my

vision for the next 5–10–15–20 years of global economics. I understand that

there is a substantial amount of hubris involved in such an undertaking, so I

will approach the topic gingerly.

Why even risk such prognosticating? As longtime readers know, I am

actually writing a book on what I think the next 20 years will look like,

technologically, geopolitically, sociologically, and economically. The book is

called The Age of

Transformation. The basic thesis is that we are going to see more

change in the next 20 years than we’ve seen over the past century. Consider how

much different the world will be if a century’s worth of change is compressed

into the next 20 years.

If you do not resolve to adapt to that level of change in your

life and in the lives of your loved ones, you will not be ready to fully

participate in the society of 2038. You’ll also fail to reap the full rewards

of all the years of hard work and dedication you have put in, preparing for

your retirement.

This series on the future of the global economy will shape my

outline for the last 25% of the book. The book will expand greatly on this

series. I feel comfortable opening up my thought process to you, and I welcome

the feedback I’m going to get, because it will only improve the book.

Thoughtful comments from friends are always welcome.

The first 40–50% of the book will focus on the technological and

biological transformations that will happen in the next 20 years. In general,

that is the rainbows and puppies section of the book. There are any number of

books out there that deal with this broad topic in different ways, but nearly

all of them have a somewhat techno-utopian slant. And for good reason. Living

longer and healthier in a world of greater abundance, where the things we want

cost less? What’s not to like?

The next 25–30% of the book will deal with the

geopolitical/sociological/demographic changes that will inexorably force

themselves on us in conjunction with this technological revolution. Some of

those changes will be a reaction to the very technological forces that are

driving the change. This section will conclude with the most difficult chapter

of the book, the one that I have wrestled with the longest over the last two years,

the chapter on the future of work. For some of us that will be quite a bright

future; for others who are unable to adapt, not so much. Globally, hundreds of

millions of jobs that are currently filled by humans will simply not require

humans in the future. We will have to move on to other occupations.

This level of labor transformation is nothing that we haven’t done

in the past. Many of you will recall that 80% of Americans toiled on farms in

1800. Today that number is less than 2%, who produce massively more per capita

in much better conditions. But that change played out over more than 10 full

generations. The changes I am talking about are going to happen in less than

one generation. The transformation of employment will be one of the most difficult

social and political problems that societies all over the developed world will

face. It’s not just that there won’t be jobs, but that many of the new jobs

will require different sets of skills and be in a different locations from

where many of us live today. And while our ancestors may have set out boldly

from other corners of the world to give America a try, never to see their

home-countries and loved ones again, that propensity for relocation seems to

have diminished in present-day culture. How many Americans relish the notion of

moving from region to region anymore?

The last section of the book will deal with the future of the

global economy. And there we have some issues, as my kids would say. I don’t

think we end up in some techno-dystopian, cyberpunk Blade Runner-type world,

but the tools we use to measure the economy and the things we are measuring are

going to experience a great deal of volatility. Depending on which side of the

volatility you find yourself on, it may be either extraordinarily beneficial or

harmful. The purpose of my book will be to help you see the general direction

and power of the unfolding transformations, so that you can adapt your

strategies for the benefit of your family, friends, and businesses.

The massive amount of research that I’ve had to work through has

forced me to change my opinions more than a few times as I’ve waded through

material and prepared to put words on the screen. I’m deeply grateful to the

120 volunteer researchers who gave me literally tens of thousands of pages of

material to read and sort through on an extraordinarily wide variety of topics.

I am ultimately optimistic, and the book itself will be optimistic

about the future, but there are difficulties that we as a society will face. We

will have to devise different, and in some cases heretical, ways of operating

in order to bring the benefits of transformation to as many people as possible

in our global society. Make no mistake, political turmoil lies ahead. The

current dysfunction in Washington will seem almost quaint, by comparison, as

the country and the world lurch from one vision of the future to the next.

In trying to predict the future, I feel like a Daniel Boone sort

of explorer, leading a band of compatriots through the wilderness; and we come

to the top of a new pass and peer into the distance. Way off, 50 miles away,

there appears to be another pass in the direction we want to go. The problem is

that, between here and there lie more mountains, valleys, rivers, and potentially

hostile natives. It’s not clear how we get there from where we’re standing. So

our intrepid team plunges on, trusting that our instincts and skills will take

us to that far-off pass, and then to the next one beyond that.

