As

the Fed Turns

By John Mauldin

“Monetary

policy has less room to maneuver when interest rates are close to zero.”

–

Ben Bernanke

“Many

Americans rely on interest income from their savings to help cover their cost

of living.”

–

John Delaney

When I

was growing up – and until I was well into my 60s, in fact – one of the

fixtures of daytime TV was the soap opera As

the World Turns. It was often the highest rated of the soaps, but I

have to admit that I probably watched it only once or twice. Its stars were the

reality-TV celebrities of their time.

Now,

there is a high probability that you too are a soap opera fan, but a soap in a

different genre, though still brought to you by our beloved mass media…

The

highest-rated soap opera ever, at least among those with an economic and

investment approach to life, is the show put on by the US Federal Reserve. I’m

going to have a few things to say about the recent FOMC meeting, and we’ll use

it as a springboard to chew the fat about the new season and upcoming episodes

of our very own soap opera: As

the Fed Turns. Just as devotees of As the World Turns used to speculate about what

their favorite characters were up to, we can have a little fun opining about

the Fed’s next moves. Now, a Trump presidency offers a lot of potentially juicy

drama, too, and we’ll certainly want to chat about it. And of course, we won’t

be forgetting that this is soap opera with real-world implications for the

markets and our investment portfolios.

Very

few things are certain in financial markets these days. We used to be certain,

for instance, that interest rates would always positive be positive. Now we

know that’s not so! But last week we experienced a moment of near-certainty

when federal funds futures contracts said the odds of an interest rate hike

were 95% or better. That turned out to be true.

What

wasn’t certain was what we would hear in Janet Yellen’s commentary and see in

the projections of the FOMC participants. They gave us some things to talk

about, and they even gave us their dot plots; but there is very little that’s

certain in those. In next season’s Fed, executive produced by Donald Trump, those

dot plots will have even less predictive power than they do now. There are some

obvious reasons why the plots are continually wrong, but they’re about to be

more wrong.

What We Learned from As the Fed Turns This Week:

1.

The Fed thinks GDP growth is stuck in low gear.

2.

They believe the US economy is at or near full employment.

3.

Interest rates will rise but not too much.

4.

They don’t want to think about fiscal policy.

5.

Janet Yellen will stick around through 2017.

6.

And the fun part – speculation about the drama surrounding new appointments to

the FOMC. Will Trump get to appoint just two governors or the full monty of

seven? Both scenarios are possible. As in any soap, you need to have some

uncertainty to keep people off balance and paying attention. Trump’s appointees

will make a difference in policy, but will their policy change the reality on

the ground of the global economy?

I’ll

expand on each of the above points. I was travelling or in meetings most of the

week, so I wasn’t able to tune into this week’s drama as it unfolded. I think

that may be just as well. Initial analyst and public response is often wrong,

but it can “anchor” our thinking in ways that aren’t helpful. Sometimes it’s

better to walk into the room late and then just calmly meditate on what you

see.

Promoting

economic growth and employment is one of the Fed’s core missions, assigned to

it by Congress in (I believe) 1974. It was a triumph of Keynesian thought over

Hayek’s beliefs; and despite all evidence to the contrary, most market

participants still think that monetary policy is the magic that drives the

business cycle. Policy is supposed to moderate the boom-and-bust cycle and lift

the economy out of recessions within a reasonable period.

On that point,

monetary policy has failed miserably. We’re seven years out of recession and

have yet to see GDP growth break above 3%.

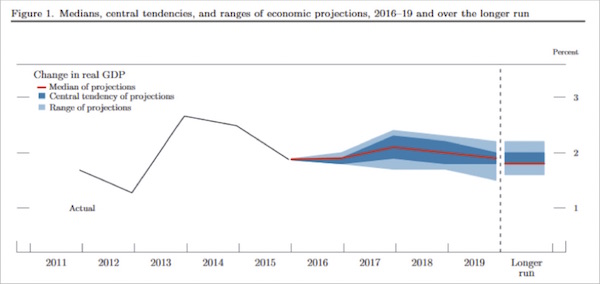

The

Fed’s answer in this week’s episode was to throw in the towel: Expect more of

the same. Here’s actual growth since 2011 and the FOMC’s projections through

2019. Notice that the top end of the range of growth is barely more than 2%.

You

can see that 2013 was a “good” year. Ben Bernanke was confident enough to start

talking about “tapering” down from quantitative easing. Staying on that path

another year or two might have changed everything. But it didn’t. There was a

global taper tantrum; Growth fell back again; and now even the most optimistic

FOMC participants see little chance that it will climb much above 2% through

2019.

