More on Complexity Economics

John Mauldin

In last weekend’s Thoughts from the Frontline, I talked about how the economics profession in general and central bankers in particular have consistently failed with their economic projections, and I pointed to the need to deepen our understanding of complex systems behavior. I said that we need to marry complex systems theory and information theory in order to establish a new basis for analyzing the economy and creating economic policy.

I couldn’t have been happier, then, when the new issue of Michael Lewitt’s The Credit Strategist popped into my inbox this morning and I found him addressing the same issue. Michael leads off with a discussion of the views of William White, formerly with the Bank for International Settlements (BIS) and now chairman of the Economic and Development Review Committee at the OECD in Paris. (He also spoke at our Strategic Investment Conference last year.)

White, too, has argued that “the fundamental analytical mistake has been to model the economy as an understandable and controllable machine rather than as a complex, adaptive system,” and Lewitt certainly concurs.

OK, so we all agree. But I have to confess, I wasn’t quite satisfied with my own attempt last week to point to a new path forward for economics. It’s one thing to say the economy is complex and nonlinear and another to translate that fundamental understanding into actionable analysis.

And in today’s Outside the Box, I find both Lewitt and White struggling similarly.

Consider these sentences from Lewitt, for instance:

The failure to recognize markets as complex systems led policymakers to adopt the wrong approach to healing the global economy after the crisis. Giving credence to the adage that a hammer views every problem like a nail, they clung to the misguided belief that “growth and job creation deemed to be inadequate are solely due to inadequate demand and that this can always be remedied with expansionary monetary policy.”

Notice how he has immediately jumped from his prescription for complex systems thinking to an entirely mundane statement about the failings of Keynesian economics. You may have found me copping out the same way last weekend!

Lewitt does this more than once. Here’s another example:

Lewitt does this more than once. Here’s another example:

Understanding what to look for requires the proper intellectual frame of reference, which Mr. White correctly argues requires an understanding of complex systems, which require digital not analogue and non-linear rather than linear thinking. The global economy lacks a common anchor of value, leading the value of all financial instruments to be based on a structure of reference rather than relation; in other words, assets are valued based not on their inherent characteristics but on their relative worth compared to other assets.

Well, in the first place, what the heck does it mean to engage in “digital not analogue” thinking? How exactly is digital thinking more nonlinear or better aligned with complexity? What I suspect is going on here is that all of us – Lewitt, White, me, and many others – are just beginning to come to terms with this complexity business. We start to talk about it, and then two seconds later we’re using same tired old economics language we have used for decades. It’s the only language we have! Complexity economics, at this stage, is just very fancy algorithms in very fast computers; it’s not something we can fruitfully chew over and do anything with in our daily work as analysts and investors.

But we’ll get there, and that’s why I’m sharing this piece with you today. I hope you’ll read it, mull it over, and get back to me about it. Let’s share other resources on complexity economics and figure out together how to put it to work.

This week, I find myself deep in the jungle of trying to figure out what the new federal tax policy will be. My fellow explorer Patrick Watson and I have been on numerous conference calls with various people, most of whom are willing to provide background but not actual quotes, although Congressman Kevin Brady (of Texas), the chair of Ways and Means, the House committee where all tax bills must originate, was gracious enough to go on the record. To say this bill is complex is an understatement. It touches EVERYTHING.

I have been in jungles on several continents. Let me just say that this tax jungle is not as breathtakingly inspiring as the Amazon jungle.

Still, There are a quite a number of proposed changes in the bill that give this conservative economist warm fuzzy feelings. Lower and simpler taxes, immediate expensing of equipment, etc. But (you knew there was a but coming) I am having a hard time wrapping my head around the core of the bill. Well that and...

Several things actually. The whole idea is to create jobs, which no one can be against, but what jobs and where? Rather than do the “reveal” on these thorny questions today, they will be the topic of this week’s letter, coming to your inbox over the weekend. The whole jobs question is a big part of my thinking in “The Future of Work,” which I keep saying has been the most difficult chapter to write in my upcoming book on the next 20 years. Are we conservatives like the generals who are always planning to fight the last war? Or are positive human responses to proper incentives part of our core DNA, so that getting the incentives right will work? Are we fighting the future, or making it? Big questions.