Now we’ve just reached the top of that pass, and we’re peering far

into the blue distance. I’m just trying to get the direction right. The actual

path we’ll take is still a great unknown.

With that thought in mind, let’s survey the main forces that will

drive the future of the economy, and in the coming weeks we will dive more

deeply into each of those forces. What we learn will serve as the backbone for

the final section of the book, which I will write in the coming weeks.

Right up front, I’m going to utter the four most dangerous words

in economics: This time is

different. Oh, I admit a lot of things will be the same, but anyone

who expects the future to look like the past is in for a rude awakening.

There are three main economic forces that are imposing themselves

upon the world, whether we like it or not. Two of them are the largest bubbles

in the history of man.

1. The bubble of global debt

2. The bubble of government promises

3. The shifting of the supply curve

2. The bubble of government promises

3. The shifting of the supply curve

I know longtime readers will be familiar with the first two, but

the last one is going to have a few of you scratching your heads. Let’s take up

each briefly.

There is considerable debate over the exact amount of global debt.

You first have to find it, and parts of it get hidden in many out-of-the-way

pockets. But broadly speaking, global debt is about 325% of GDP, and likely

over $225 trillion as I write. (I am assuming that over the last nine months

debt grew at roughly the same rate as in the preceding nine months, even though

we know the growth of debt has been accelerating.)

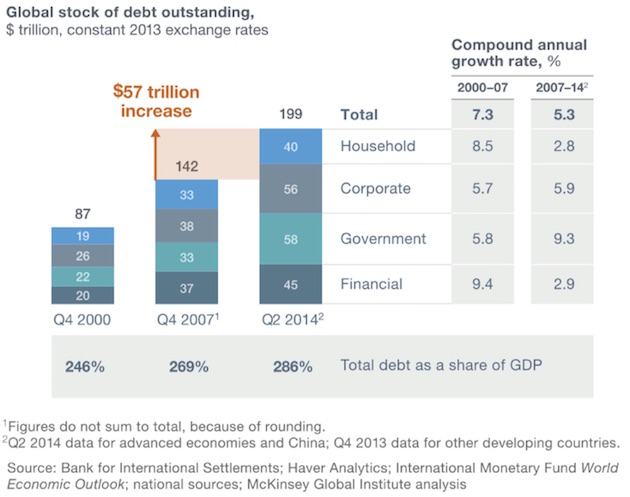

This

chart from McKinsey is almost three years old, but it does show the growth

of debt over time, and we know that global debt has grown by about $26 trillion

in the last two years.

The above chart requires a few observations. First, notice that

the growth of household and financial debt has decelerated. Corporate debt

continues to grow at roughly the same pace as before. The real acceleration of

growth in debt is coming from government borrowing. Second, we are on a pace to

grow the debt by significantly more between 2014 and 2021 than we did in the

previous seven years. Last, global debt is growing faster than global GDP. We

are borrowing money faster than we are creating wealth.

US government debt is about 100% of GDP, or $20 trillion, and

growing around $1 trillion a year. Forget what they say when they talk about

budget deficits. They lie, because they don’t want to admit what the true

deficit is. However, you can determine the true deficit simply by looking at

the amount of money the Treasury has borrowed at the end of the year and see

that another $400–$500 billion of “off-budget” debt has been added. If I ran my

regulated investment businesses with the same sort of spurious accounting, the

SEC and a raft of other agencies would shut me down faster than you can say

“MD&A” and ban me forever from participating in the financial industry. As

they should. You simply cannot lie when you have a public trust. Well, you

can’t unless you are Congress and the government. Then you can pass laws that

allow you to lie. But I digress.

To be able to compare our debt to that of other countries, we have

to include state and local debt, which is another $3 trillion. That means total

US government debt is 115% of GDP. That is certainly less than the 250% of

debt-to-GDP that Japan finds itself saddled with, but Japan does offer us a

clue as to how we are going to have to deal with our burgeoning government debt

in the future. If you had told me 10 years ago that Japan could essentially

monetize well over 100% of their GDP and not have their currency fall through

the floor, I would have laughed at you. (I know, I know, monetize is not the correct

technical term, as the Bank of Japan is simply buying the Japanese debt and

putting it on its balance sheet.) Since the yen didn’t collapse, we start

having to look for other causes and effects. We will get into that in later

letters.