(One

caveat – and it’s one that I feel the need to keep repeating: GDP is a deeply

flawed statistical measure that doesn’t fully capture the way today’s economy

works. We use it because we have nothing better.)

Former

Treasury Secretary Larry Summers, who desperately wanted to star in the show

Janet Yellen now headlines, famously called the current trend “secular

stagnation.” He thinks we should all get used to it because its structural

causes are impossible to change. Yellen and her crew might not use language

that strong, but they appear to mostly agree with Larry.

Are

they right? Maybe, but I think we can escape this dreary fate if we play our

cards right.

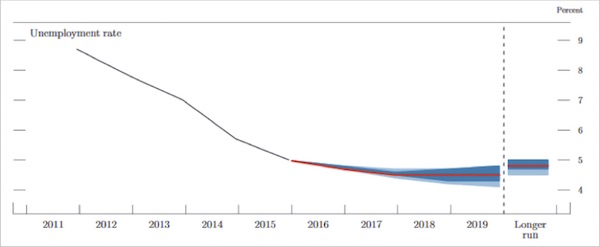

The

unemployment trend is looking better. The rate has fallen pretty steadily and

is now below 5%. The FOMC expects it to stay there, too.

The

problem is that not all jobs are equal. The wealthy law firm partner and the

student-debt-plagued law degree holder who is instead driving for Uber both

count as “employed,” even though their situations are vastly different.

Also

problematic: The unemployment rate is down in part because so many workers have

left the labor force – or, increasingly, never entered it. My airplane reading

this week included a short, fascinating book called Men

Without Work: America’s Invisible Crisis, by Nicholas

Eberstadt. He documents evidence that this abandonment of the labor force isn’t

a new problem, either. It has been quietly building for decades. It has

multiple causes that aren’t at all easily solved. It is likely that I will

write about this book in at least one or two future letters. Eberstadt’s data

is both compelling and depressing.

Roughly

10 million American males of prime working age have literally dropped out of

the workforce. And we wonder why productivity is low. Again, this problem has

been building steadily since the ’60s. The trend has held steady through boom

periods and recessions, and the Clinton/Gingrich welfare reforms didn’t affect

it. France and Greece have significantly higher labor force participation rates

than the US does. And no, these dropouts are not Trump voters, and it’s not

just the labor force they don’t participate in. This is a major and very

troubling social trend.

However,

let’s not overlook progress we have made. We have indeed seen much improvement

from the Great Recession’s depths. Businesses are expanding and creating new

jobs. The problem is that we have a mismatch between the skills of jobless

people and the kinds of work employers need done. That is not something lower

interest rates can solve.

Now to

the main course: Dot Plots du Jour. The dots that the FOMC members contribute

to the plot indicate their expectations for the federal funds rate.

By the

way, I saw a tweet this week in which someone said that the dot plots are not

“forecasts.” It’s true that the Fed doesn’t use that word. They call the plot

their “assessment of appropriate monetary policy” for certain points in the

future. So technically, it’s what they think rates should be, not a prediction of what rates will be on those dates.

Is

that a forecast? You can call it whatever you like. I think “forecast” is close

enough.

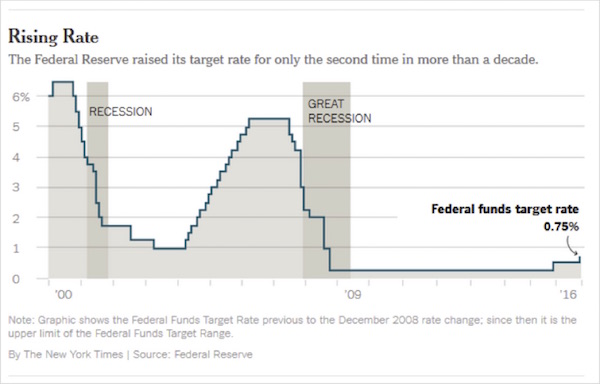

But

before we look at the whatever-you-call-it, here’s a rate history of the last

16 years:

I’ve

highlighted this fact before, but it’s worth mentioning again: In 2007, less

than a decade ago, the fed funds rate was over 5%. So were the interest rates

for Treasury bills, CDs, and money market funds. People were making 5% on their

money, risk-free. It seems like ancient history now, but that year marked the

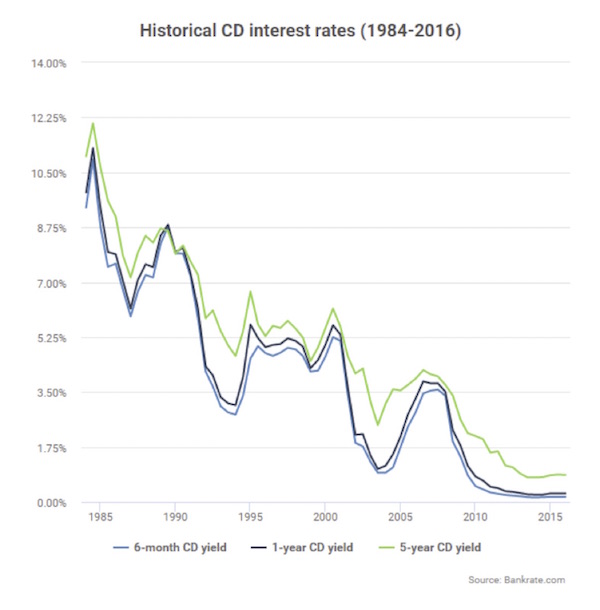

end of a halcyon era of ample rates that most of us lived through. The chart

below shows historical certificate of deposit rates – but remember, you could

put your money in a money market fund and do better than the six-month

certificate of deposit yield, back in 2007.

Today’s

young Wall Street hotshots have never seen anything like that. To them the jump

from 0.5% to 0.75% must seem like a big deal. It’s really not. If the chart

above were a heart monitor readout, we would say this patient is now dead and

that last blip was an equipment glitch.

The

point to all this is that these near-zero rates to which we have all adapted

are by no means normal or necessary to sustain a vibrant economy. We’ve done

fine with much higher rates before. They are even beneficial in some ways –

they give savers a return on their cash, for instance. But there are likely to

be consequences once we embark on this rate-increase cycle, and I’ll examine

them later in this letter.

The

FOMC cast members are all old enough to remember those bygone days of higher

rates as well as I do. So we would think they might at least foresee a return

to normalcy at some point in the future. Not so. They see nothing of the sort.

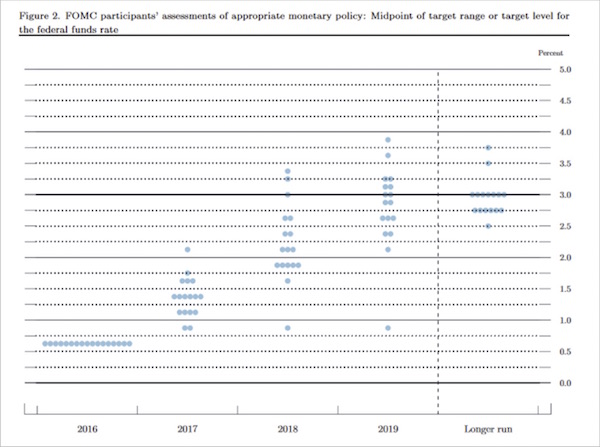

Here

is the official dot plot published by the FOMC. (I have included their

preferred heading so that no one complains about my calling it a forecast, even

though that’s what it is.)

Each

dot represents the forecast assessment of an FOMC member. That group

includes all the Fed governors and the district bank presidents. All 17 of them

submit dots, including the presidents of districts who aren’t in the voting

rotation right now.

There would be 19 dots if the two vacant governor seats had

been filled.

That

flat set of dots under 2016 represents a rare instance of Federal Reserve

unanimity: They all agree where rates are right now. (See, consensus really is

possible.) The disagreement sets in next year. For 2017 there’s one lone dot

above the 2.0% line, but the majority (12 of 17) are below 1.5%.

Nevertheless,

it will be a much different year than this one if they follow through. The dots

imply that the fed funds rate will rise a total 75 basis points next year.

Presumably, that would be three 25 bps moves, but they can split it however

they want. They could ignore their expectations completely, too. This time last

year, the FOMC said to expect a 100 bps rise, or four rate hikes, in 2016. We

got only one.