They are giving me the signal to get ready to go on stage, so I will hit the send button. Shane and I are throwing a Super Bowl party on Sunday and I will simply say that I want to see a good game that is close, talk with friends and family, and enjoy my chili and Shane's beans and some of the best BBQ in Dallas – and of course guacamole. No diets on Super Bowl Sunday. Have a great week.

Your loving complexity but still stumped by it analyst,

John Mauldin, Editor

Outside the Box

Objects In Mirror Are Closer Than They Appear

By Michael Lewitt

Excerpted from The Credit

Strategist

“The fundamental

ontological error has been to model the economy as a relatively simple machine,

whose properties can thus be known and controlled by its policy operator. In

reality, it is an evolving system, too complex to be either well understood or

closely controlled. Moreover, it is a system in which stocks and ‘imbalances’

build up over time in response to monetary stimulus. This reality makes future

prospects totally path dependent, and we are on a bad path.”

William White1

William White is one of the few policymakers who

foresaw the 2008 financial crisis. Understanding the pathologies that led to

the global financial crisis, Mr. White today rejects the intellectual errors

that mislead so many mainstream economists, pundits and officials regarding the

current state of the global economy. In a recent speech, he criticized

consensus economic thinking and warned that, for all the hoopla surrounding

Donald Trump’s ascension to the presidency, insufficient attention is paid to

the precarious state of global finances.

Mr. White argued that “the fundamental

analytical mistake has been to model the economy as an understandable and

controllable machine rather than as a complex, adaptive system.” As a result,

the decision to solve a debt crisis by printing tens of trillions of dollars

more debt2 means that “the situation we face in late 2016, both in the

advanced economics (AMEs) and the emerging market economies (EMEs ), is

arguably more fraught with danger than was the case when the crisis first

began.” He added, “(b)roadly speaking, the levels of prices in financial

markets today look as stretched as they did in 2007 just before the crisis

erupted.” The global economy is much more leveraged today, central banks’ are

running out of policy responses, and the geopolitical landscape is more

stressed than at any time since the end of the Second World War. I would go

further than Mr. White’s warning, however; global bond markets are in an epic

bubble and stock markets are quickly catching up.

The failure to recognize markets as complex

systems led policymakers to adopt the wrong approach to healing the global

economy after the crisis. Giving credence to the adage that a hammer views

every problem like a nail, they clung to the misguided belief that “growth and

job creation deemed to be inadequate are solely due to inadequate demand and

that this can always be remedied with expansionary monetary policy.” This is

the wrong lesson gleaned from reading John Maynard Keynes though certainly the

most politically palatable one since monetary stimulus delays the necessary

(and painful) cleansing of excesses that economies require to move forward.

Policymakers also developed an excessive fear of deflation and failed to

distinguish between deflation caused by positive factors such as higher

productivity and technological innovation, on the one hand, and deflation

caused by too much debt suppressing economic growth and ultimately inflating

asset values bey ond sustainable levels on the other hand, such as the type we

saw during the financial crisis. As a result, any time they see low inflation

(as they measure it, which has little relationship to reality), they expand

credit with little regard for the consequences. The result is an increasingly

over-leveraged economy whose growth prospects are suppressed by the very debt-

driven policies employed to stimulate economic growth.

Mr. White also makes the extremely important point

that “one characteristic of complex systems is that precise forecasting is

literally impossible.” We rarely hear market pundits say they don’t know where

the market is going despite the fact that nobody knows where the market is

going. Complex systems are non-linear and experience discontinuous change when

forces build up to the point where current conditions can no longer be

sustained. These forces often accumulate gradually and unseen and render the

system more fragile and more vulnerable to abrupt change or crisis. Economic

policymakers are particularly poorly equipped to identify the types of changes

that render economies unstable and vulnerable to crisis because, for the most

part, they are not educated in how complex systems work but are beholden to

static economic models that ignore concepts such as path dependency, non-linear

change and instability.3

The question that all market observers ultimately

have to answer today is whether the epic accumulation of global debt is

sustainable. If it is not, as I believe, the next question is how to identify

the signs indicating that excesses are becoming unsustainable and leading to

breakage. Understanding what to look for requires the proper intellectual frame

of reference, which Mr. White correctly argues requires an understanding of

complex systems, which require digital not analogue and non-linear rather than

linear thinking. The global economy lacks a common anchor of value, leading the

value of all financial instruments to be based on a structure of reference

rather than relation; in other words, assets are valued based not on their

inherent characteristics but on their relative worth compared to other assets.