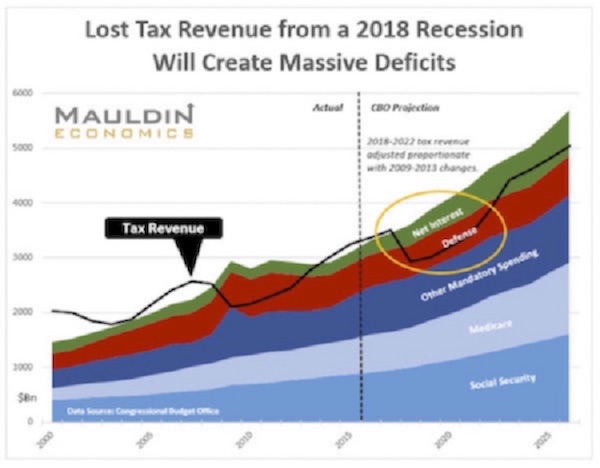

When the next recession blows in, it will likely balloon the US

government deficit up to $2 trillion a year. The Obama administration took

eight years to run up a $10 trillion debt after the 2008 recession. It might

take just five years after the next recession to amass the next $10 trillion.

Here is a chart my staff created in late 2016, using Congressional Budget

Office data, that shows what will happen if the next recession comes in 2018

and revenues drop by the same percentage as they did in the last recession

(without even counting likely higher expenditures next time). And on top of the

$1.3 trillion deficit that this chart predicts, you can add the more than $500

billion in off-budget debt that I mentioned above, plus higher interest rate

expense as rates rise. I will update this chart for the book and later letters,

but it gets the general direction right.

By the early to mid 2020s, barring substantial increases in taxes

or reductions in government benefits and entitlements, the deficit will be

approaching $2 trillion annually. There will be weeping and wailing and gnashing

of teeth.

If you are in the top 25% of income earners in the United States,

you have a big target painted on your income and wealth. The imposition of a

VAT seems almost guaranteed, as that is the only real way to boost revenues to

offset the increases in entitlement spending. And because the Republicans don’t

want to impose a VAT now as part of major tax reform, it will end up being

imposed by a future Democratic administration and congressional majority that

will not be interested in reducing income taxes. I cannot believe the

shortsightedness of the Republican Party leadership, with their futile belief

that somehow or another they are going to develop a “pure” Republican majority

that will look like the current conservative bloc. Their intransigence is the

main reason that things can’t happen in DC. You can simply look at the

demographic trends and political forces at play and understand that they’re not

going to budge on a VAT. Sigh.

We will go into the debt bubble in greater detail, but it is the next

bubble that will drive macroeconomic change in the US.

The US government balance sheet features unfunded liabilities in

the range of $80 trillion to $200 trillion, stemming from future entitlement

program burdens that are, in effect, government promises of future largess. No

constituency is going to vote to reduce their entitlements. (Well, other than

the very well–off, who don’t actually need those entitlements.)

Unfunded pension liabilities at the state and local levels have

swollen to roughly $4–$6 trillion in the United States. And that may be

understating the severity of the problem.

It’s easy to cite Illinois or New Jersey, but let’s look at a

state like Kentucky. The State of Kentucky released a remarkably candid

self-appraisal of their pension liability issues earlier this year. The

report makes for very sobering reading if you are a resident of Kentucky.

If you optimistically (and unrealistically) assume between 6.75%–7.5%

compounded returns for the future, Kentucky still ends up $33 billion

underfunded. To bring that number into focus, total State of Kentucky spending

last year was $32.7 billion, which makes the underfunded portion of their

pension liability larger than the entire state budget. But wait, it gets worse.

They asked themselves, what if we have to assume a more realistic

discount rate for future returns? Assuming returns just north of 5%, the

unfunded portion rises to $42 billion. Assuming a more realistic 4% (given the

likely returns on their fixed-income portfolios), unfunded liabilities rise to

$64 billion, roughly twice the state budget. If you assume a discount rate

equal to the 30-year Treasury rate of 2.7%, the unfunded liability climbs to $84

billion – seven times more than the annual general fund spending would allow.

Now, this is all before we take into account a potential

recession, which has in the past meant an average 40% loss on stock market

equities, which would make Kentucky’s (and everyone else’s) pension woes even

worse. Further, as we shall see in future letters, the massive increases in

debt, both in the US and globally, will make the next recovery and future

growth even more laggardly than the tepid recovery we have experienced in the

past decade.