Follow

the dots on out and you see that their assessments trend a little higher in the

following two years, and then we have the “longer run” beyond 2019. Most FOMC

participants think rates at 3% or less will be appropriate as we enter the

2020s. The most hawkish dot is at 3.75%.

Think

about what this means. Today’s FOMC can imagine raising rates only to the point

they fell to about halfway through their 2007–2008 easing cycle. They see no chance that overnight rates

will reach 5% again. None.

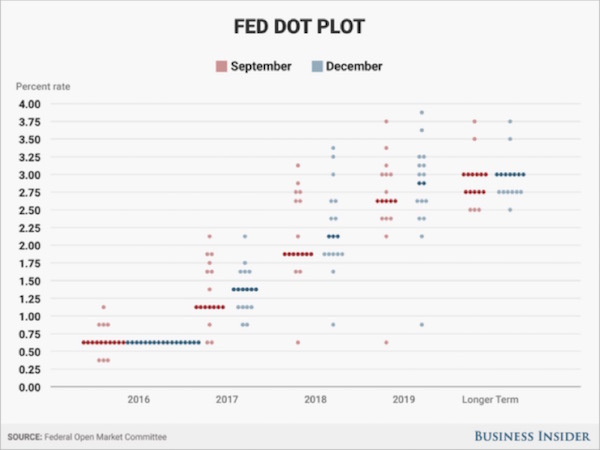

Here

is another view of the same data, courtesy of Business Insider. They added the September dot

plots, so we can see how the dots shifted.

Looking

at each set of red (September) and blue (December) dots, we see only a slightly

more hawkish tilt than we saw three months ago. The “Longer Term” sets are

almost identical – two of the doves moved up from the 2.5% level, while the two

most hawkish hung tight at 3.75% and 3.50%.

That

word hawkish is

relative here. By 2007 standards, these two voters are doves. But, Toto,

I’ve a feeling we aren’t in 2007 anymore.

I got

an email from the brilliant Peter Boockvar after the FOMC news. He said, “If

something changed on November 8th, the Fed didn’t see it.” That was

a good way to put it. The same election that jolted markets into some of the

sharpest moves in years barely affected the FOMC participants. That’s very

clear from the near-identical red and blue dots in the chart above. Peter’s

take?

Now

the dots predict 3 in 2017, and the market this time actually believes we may

get it because of Trumponomics and the reality that Fed forecasts must shift

higher.

Three rate hikes, though, will only take us to a whopping fed funds

rate of 1.375%.

Even with a zero rate for 8 straight years, the 25-year average

in the fed funds rate is still about 2.75%. Headline CPI today is expected to

print 1.7%. We should still see negative real interest rates in 2017. The

dollar doesn’t care about the absolute level of rates as it continues to rip on

the continued growing rate differentials. I’m waiting for the Trump tweet

complaining about the strong dollar. I find that to be inevitable if he wants

to bring manufacturing jobs back to the US.

Are

the Fed governors and bank presidents in denial? I don’t think so. Whether they

supported the election outcome or not, they know what happened. They know how

markets reacted. They know a whole bunch of things are about to change. So why

are they so stubbornly sticking to their guns?

This

may surprise some of you, but I’m going to defend the Fed on this point.

I

wholeheartedly believe Donald Trump and the Republican majority will enact a

sweeping package of tax cuts, at least a modest infrastructure spending

program, and hopefully some radical deregulation. It won’t be exactly what any

of us want, but they’ll make some good moves that should help the economy,

which is badly in need of some help. (As we will see below, there are other

forces that are problematic.)

But

here’s the rub. We don’t

yet know exactly what it will all look like. Right now, we’re

hearing a lot of ideas and speculation. Presidents never get everything they

want from Congress. Trump may get more than most, but I doubt he’ll get it all.

Senators and Representatives have their own ideas and incentives. Serious

prognosticators are paying a lot more attention to House Ways and Means

Chairman Kevin Brady than the media is. Brady’s ideas are well-known, but

they’d be a radical departure from current policy. And every economist knows

that any change comes with a time lag before its effects are truly seen in the

economy.

Likewise,

the details matter. Tax reductions are generally good, but they can have more

or less growth impact depending how they are constructed. There’s also the

question of how they will affect the debt. That problem isn’t going away. The

same with spending and deregulation.