This is what gave rise to a $600 trillion derivatives infrastructure that

prices the risk of all types of financial instruments based on binary contracts

between counterparties rather than reference to any independently verifiable

indicia of value (and also requires the ability of contracting parties to

perform their obligations). It also divorces market values from fundamental

economic values based on the inherent qualities of financial instruments.

Complex systems are also self-adaptive, which

means they are capable of adjusting to changing conditions. But these adjustments

are often sudden and violent and systems don’t return to their previous state,

leaving those trying to manage them with a new reality for which old models and

modes of thinking are inadequate. This is precisely what happened after the

2008 financial crisis, when policymakers were left facing a much more leveraged

world but failed to adapt their tools to new conditions. Whether the global

economy is capable of adapting to an unsustainable state of over-indebtedness

is dubious; the only question is the timing and severity of the coming

adjustment. As Mr. White warns, we risk learning the answers to those questions

before we are prepared to withstand the consequences. As we are reminded every

time we look in the mirror of our automobile, objects are closer than they

appear. In this case, the forces destabilizing financial markets and rende ring

them fragile and vulnerable to another crisis are staring us right in the face.

But in order to see them, we have to learn to see markets for the complex and

unpredictable systems they are.

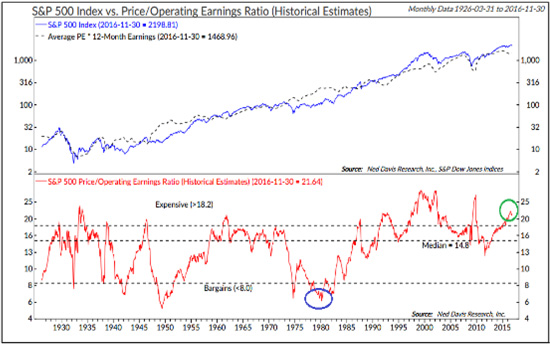

Stocks Are Very Expensive

Markets are chasing the highest valuations in

history. And as usual, they are cheered on by an increasingly puerile

mainstream media. Barron’s didn’t

even wait for the ink to dry on the Dow Jones Industrial Average’s 20,000 print

before declaring in a new cover story: “Next Stop Dow 30,000.” Barron’s argues that “[t]he Dow

hitting 20,000 was no fluke. Today’s stock prices are well supported by

corporate earnings and economic growth. In fact, if President Trump can avoid

stumbling into a trade war – or a real war – the Dow could surpass 30,000 by

the year 2025.” Leaving aside that this National

Enquirer-style headline is a desperate attempt to pump up

readership and is followed by an article lacking a modicum of analytical

substance, let’s take a serious look at claims that corporate earnings and the

economy are strong. The facts tell a different story than the one Barron’s tries to sell.

Corporate earnings have been weak for the last two

years. According to Factset, estimated non- GAAP earnings growth for S&P

companies in 2016 was a paltry +0.1% (and GAAP earnings growth was negative).

Revenues were up roughly 2.0%, which is zero growth once you back out phony

government inflation data and negative if you use real world prices. In 2015,

S&P 500 earnings declined year-over- year on both a GAAP and non-GAAP

basis. But even these figures really don’t tell how poorly businesses are

performing because GAAP and non-GAAP earnings are inflated by low effective corporate

tax rates, low interest rates on the money borrowed to buy back stock and pay

higher dividends, and sluggish wage growth.

US corporations are significantly

more leveraged than they were on the cusp of the financial crisis in 2007, a

condition disguised by record low interest rates that are now rising. So-called

non-GAAP S&P 500 earnings (which are best considered “earni ngs as we would

like them to be” rather than as they actually are) are more than $20 per share

higher than GAAP earnings. With almost half of companies reporting so far for

4Q16, the full year estimate for 2016 S&P 500 non-GAAP earnings is $108.66

and GAAP earnings is $97.98 This puts the market multiple at 21.1x trailing

non-GAAP earnings and 23.4x GAAP earnings.4 By way of comparison, this

multiple was 24x non-GAAP earnings during the Internet Bubble. Other valuation

metrics such as the Shiller Cyclically-Adjusted P/E at 28.4x (versus a mean of

16.7x) and the S&P Market Cap/GDP Ratio of 125% are also at extreme levels.