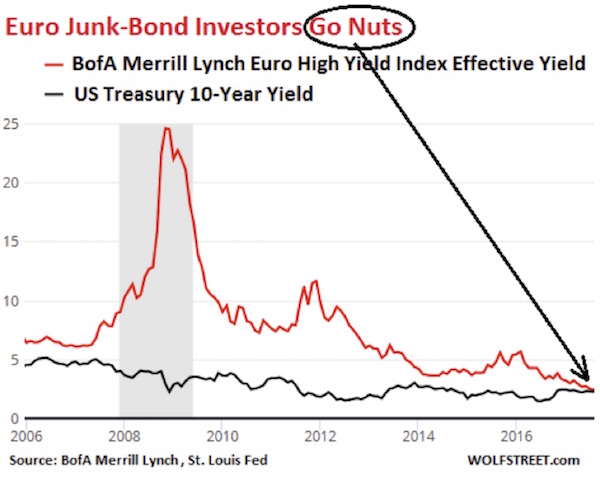

The next financial crisis will not look anything like the last

financial crisis did. But it will rhyme. This next chart depicts an extreme

example of what is happening around the world. Scary levels of junk-bond debt

with covenant-lite options – coupled with the Frank Dodd rules that don’t allow

banks to operate in the corporate bond market as market makers – are going to

mean that corporate debt, from the worst right on up to the best, will take a

massive yield hit, as the flight for cash rhymes with what we saw in 2009.

Remember, in a crisis you don’t sell what you want to sell; you

sell what you can sell.

And at a bargain-basement price. We have monster mutual

funds and ETFs investing in these high-yield corporate markets, and the

redemptions from them are going to force selling into a market where there are

no buyers. If you’re wondering what will push the country into recession, look

to the financial markets. That’s where the excesses are being created. And for

the record, I could spend another four pages showing charts like the one above.

Neo-Keynesian economists in the government and at the Fed have

been doing everything they can to stimulate demand in terms of dollars spent,

believing that they will stimulate a recovery. They are missing part of the

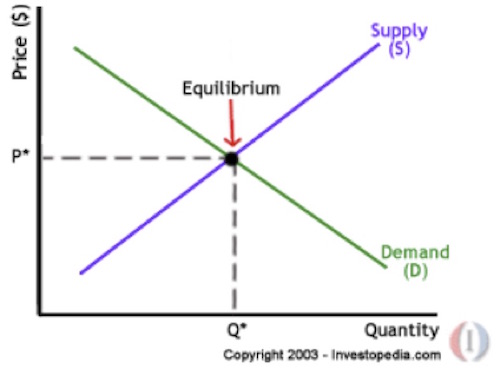

equation. Let’s go back to economics 101 and look at possibly the first graph

you ever saw in that class: the classic supply and demand equilibrium price

graph.

If you push the supply curve to the right, i.e., you provide more

of a particular good, then the price of that good is going to go down to find a

new equilibrium.

I was talking with an economist yesterday who has John Deere as a

client. As he was touring their factory, they pointed that they were making the

same parts for 40% less today than they did just a few years ago. Improved

quality and lower prices.

Everybody latches onto the fact that real wages haven’t risen all

that much in 40 years. Well, if you look just at the standard economic numbers,

that is true. But compare what you could get 40 years ago to what you can buy

today (assuming equivalent purchasing power). Do you think TV quality was

anywhere close to today’s? Telecommunications? Automobiles? Almost everything

is far better today, more abundant, and less expensive than it was in 1977. The

same amount of money today buys a far more desirable basket of goods.

Not to mention that some of those goodies didn’t even exist back

in 1977, like our computers and cell phones. Our automobiles were clunkers that

maybe got 12 miles to the gallon and started to go belly up at 70,000 miles.

And don’t even get me started about the quality of healthcare. We all bitch and

moan about the cost of healthcare, much of which is government-generated, but

oh my, the quality of care is so vastly superior.

Personal example: My family has a history of tinnitus. Mine has

been getting steadily worse over the last 10 years, to the point that I have to

consider hearing aids. I sat down two days ago with my audiologist, who gave me

a loaner pair of hearing aids until the latest and greatest from Switzerland

show up in about four weeks. Those will connect to my iPhone and computer. I

kid you not. And when she began to explain the power of the microchips in those

little devices, I was totally blown away. The amount of real-time,

instantaneous analysis that these hearing aids can perform on the sounds around

you is truly stunning. They can change the output to your auditory nerve on the

fly, depending upon the acoustic characteristics of your situation.