There’s

a lot we don’t know, and right now what we do have is mostly guesswork. Do we

really want a Federal Reserve that reacts to guesswork? I don’t. I want them to

look at hard data and make their best judgment calls. This week’s hike was

probably going to happen no matter how the election turned out. They told us in

the dot plot to expect more hikes next year, totaling 0.75%. They have plenty

of time to react to whatever fiscal policy changes make it to the president’s

desk.

The

same applies to their morose GDP projections. Do they think the coming changes

will have no effect? Probably not. But they don’t know exactly what the changes

will be, which makes their impact hard to assess. Plus, while I don’t agree

with Summers on secular stagnation, I do agree that long-term forces are

causing a generally slower growth environment.

We’ll

get a new dot plot at the mid-March FOMC meeting. By then we should have a much

better sense of fiscal policy changes. I suspect the impact will be visible in

that meeting’s projections, and certainly by the meeting in June.

The

current FOMC may have some new voters by March. There are two vacant seats

Trump can fill as soon as he takes office and gets the Senate to confirm them.

But it appears Janet Yellen isn’t going anywhere. Asked about her own future at

the news conference, she noted that the Senate had confirmed her to a four-year

term as chair and that she plans to finish it on schedule, that is, on February

3, 2018.

And

this is where we get some drama. Trump could have anywhere from a minimum of

two appointments in his first term to possibly all seven. We’ll start with some

facts and then throw in some speculation. I should note that I have talked

about this with a number of people who have deep insights and contacts in the Federal

Reserve, but I owe a special word of thanks to Danielle DiMartino Booth, whose

new book on the Fed will be out on Valentine’s Day. We will preview it here,

and I’m sure it’s something you’ll want to read. It is getting rave reviews

from the coterie of insiders she has allowed to read it. Now to the drama…

At

Yellen’s press conference she made a couple of notable points. She specifically

noted that Federal Reserve appointments aren’t tied to presidential elections.

I think that was a hint that she will defend the Fed’s independence, or at

least try to.

She

also left open the possibility of staying on the Board of Governors even after

her term as chair is over. Those are separate appointments. She can stay on the

board until January 31, 2024. At age 70 now, I doubt she will, but it’s

possible. We know Supreme Court justices delay retirement so that a president

they like can appoint their successor. I think Yellen was reminding Trump that

she has that option.

The

same is true for Vice Chair Stanley Fischer, by the way. His board term lasts

until January 31, 2020, so if he chooses to stay it will be until either

Trump’s second term or someone else’s first .

You

all know that I think the Fed needs a major shake-up. I think Trump can do it,

too, but only to the extent there are vacancies he can fill. There are the two

current openings, but beyond them he will need some of the current five

governors on the FOMC to step down voluntarily. The others’ terms all extend

through 2022 or later.

For

the record, the other three serving Board of Governors members are Daniel

Tarullo, whose term does not end until January 31, 2022; Jerome Powell, whose

term isn’t over until January 31, 2028; and Lael Brainard, whose term ends on

January 31, 2026. They can all elect to stay.

Now, I

am told that Yellen actually wanted to raise rates in September but that she

would have had two dissenting votes from members of the Board of Governors.

It’s one thing to get dissenting votes from the district Federal Reserve

presidents who are serving as voting members on the FOMC; it’s another thing to

get dissenting votes from the members who are appointed to the Board of

Governors. There has not been a dissenting vote from a governor since 1996 –

not to say it couldn’t happen next meeting, but just to give you an idea how

rare it is.

If

Yellen and Fischer decided they wanted to stay and the other three current

board members also agreed to stay on, together with the generally dovish

district Federal Reserve presidents, they could seriously hamstring any real

shift in Federal Reserve policy that Trump might prefer.

That

means the two appointments that he initially makes may be his only true options

to eventually become chairman and vice chairman. While I don’t think this

outcome is likely, is clearly an option in everybody’s back pocket. That

ratchets up the importance of the first two appointments.

Fortunately

for Trump, it’s pretty rare for Fed governors to complete their full 14-year

terms.

First of all, you have to realize that they get something like $169,000

a year. That’s a rounding error in their speaking income, not to mention what

they can get by sitting on major corporate boards and consulting. And

seriously, you have to be a total data wonk to get any excitement out of some

of the responsibilities they have. So consequently, they either retire or seek

other opportunities (and maybe a bit more fun). So there’s a good chance Trump

appointees will hold at least four of the seven Board of Governors seats by the

end of his first term. That could happen as soon as mid-2018 if Yellen and

Fischer retire when their leadership positions end.