There are other signs of excess as well such as margin debt running above $500

billion compared to $380 billion at the market top in 2007. Wall Street

strategists trying to tempt investors into buying more stocks at these levels

are playing with fire.

And Dow 20,000 isn’t what it seems. Drawing

historical comparisons between index levels is an inexact science due to the

fact that the composition of these indices changes over time. The composition

of the Dow Jones Industrial Average has changed over time. As economist

extraordinaire David Rosenberg points out, if the eight companies that were

replaced in the Dow since April 2004 had remained in the index, we would be

reading about Dow 12,886, not Dow 20,000.5 Also, as a price-weighted

index, moves in certain stocks have an outsized impact on the Dow, creating

false impressions about the overall strength of the market. For example, moves

in Goldman Sachs Group (GS) have eight times the impact on the Dow as those of

General Electric (GE), a factor that contributed to the index’s post-election

rally. Tracking the Dow may make for good financial television (actually,

nothing makes for good financial television today other than Realvision TV, bu t that’s a

topic for another day), but it is comparing apples and oranges and means little

analytically. All Dow 20,000 accomplishes is getting investors all stirred up

that they are missing a rally. They should be careful what they wish for.

The chase to peak valuations is occurring in a

weak economy. Barron’s claim

that economic growth justifies not only Dow 20,000 today but Dow 30,000 in

eight year is malarkey. Barron’s ignores

the fact that fourth quarter GDP sputtered to 1.9% and kept full year 2016

growth at a disappointing 1.6%, the slowest since 2011 and down sharply from

2015’s 2.6% pace. Last year marked the 11th consecutive year that America

failed to reach 3% growth, the longest period since the Bureau of Economic

Analysis started reporting GDP. U.S. industrial production has declined on a

year-over-year basis for 15 consecutive months and the capacity utilization

rate is a disappointing 75% (a level considered contractionary). And let us not

forget that this tepid growth was boosted by eight years of zero interest rates

and trillions of dollars of QE; without that support, the economy likely would

have shrunk. Claiming that robust economic growth supports hi gher stock prices

is nonsense. Stock prices are primarily supported by cheap money and, as we

will see in a moment, important structural forces in the markets.

Stocks enjoyed quite a run since Election Day. But

even before Donald Trump surprised the world and won the U.S. presidency,

stocks were on an epic run that began in March 2009 at the depths of the Great

Financial Crisis. The most impressive aspect of this bull market is that it

defied the worst economic recovery in the last century and survived eight years

of Obama administration policies that were hostile to economic growth and

markets.6 As noted above, rather than based on a solid economic

foundation, the bull market benefitted from zero interest rates, lower

corporate tax payments, wage suppression and financial engineering in the form

of epic levels of debt-funded M&A, stock buybacks and dividend increases.

These factors have little to do with the fundamental financial condition of

American corporations (in fact, some of these factors weaken their condition).

Eight years later, this leaves the markets (and the individual companies

comprising them) overva lued and overindebted.

But the important question for investors is not

where the market has been but where it is going. Right now, it would be

imprudent to fight the sentiment pushing stock prices higher. Donald Trump’s

presidency represents a sharp break not only with the awful Obama years but the

Bush II administration as well. The new president is laying waste to decades of

failing domestic and foreign policies. It is hardly surprising that investors

are willing to ignore serious structural impediments to growth in order to give

the new president the benefit of the doubt. This sentiment will likely calm

down once the realities of governing within the American constitutional system

set in, but for the moment fighting the tape is a tough gig.