Shane came home, and it was some time before she noticed that I

even had the hearing aids in. You can barely see them unless you’re looking.

Then we went to dinner at the local watering hole and sat outside, where I

admit it has been hard for me to carry on a conversation, and I was amazed at

everything that I could hear.

Or ask somebody about their latest knee or hip replacement. Or

whatever. Anybody who wants to go back to the good old days of 1977 is welcome

to them. Count me out.

Let me wrap up here. I am telling you that in the next 20 years

the amount of high-quality goods that are going to be supplied to the world is

going to drive the prices of almost everything down – except of course the cost

of government, which is only going to go up. Fact: The poverty level in the US

has been flat for almost 40 years, but spending on government poverty programs

is up 900%. Government has no incentive to be efficient. And in fact, as Jerry

Pournelle told us at the beginning of the letter:

In any bureaucracy, the people devoted to the benefit of the

bureaucracy itself always get in control, and those dedicated to the goals the

bureaucracy is supposed to accomplish have less and less influence, and

sometimes are eliminated entirely. [Pournelle's law of bureaucracy]

In any event, the ever-increasing amount of supply is going to be

massively deflationary over time and will offset the massive needs for

quantitative easing and debt relief, etc. We are going to do things in the next

20 years that simply defy our current imagination – mostly because we will be

forced into them in order to avoid utter disaster.

Let me close with this note to the wise. We are putting the

finishing touches on the next Strategic Investment Conference, to be held March

6–9 in San Diego. We are going to spend a great deal of time on these issues

that will be so utterly critical to us as we learn how to steer our portfolios

through future storms. You should look at your calendar and set aside those

dates. We will be accepting early-bird registrations within a few weeks. See

you there.

I want to first thank all my readers who have been generous with

their time and money in helping the victims of Hurricane Harvey. The toll is

staggering, with tens of thousands of homes totally destroyed and another

hundred thousand damaged and requiring repair that will take a long time to

complete. To put this disaster in perspective, if the Houston area were a

country, it would be the 17th largest by GDP in the world.

And now here comes Hurricane Irma. As I work on final edits while

flying to Boston, I meditate on the fact that Florida is even bigger than

Houston. I have been in contact with many friends who are planning to ride the

storm out in Florida, and I will admit I worry about them. And the entire

country will be faced with another large relief effort. Floridians will be in

our thoughts and prayers and hopefully benefit from our efforts and money in

the next few days.

Tomorrow I have to take a quick flight to Boston, where I will

spend a few days. But then I’ll be home until the end of the month, when I fly

up to Chicago for a couple days (Sept. 26–28) for a speech to the Wisconsin

Real Estate Alumni Association. Then I’m off the next day to Lisbon. I return

to Dallas to speak at the Dallas

Money Show on October 5–6. You can click on the link for details. I

will speak at an alternative investments conference in Denver on October 23–24

(details in future letters). I will again be in Denver on November 6 and 7,

speaking for the CFA Society and holding meetings. After a lot of small

back-and-forth flights in November, I’ll end up in Lugano, Switzerland, right

before Thanksgiving. Busy month!

And just for the record, I probably have about one third of The Age of Transformation

done or nearly so. I am not going to set an ETA for the final copy, because I

know the editing and rewriting process is going to be grueling and

time-consuming. There are going to be numerous copies out there for people to

read and provide comments on – either the total book or sections. I want this

one done right.

I was saddened to learn yesterday of the death of one of my

science-fiction heroes, Jerry Pournelle, who has given me so many hours of

reading pleasure over the last (at least) five decades and has contributed some

gems to this letter. Little-known fact: Back in 1985 he was kicked off of

ARPANET, the precursor to the Internet, because he had the temerity to write

about it in one of his columns. Those early intrepid Internet explorers from

MIT? They were all afraid that if Congress found out what they were doing, they

would shut the thing down as a boondoggle, as it was still being funded by

DARPA. The back-and-forth messaging is actually a

hilarious read, as viewed from 2017. But their brainchild was just another

one of those inventions that has radically shaped and improved supply. I doubt

anyone remembers those internet pioneers very much anymore, but in any case,

Jerry Pournelle’s stories will live on for a long time. May he rest in peace

(or stir up a bit of trouble where it needs stirring).

Time to hit the send button. Your assignment is to figure out how

to get to San Diego. As for me, I have to deal with my inbox. Have a great

week!

Your optimistic about humanity but concerned about government

analyst,

John Mauldin

0 comments:

Publicar un comentario