Okay,

let’s ratchet up the drama. Lael Brainard was hoping to be appointed Secretary

of the Treasury under a Clinton administration. Clearly, that’s not going to

happen. She’s young enough that a future Democratic president could appoint her

to the position, but does she want to hang around on the Federal Reserve for a

minimum of four more years? I am told she doesn’t.

By

people who know Governor Tarullo (and like him), I am told that he is likely to

leave sooner rather than later. Currently, he is head of the Federal Financial

Institutions Examination Council, a spot he is certainly qualified for but one

that is generally given to the Federal Reserve vice chair. He is 64 years old,

and I don’t think he will want to hang around just holding down a spot.

Jerome

Powell’s background is impressive, but I wonder if he would want to be the

last man standing of the current governors. I have heard nothing either way and

no one seems to really know, other than Governor Powell. He is actually the

lone Republican on the board but has not proven as hawkish as some people

thought he would.

Also

for the record, I know that both John Taylor and Kevin Warsh would like to be

Fed chairman. Either one would be a good chairman, but my true preference would

be Richard Fisher, the former Dallas Federal Reserve president. The coming

times are going to be extremely difficult to navigate by the limited means of

monetary policy, but within that scope, the wisdom and counsel of Richard

Fisher would be a great addition. There are any number of good governor

nominees, but let me put the names of Dr. Lacy Hunt and David Malpass on the

list. Especially Lacy. True aficionados of the genre know that these two are

not always on the same page, but they both bring an enormous amount of

historical knowledge and economic sagacity. We are coming into a world where

there will not be many good choices, and choosing among the – well, let's just

call them less than optimal – choices will demand that wisdom. Just saying…

So

it’s possible that Trump gets at least six and maybe seven appointments within

his first two years to the Board of Governors of the Federal Reserve.

Even

if you like nothing else about Donald Trump, you really should celebrate this

part. The stars

have lined up to give an “outsider” president a shot at completely remaking the

Federal Reserve. Washington is full of agencies that need a shake-up, of

course. I expect many will get one. None need it more than the Fed. In terms of

long-term impact, reshaping the Fed could be one of Trump’s greatest

undertakings.

That

being said, if he gets the number of appointments that I think are likely, that

means he “owns” the Fed, in terms of having to take responsibility for its actions.

It goes back to Colin Powell’s philosophical line, “You break it, you own it.”

The

problem is, as I have been repeating, that monetary policy is unlikely to be

all that effective in the future. It is questionable how effective it has been

in the recent past, aside from driving up asset prices, which hasn’t done much

for Middle America.

I keep

pointing out that we really do have to be paying attention to what is happening

in Italy and Europe, too. Italy is truly on the brink of a major crisis. Maybe

I should write that as MAJOR

CRISIS. One that can send Europe into a deep recession and

push the world to a global recession.

Let’s

review the reality on the ground. In a conversation I had yesterday with Dr.

Lacy Hunt, he pointed out that total US debt is $70 trillion. $20 trillion of

that will have its interest rates reset within the next two years. That means a

minimum of $200 billion more interest, which comes directly out of the

productive economy. Now, that money is partially transferred here or there, but

it is clearly not stimulus. As I have demonstrated in past letters, at some

point debt becomes a drag on the economy, and we are at that point.

Further,

and without getting too deep into the weeds, the QCEW (an employment report)

suggests that the actual number of added jobs in the US may be overstated by

190,000 or more and will get adjusted next year when we get the normal

revisions. And as I mentioned, 10 million American males are no longer in the

labor force and aren’t looking for work. No productivity or any other help for

the economy there.

The

bulk of the current FOMC members believe that GDP growth will remain below 2%.

There is reason to think that 1.5% is closer to the real potential. For all

intents and purposes, that’s stall speed. A crisis in Europe, and President

Trump has a recession on his hands. And as I have consistently pointed out for

20 years, presidents have *&^%&^% little control over the economy – but

they get blamed or praised, take credit or point fingers, for whatever happens.

