Italy’s

Day of Reckoning Is Coming

John Mauldin

Italy

has a new government, and Matteo Renzi is not in charge of it. The former prime

minister kept his word and resigned following his constitutional reform plan’s

crushing defeat at the polls. Is all now well in that beautiful land?

Not

exactly, though we did see a glimmer of hope this week. Unicredit, Italy’s

largest bank, announced job cuts and asset sales that may buy it some time.

This does not, however, mean the crisis is over. At best, it means the

beginning of the crisis is over. We have a long way to go.

With

those cheery thoughts, we turn next to the Telegraph’s

Ambrose Evans-Pritchard. He profiles a Milanese professor named Claudio Borghi,

who may well become the finance minister who takes Italy out of the eurozone.

Professor

Borghi is doing the ugly but necessary work of defining exactly how Italy can

restore its own currency. He would begin by launching a kind of parallel

currency alongside the euro.

“The Italian treasury has €90 billion (£76

billion) in arrears on contracts. These could be paid with treasury bonds

issued for as little as €50, €20, €10, or even €5, giving us time to create a

second currency.

“When the time comes we can then switch to this

new currency. It can be done electronically. We don’t even need to print

paper,” he said.

Prof Borghi said the cleanest option is for

Germany to leave the eurozone. If that is impossible Italy can pass a law to

convert its debt obligations into lira overnight – or the ‘florin’ as he

prefers to call it, harking back to the days of Florentine ascendancy under the

Medici.

“The losses would shift to the national central

banks through the Target2 system,” he said. This means the Bank of Italy would

repay €355bn on liabilities to eurozone peers (chiefly the Bundesbank) in

devalued lira. The Bundesbank would face instant paper losses on its credits –

effecting €700bn in the likely event that an Italian exit would lead to a

general return to sovereign currencies.

I

can only imagine the frowns in Berlin upon seeing the line, “the cleanest

option is for Germany to leave the eurozone.” It may well be true, but it’s

hard to imagine any German government agreeing to do so.

Münchau

and Evans-Pritchard are two of the leading economic commentators in Europe. If

they’re this worried about Italy, we should be, too. The first 90 days of the

Trump administration will be important to the near-term fate of the US economy,

but Italy could be more crucial. Italy is a ticking bomb.

I’m

writing this on a plane from New York to Atlanta. I’ll be home in a couple

days, but then I have to turn right around and head back to DC, where we’re

planning an event for the inauguration. I may have more to say on that in this

weekend’s Thoughts from the

Frontline. Meanwhile my shadow complains that it’s having trouble

keeping up with me!

Before

I go, I don't normally mention hotels, but the Melrose Hotel in DC (Georgetown)

is a true gem. A boutique that is rated best value and #2 by Conde Nast, and

even though not expensive, it was first-class with great individual touches.

The restaurant was superb and surprisingly not crowded on a Saturday. Try the

sole or pork. My new DC home.

Your

thinking of Tuscany analyst,

John Mauldin, Editor

Outside the Box

Italy’s rebel economist hones plan to ditch the

euro and restore the Medici florin

By Ambrose Evans-Pritchard

The once-unlikely and remote prospect of an

anti-euro government in Italy is suddenly becoming a real possibility,

threatening to rock the European Union to its foundations within weeks.

Events in Italy are moving with lightning speed.

Key figures in the Democrat Party of premier Matteo Renzi have joined the

chorus of calls for snap elections as soon as February to prevent the

triumphant Five Star Movement running away with the political initiative after

their victory in the referendum over the weekend.

Mr Renzi has not yet revealed his hand but close advisers say he is

tempted to gamble everything on a quick vote, betting that he still has enough

support to squeak ahead in a contest split multiple ways and that his opponents

are not ready for the trials of an election.

It could easily spin out of his control, opening a

way for a tactical alliance of Five Star, the Lega Nord, and a smattering of

small groups, all critics of the euro in various ways.

The man tipped as possible finance minister of any

rebel constellation is Claudio Borghi, a former broker for Merrill Lynch and

Deutsche Bank, and now a professor at the Catholic University of Milan.

“We are coming to the point where Italy must the

make the real decision: are we for Europe or are we against it?” he told the

Telegraph.

“What is emerging is a list of four parties or

groups who all have one thing in common. We all agree that nothing is possible

until we leave the euro.”

“Europe has brought us a depression worse than

1929. It has led to entire peoples being broken and humiliated, like the

Greeks, all for the sake of preserving the infernal instrument of the euro.

This whole disaster has been adorned by a chain of lies, shouted ever louder

because they are afraid that the colossal damage they have done will be

discovered,” he said.

Dr Borghi said the landslide 59:41 result in the

referendum is a shock to Italy’s powerful vested interests, or “poteri forti”.

“They are absolutely scared because none of their tools of control are working

any more,” he said.

“They invested huge prestige in the campaign.

Confindustria [Italy’s CBI], the chambers of commerce, and all of Italy’s big

employers were for the ‘Yes’ side. They said the banks would collapse, that we

would lose all our savings, and that we would all go to Hell if we voted ‘No’,

but it didn’t work. It was Brexit reloaded,” he said.

Professor Borghi said withdrawal from the euro

would be messy but there are ways of mitigating the effects, first by creating

parallel liquidity and letting it seep into daily life.

