Risks remain amid the global recovery

Financial weakness, debt and fears of a collapse in co-operation are hurdles

by: Martin Wolf

.

The Bank for International Settlements is the stopped clock of international economic institutions. It has argued for monetary and fiscal tightening, whether that makes sense, or not. Fortunately, policymakers, or at least the central banks that are members of the BIS, have ignored its apparent conviction that the world needed an even deeper and more prolonged recession. Yet now, precisely because central banks wisely ignored its advice, a synchronised recovery has finally arrived. So does the latest BIS annual report tell the right time again, as it did in the years before the crisis?

It is worth recalling how wrong the BIS has been in the past. In June 2010, when, as we now know, the post-crisis damage was very much with us, the BIS already asserted that “the time has come to ask when and how these powerful measures can be phased out”. Oh no, it had not.

The time had come to act more aggressively to accelerate the recovery and so limit the longer-term damage of the crisis. The need then was not to phase out monetary and fiscal stimulus, but to strengthen it. The weak recovery is in good part a consequence of that failure.

Yet now things do look different. As Catherine Mann, chief economist of the OECD has stated, things are “better, but not good enough”. The Paris-based club of developed economies, in line with most forecasters, expects a modest pick-up in global growth this year and next. The hope must be that this will be the beginning of a sustained upswing, in which strengthening investment and faster productivity growth keep inflation in check. But hope is what this still is.

So what risks lie in wait for the recovery?

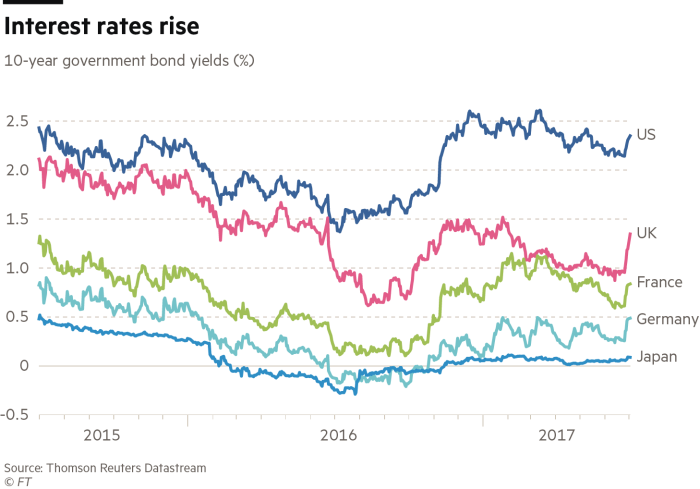

An obvious one is that monetary tightening will be too fast, even in the US, let alone the eurozone. Inflationary pressure remains remarkably subdued. Even the BIS, a worrywart’s worrywart, agrees that resurgence of inflation is not a large risk. This is partly because of globalisation, which has greatly enhanced competitive pressures.

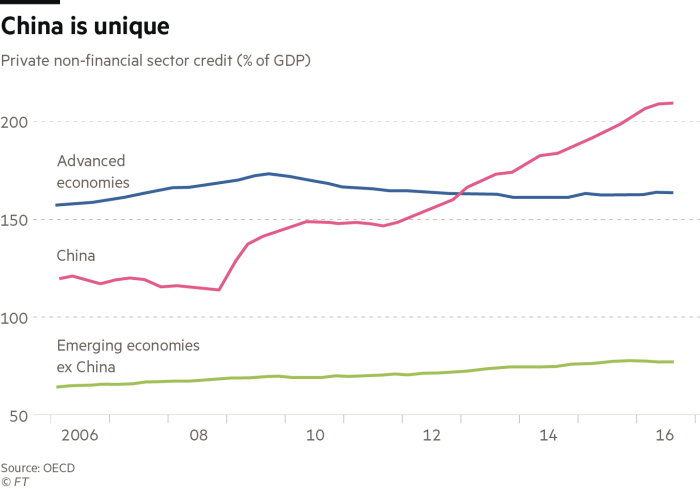

Another risk is financial. As Jaime Caruana, general manager of the BIS, notes: “In a number of smaller advanced economies and emerging market economies, long financial booms have moderated or turned into downswings. And globally, debt is at record levels: in 2016, the stock of non-financial sector debt in the economies [of the group of 20 countries] stood at around 220 per cent of GDP, almost 40 percentage points higher than in 2007.” A striking feature is the remarkably rapid growth of credit and debt in China.