There are also important structural forces pushing

stock prices higher without regard to fundamentals. The question the market

will have to answer is whether the serious valuation, growth and debt headwinds

facing stocks are more powerful than these structural forces that developed

over the past two decades that contributed to stock prices trading today near

their highest valuations of the century. The most powerful structural force at

work is an unprecedented amount of money pursuing a diminishing number of U.S.

stocks. There are roughly half as many publicly listed companies trading on

U.S. stock exchanges today than 20 years ago. The peak of 7,322 public stocks

was reached in 1996; by late 2015 the number was down to 3,700.7 The primary

reason for the decline is massive M&A activity that removed many public

companies from the mix; lesser reasons include the cumulative effects of

private equity firms buying public companies (a subset of the M&A boom) an

d a steady slowing of IP0 activity. Heavier regulation such as the

Sarbanes-Oxley Act passed in the wake of the Enron scandal significantly

increased the costs of being a public company and contributed to more companies

staying private. All of these factors caused the number of publicly listed

companies to shrink significantly over the last twenty years.

While the number of listed companies dropped

sharply, thousands of new ETFs sprang up to take their place. But ETFs do not

create new investment opportunities; they merely repackage existing ones. As a

result, they magnify the shrinkage of available stocks by funneling more money

into the limited number available. Stocks included in the most popular and

largest ETFs attract more capital than those excluded from such ETFs without

regard to their investment fundamentals. This inflates their values beyond what

fundamentals justify. This is how the market became as overvalued market as it

is today. And it is also how markets can stay overvalued for long periods of

time.

But this is only half of the picture. The other

half involves the fact that there is much more money in the world today chasing

this diminishing number of investment opportunities. While the number of stocks

dropped in half over the last twenty years, the global stock of money available

to invest in them exploded as a result of unprecedented efforts by central

bankers to revive economic growth.

These efforts accelerated after the 2008

financial crisis to the point where the world is now home to more than $200

trillion of debt. In addition, there are tens of trillions of dollars of equity

on top of this figure to bring the total stock of money to somewhere in the

$250 trillion range (my very rough estimate). Obviously all of this money is

not chasing equities, but the world is flooded with capital seeking a positive

return, a challenge exacerbated by the imposition of historically low interest

rates by central banks. With bonds reduced to certificates of confiscation t

hat guarantee negative real returns for years to come, money is naturally drawn

to stocks that at least offer the chance of higher returns.

While a more economically enlightened policy

environment may offer a reasonable basis for buying stocks, more money chasing

fewer stocks is arguably a more powerful force. Even if U.S. stocks struggle

with higher interest rates and a strong dollar under the new administration,

the gravitational pull of tens of trillions of dollars of capital looking for

decent returns within a shrinking pool of stocks may make it much more

difficult for a sharp sell-off to occur, certainly one that would last very

long before all that money would come back into the market looking for

“bargains.” This is particularly true in a world where investors are trained to

buy on dips like Pavlov’s dogs.

Right now, the biggest danger to stocks appears to

be higher interest rates. Most observers (at least the ones I respect) put the

danger zone at the 10-year Treasury hitting 3%. I actually think the yield

could hit 3.25-3.5% without sinking stocks if higher rates are seen as a sign

of better economic growth. The Fed is telling people it plans to raise rates

three times in 2017, an aggressive stance to which it is unlikely to stand up.

But even 50 basis points of hikes before year end (my expectation) would push

10-year yields to 3% (assuming the curve doesn’t flatten or invert due to

recession) and closer to the day of reckoning. With American corporations

carrying more debt than ever before, higher rates should worry investors.

But until rates hit the danger zone, the enormous

amounts of money chasing a diminishing number of stocks will remain a strong

force supporting the market.

That doesn’t mean stocks are guaranteed to produce

positive returns in 2017, just that the odds of anything worse than a garden

variety bear market (down 10%) are limited. Further, all that money chasing the

limited number of stocks would likely render any bear market short-lived. This

also doesn’t mean a lot of stocks won’t go down – there are many lousy

companies trading at unsustainable levels. But it remains a stock picker’s

market on both the long and short sides.

President Trump

There is little question that Donald Trump’s

presidency introduces an unusual degree of uncertainty into markets. The fact

that liberals purport to be shocked that Mr. Trump is fulfilling his campaign

promises confirms their cynicism and inauthenticity. The Trump administration

represents a sharp break not only with the disastrous domestic and foreign

policies of the Obama years but the failures of the Bush II administration. Mr.