“The Italian treasury has €90 billion (£76

billion) in arrears on contracts. These could be paid with treasury bonds

issued for as little as €50, €20, €10, or even €5, giving us time to create a

second currency.

“When the time comes we can then switch to this

new currency. It can be done electronically. We don’t even need to print

paper,” he said.

Prof Borghi said the cleanest option is for

Germany to leave the eurozone. If that is impossible Italy can pass a law to

convert its debt obligations into lira overnight – or the ‘florin’ as he

prefers to call it, harking back to the days of Florentine ascendancy under the

Medici.

“The losses would shift to the national central banks

through the Target2 system,” he said. This means the Bank of Italy would repay

€355bn on liabilities to eurozone peers (chiefly the Bundesbank) in devalued

lira. The Bundesbank would face instant paper losses on its credits –

effecting €700bn in the likely event that an Italian exit would lead to a

general return to sovereign currencies.

The sums are in one sense an accounting fiction.

The trial run was the collapse of the Swiss franc peg against the euro in

January 2015. The Swiss National Bank suffered vast theoretical loses on its

holdings of eurozone debt when the franc revalued, but life went on regardless.

The gamble is that large sums held by Italians in

accounts in London, New York, Paris, or Munich, or held in safe-deposit boxes

in Switzerland, would flow back into the system as soon as the boil is lanced,

and once Italy has returned to exchange rate viability. Foreign investors would

view Italy as a far more competitive prospect.

“I don’t see any disaster. There is no way to

smash our currency since we have a trade surplus. If we had a weaker exchange

rate we would have an even bigger surplus,” he said.

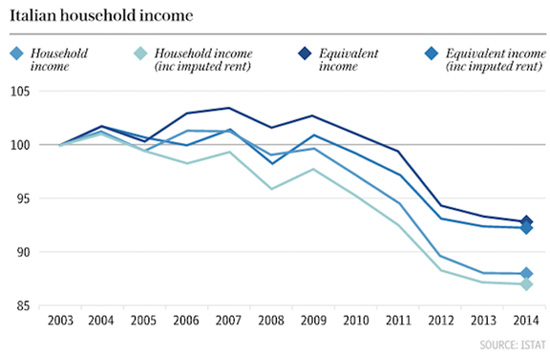

For Italy’s eurosceptics a return to the lira

would be a liberation after fifteen years of economic decay that has hollowed

out the country’s manufacturing core. Industrial output has fallen back to the

levels of 1980. Real GDP per capita is down 13pc from its peak.

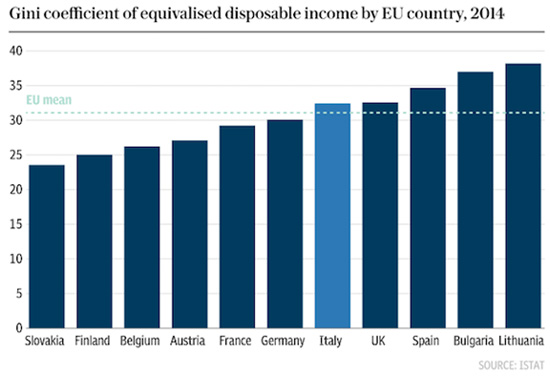

A report this week from the statistics agency

ISTAT said the numbers at risk from poverty and social exclusion last year rose

to 28.7pc, and a fresh high of 46.4pc in South, and 55pc in Sicily – the

epicentre of the ‘No’ vote in the referendum.

A study by Mediobanca found that Italy’s growth

rate tracked that Germany almost exactly for thirty years. The pattern changed

with the advent of the euro, which precluded devaluations and led to a slow but

fatal loss of labour competitiveness – like a lobster being boiled

alive.

This was compounded by the eurozone’s fiscal and

monetary contraction from 2010-2104, a policy error that caused the EMU debt

crisis and led to a double-dip recession. This is turn pushed Italy over the

edge and into a banking crisis.

Exit from the euro would give the country the

fiscal freedom to break out of its deflationary trap, and to save its

banking system with a state-led recapitalization along the lines of the TARP

programme in the US – forbidden under EU state aid laws, unless Italy agrees to

swallow the draconian terms of an EU bail-out.

Prof Borghi said the EU’s new ‘bail-in’ rules must

be swept aside. “As soon you start wiping out savers and bondholders – who did

not behave recklessly – you are telling people that their money is not safe in

the bank,” he said.

“All the EU has achieved is a collapse in Italian

banking stocks by 85pc since last November. You have to step in to save the

banking system in a crisis otherwise everything is destroyed,” he said.

Prof Borghi is chief economic strategist for the

Right-wing Lega Nord, but what is emerging is a tactical alliance between his

party and the Five Star Movement, which has more in common with the Left. The

two together are running at 44pc in the polls. Their economists are working

together in what is becoming a closely-knit school of eurosceptics.

The grass roots of the Five Star party have always

been hostile to pacts with any other group, regarding the whole political cast

in Italy as rotten to the core. But Mr Grillo says the party is closing in on

power and must be prepared to make compromises. “We are in a spiral towards

government,” he said.

Prof Borghi is under no illusion that leaving the

euro can alone solve Italy’s deep-rooted problems, but ’Italexit’ is a

minimum condition. “It is going to be hard, but without our own

correctly-valued currency, we are not going to be able to do anything however

hard we try,” he said.

0 comments:

Publicar un comentario