Warren Buffett has said that: “Only when the tide goes out do you discover who’s been swimming naked.” As interest rates rise, financial risks will crystallise. Yet reasons for optimism on this point also exist: the core western financial system is far better regulated and capitalised than it was in 2007; the Chinese authorities can stabilise their financial system, if necessary; no globally significant credit-driven boom is to be seen, except in China; and, finally, even though prices of highly valued equities might fall, that would not of itself cause a crisis in the credit system. If a financial risk exists, it is likely to be in public debt, maybe in the eurozone.

Yet another danger is renewed weakness in aggregate demand. This is one on which, rather surprisingly, the BIS does focus. But, so long as inflation remains subdued, both monetary and fiscal room for manoeuvre remains. Of course, this also argues against premature monetary tightening. Let us establish strong forward momentum first.

The final and possibly greatest danger is a collapse in global co-operation, perhaps even an outbreak of conflict. That would destroy the stability of the world economy on which all — including, though they do not know it, foolish nationalists and protectionists — depend. Indeed, it could destroy the stability of the entire global order. There is no doubt that, as the BIS notes, “formal statistical evidence, casual observation and plain logic indicate that globalisation has been a major force supporting world growth and higher living standards”.

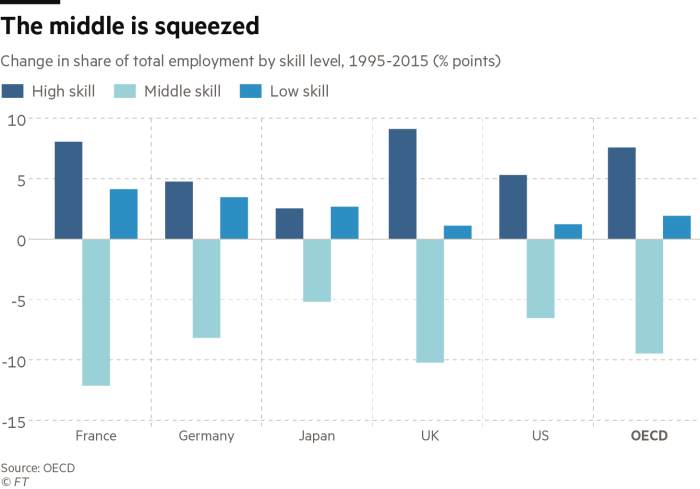

Yet, as Ms Mann rightly says, this indubitable progress has coincided with rising inequality, a concentration of job losses at the middle-skill level and sharp declines in jobs in manufacturing in the high-income economies. That, in turn, has, among other things, led to the protectionism we see, notably in the US.

A collapse of the global political and economic orders could do enormous damage. The assumption, apparent in the markets, that such actions would be “full of sound and fury, signifying nothing” seems remarkably insouciant. It is perfectly possible that nothing much will happen. But it is also possible that the fragile spirit of rules-governed co-operation will simply vanish overnight.

We in the high-income countries allowed the financial system to destabilise our economies. We then refused to use fiscal and monetary stimulus strongly enough to emerge swiftly from the post-crisis economic malaise. We failed to respond to the divergences in economic fortunes of the successful and less successful. These were huge mistakes. Now, as economies recover, we face new challenges: to avoid blowing up the world economy, while ensuring widely shared and sustainable growth.

Alas, we seem likely to fail this set of challenges. The BIS talks, sensibly, of building resilience. A part of this lies in ensuring that growth becomes less dependent on debt. Yet that is only one way in which we need to make our economies more effective and politically legitimate. If we fail to respond to these structural challenges, the recovery is unlikely to prove strong or lasting.

The post-rescue phase is at last quite close. It is a time for reinforcing what was good and reforming what was not.

0 comments:

Publicar un comentario