Whatever

happens, it is going to be an interesting next four years. Let me make a

personal admission. This will probably earn me no kudos from anyone, but in my

private moments over the summer and going into the election, I consoled my

friends with the possibility that while Republicans might lose at the ballot

box, the fact that the likelihood of a recession in the next four years was so

high that a Clinton presidency and progressives in general would be blamed for

it. Blamed unfairly, at least to some degree, although they are responsible for

the regulatory environment we live in today. But this would lead to a massive

sweep in 2018 and 2020 and in the long view might change things for the

following 10 to 15 years.

Now?

Republicans own it. At least in the minds of the voters. And for the record,

let me clearly state that the policies that I expect a Republican president and

Congress to initiate will go a long way to mitigating the negative effects of a

recession, far more than the dovish and more repressive regulatory and high-tax

policies of a Clinton administration would have done. But arguing that things

are at least better than they would have been does not make for a very good

political campaign slogan.

To an

agonizingly great degree, the incoming US administration is hostage to the

German election cycle, which means that Merkel cannot condone bailing out

Italian banks until after her election in the fourth quarter of next year.

Sometimes, bond markets can be very inconvenient. Italy is in extremely deep

kimchee. And that’s putting it delicately. Unlike Greece, Italy matters. Italy

is too big to bail out, too big to save. A breakup of the euro practically

guarantees a deep recession in Germany – and I mean really deep. Which will

suck in its other northern partners. A recession in Europe would drag the world

down – including a debt-driven China.

You

want soap opera? What happens when the currencies of the world start falling

significantly against the dollar? Currency manipulation or the real world? What

does a Trump Treasury Department do in response? Labeling everybody as currency

manipulators won’t work very well. Punitive tariffs are counterproductive. Do

we actually respond by monetizing the federal debt (at least the debt held in

the US) in order to reduce the value of the dollar and keep from completely

devastating the potential positive aspects of a new corporate income tax

policy? That would not be an irrational response, as it would essentially be what

the rest of the developed world was doing.

Dear

gods, we are moving into a world where we have absolutely no idea how things

are going to unfold. The uncertainty gage is pegging into the far-right red

zone.

There

are so many moving parts to the puzzle that it is hard to keep track of them. I

am going to get on a plane tomorrow to go meet in NYC with some of the

“insider” economists and thought leaders of the upcoming administration. And

I’m going to pose those very questions to them. For the most part, they are

friends or at least acquaintances. And in their private moments, they show me

that they “get it.” I will readily admit to being the Debbie Downer in the

group.

“The

problems of victory are more agreeable than the problems the defeat. But they

are no less difficult.”

New York (again), Florida, DC, and the

Caymans

As

noted above, I’m on my way to New York City on Monday and then hope to be back

home for the holidays. There will be no letter on Christmas weekend. I’m still

thinking about what to do over the New Year’s weekend, but my annual forecast

letter will come out the following week.

After

that, I’ll be at the Inside

ETFs Conference in Hollywood, Florida, January 22–25. If you are in

the industry and coming to that conference, make a point to meet with me. I

will be making some big announcements at the conference. Then I'll be at

the Orlando

Money Show February 8–11 at the Omni in Orlando. Registration is free.

There is also the high probability that I will be in Washington DC during the

inauguration as one of the corporate boards I am on is probably going to shift

their meeting to coincide with the inauguration. And I am

tentatively scheduled for a conference in the Cayman Islands.

Let me

wish you a sincere Merry Christmas and/or Happy Holidays. Most of the Mauldin

clan will be gathering for Christmas, and I am looking forward to it. Some of

them are dragging me, albeit not totally unwillingly, to Rogue One tonight. While I

have seen all the Star Wars movies, they are starting to become redundant,

derivative science fiction storytelling that doesn’t acknowledge the real

possibilities of a resplendent technological future. I was actually going to

skip this one, but I am being pulled along by some of the younger members of

the clan. I can’t gripe, because at least it’s not a chick flick.

For

me, the time between Christmas and New Year’s is when I think about the future,

and for the last 50+ years it is always the most optimistic week of my life.

Debbie Downer leaves the room and Pollyanna John emerges. The sun will come out

tomorrow, etc. That attitude is not always reflected in my annual forecasts,

but more often than not they have been pretty positive. But then again, I am

often wrong but seldom in doubt, so you need to bear that in mind. In any case,

I (probably foolishly) persevere in the annual predictive ritual.

Your

trying to make sense out of this puzzle analyst,

John Mauldin

0 comments:

Publicar un comentario