Trump is an ideological hybrid, borrowing ideas from both progressives on trade

and foreign policy and conservatives on the economy, the Supreme Court and

social issues like abortion and gun control. He is uniquely positioned to run

against both establishment political parties and, most important, to take aim

at the entrenched and corrupt government bureaucracy. He is considered

unpredictable but in fact he is quite the opposite: he does what he says and he

says what he does. If this is considered unpredictable, it is only because

recen t presidential candidates misrepresented their true colors (Obama and

Bush II campaigned as moderates but governed from the far left and far right,

respectively).

The unhinged reaction of the mainstream media,

which Mr. Trump correctly describes as corrupt and dishonest, only confirms

their attempt to disguise rank political partisanship behind a phony First

Amendment curtain. The fact that so many of the so-called journalists who were

actually working behind the scenes for Hillary Clinton and writing false

stories about Mr. Trump and the election are still on the job is inexcusable

(when, for example, is CNBC going to fire John Harwood?). I certainly do not

agree with everything Mr. Trump says or does (though I agree with much of it),

but at least he speaks his mind and backs it up with action. Our country is now

run by generals and businessmen, not by the types of academics and politicians

who made a shambles of foreign and domestic policy over the last two decades.

Before we judge Mr. Trump too harshly, we should give him a chance to implement

the policies that he was elected to implement. The fact that a biased liberal

medi a and half the country doesn’t like him or his policies is irrelevant. By

the time Mr. Trump’s first term is over, the media is going to be a shadow of

its former self if it doesn’t start telling the truth and behaving like the

Founders envisioned, not like a bunch of political operatives.

1 William R. White, “Ultra-Easy Money: Digging the Hole Deeper,”

Adam Smith Priwe Lecture, National Association for Business Economics, Atlanta,

Georgia, September 11, 2016, http://www.williamwhite.ca/content/ultra-easy-

money-digging-hole-deeper. I strongly recommend this paper as a balanced and

sobering analysis of the current state of the global economy from one of the

smartest and most well-informed policymakers in the world.

2 Friedrich Hayek famously warned that, “To combat the

depression by a forced credit expansion is to attempt to cure the evil by the

very means which brought it about.” Friedrich A. Hayek, Monetary Theory and the Trade Cycle,

Martino Fine Books, 1933, p. 21.

3 The work of Nassim Nicholas Taleb speaks to the tendency for

systems to become unstable (he uses the word “fragile”) based on human failures

to think properly about them. See Nassim Nicholas Taleb, Antifragile: Things That Gain From Disorder,

New York, Random House, 2012. On complex systems, see also Marten Scheffer, Critical Transitions in Nature and Society,

Princeton, Princeton University Press, 2009.

4 Peter Boockvar points out that non-GAAP earnings grew by 10.7%

in the last four years beginning in 2013 while the market multiple expanded by

47% (from 14.4x non-GAAP and 15.9x GAAP earnings in 2013). The reason for this

is that central banks reduced the price of money to zero through QE and ZIRP

(zero interest rate policy), radically affecting the discount rate used to

calculate the price at which equities “should” trade. Rather than being

supported by earnings, stock prices are levitated by cheap money and an absence

of intellect on the part of investors. Money is becoming less cheap but

investors are not becoming smarter, a potentially deadly combination.

5 David Rosenberg, Gluskin Sheff, Weekly Buffet with Dave, January 27, 2017, p. 13.

The eight companies dropped from the Dow and their successors are Alcoa/Nike

(2013), Altria Group/Chevron (2008), AIG/Kraft Foods (2008),

Citigroup/Travelers (2009), General Motors/Cisco Systems (2009),

Hewlett-Packard/Visa (2013), Honeywell International/Bank of America (2008),

and SBC Communications/Apple (2005).

6 While nobody should be surprised that Barack Obama never saw

3% GDP growth during his tenure as the economy recovered from a serious

financial crisis, his policies made things worse than they needed to be. Rather

than prioritize economic growth, he pursued policies to more heavily regulate

the economy and redistribute income. In doing so, he failed to help the very

disenfranchised constituencies that voted for him and that he claimed to

champion because he failed to understand the devastating effects of activist

monetary policy and refused to promote pro-growth fiscal policies. While Mr.

Obama will no doubt blame George W. Bush and Republicans for his failures, the

blame lies with him.

7 Craig Doidge, Andrew Karolyi and Rene M. Stulz, “The U.S.

Listing Gap,” NBER Working Paper No. 21181, May 2015.

0 comments:

Publicar un comentario