The

Fed Prepares to Dive

By John Mauldin

“No

one will lend at a negative interest rate; potential creditors will simply

choose to hold cash, which pays zero nominal interest.”

–

Ben Bernanke, 2009

“I

think negative rates are something the Fed will and probably should consider if

the situation arises.”

–

Ben Bernanke, December 2015

“In

theory there is no difference between theory and practice. In practice there

is.”

–

Yogi Berra

Economists

used to think below-zero interest rates were impossible. Necessity (as central

banks see it) is the mother of invention, though; and multiple central banks

now think negative rates are a necessary step to restore growth.

Are

they right? Will negative rates pull the global economy out of its funk?

Probably not; but for better or worse, several central banks are already below

zero. The Federal Reserve just sent its clearest signal yet that it is headed

that way, too. The Fed has warned banks to get ready. We had all better do the same.

This

week’s letter has two parts. The first deals with some of the practical aspects

of negative rates and what the Fed is really signaling. The second part, which

is somewhat philosophical, deals with why

the Fed will institute negative rates during the next recession. This letter is

longer than usual, but I think it’s important to understand why we will see

negative rates in the world’s reserve currency (and the currency in which most

global trade is conducted). This policy trend is truly a foray into unexplored

territory.

The idea of negative rates isn’t

new; what’s new is the willingness to try them out. The Ben Bernanke quote

above comes from a November 2, 2009, Foreign Policy article

in which the Fed chairman wrestled with how to keep inflation at the “right”

level in a weak economy.

Set

aside the question of whether there is any “right” level of inflation. As of

six years ago, the head of the world’s most important central bank thought no

one would ever lend at a negative interest rate. We now know he was wrong, at

least with regard to Japan and most of Europe. Central banks there have

instituted negative rate policies, and people are still borrowing and lending.

The

Fed staff has also speculated on the possibility. Earlier this month my good

friend David Kotok sent around links to several academic and central bank

negative-rate studies. One was a 2012 article by Kenneth Garbade and Jamie

McAndrews of the Federal Reserve Bank of New York. Their title tells you what

they thought at the time: “If

Interest Rates Go Negative… Or, Be Careful What You Wish For.”

Their

point was less about the theoretical wisdom of NIRP and more about the actual

potential consequences. They believed we would see a variety of odd responses

to a very odd policy situation. All kinds of incentives would reverse, for

starters.

Under

negative deposit rates, buyers would want to pay their invoices as soon as

possible, while sellers would want to delay receiving cash as long as possible.

Think about your credit card bill. If you normally spend $10,000 a month, your

best move would be to send the bank that much money before you spend it, then draw down the

resulting credit balance. The bank would no doubt try to discourage this

practice.

Could they? We don’t know.

Garbade

and McAndrews throw out another interesting idea: special-purpose banks:

If

rates go negative, we should expect to see financial innovations that emulate

cash in more convenient forms. One obvious candidate is a special-purpose bank

that offers conventional checking accounts (for a fee) and pledges to hold no

asset other than cash (which it immobilizes in a very large vault). Checks

written on accounts in a special-purpose bank would be tantamount to negotiable

warehouse receipts on the bank’s cash. Special-purpose banks would probably not

be viable for small accounts or if interest rates are only slightly below zero,

say -25 or -50 basis points (because break-even account fees are likely to be

larger), but might start to become attractive if rates go much lower than that.

Ludwig

von Mises fans will recognize that this approach is not far from the Austrian

economics goal of 100% reserve banking. It isn’t quite there because the vault

contains fiat currency instead of gold, but I think Mises would recognize it as

a step in the right direction. (The fact that Fed economists see it only as an

exotic theoretical possibility wouldn’t surprise him, either.)

The

consequences of such banking would be more than theoretical. If enough people

wanted to use these special-purpose banks, demand for physical cash would go

through the roof. There simply wouldn’t be enough to go around if it just sat

in vaults instead of circulating. Furthermore, if the vaulted cash in these

banks reduced deposits in normal loan-making banks, the whole banking system

might grind to a halt.

That

being the case, I suspect the Fed would prohibit banks from operating this way

– but they can’t stop people from hoarding cash under their mattresses. The one

thing they could

do is eliminate physical cash. Denmark, Sweden, and Norway are already

considering ways to do so.

Even

more ominously, Bloomberg reported on. Feb. 9 that a move is afoot for the

European Central Bank to get

rid of 500-euro notes, the Eurozone’s largest-denomination bills. They

portray this move mainly as a crime-fighting measure, but it would clearly make

cash hoarding much more difficult.

And if

Larry Summers and a few other well-known economists like Ken Rogoff have their

way, we will see the demise of the $100 bill in the US. You thought you were

just carrying those Ben Franklins around for convenience, not realizing that

they make you a potential drug dealer in some people’s eyes.

And of

course, hoarding cash would undermine the Fed’s goal of fighting deflation.

Holding cash is by definition deflationary.

All of

the above is just speculation at the moment. We don’t know how deeply negative

rates would have to go before people change their behavior. So far the negative

rates in Europe and Japan apply mainly to interbank transactions, not to

individual depositors or borrowers. Unless of course you are buying government

bonds.

That

said, we’ve seen a clear tendency on the part of central banks since 2008: if a

crazy policy doesn’t produce the desired results, make it even crazier. I

believe Yellen, Draghi, Kuroda, and all the others will push rates deep below

zero if they see no better alternatives. And my best guess is they won’t.

Turns

out negative rates aren’t exactly new. My good friend David Zervos, chief

market strategist for Jefferies & Co., sent out a note this week pointing

out that many “real,” inflation-adjusted rates have actually been negative for

years. Such rates have thus far not produced the kind of reflation that central

banks want to see. David thinks the ECB and BOJ should push nominal rates down

to -1%, launch new quantitative easing bond purchases of at least $200 billion

per month, and commit to do even more if their economies don’t respond.

Is

Zervos losing his mind? No, he actually makes a pretty good case for such a

policy – if you buy into his economic theories, which I discuss in the second

part of this letter. (Over My

Shoulder subscribers can read Zervos’s note here.)

It is painfully clear to most of us that what the central banks have done thus

far has not worked. I have a hard time imagining that a major NIRP campaign

will help, but I’ve been wrong before.

Former

Minneapolis Fed President Narayana Kocherlakota, who was for years the FOMC

uber-dove, says going negative would be “daring but appropriate.” He has a

number of reasons for this stance. In a

note last week, he said the federal government is missing a chance to

borrow gobs of money at super-attractive interest rates.

Kocherlakota

would like to see the Treasury issue as much paper as it takes to drive real

rates back above zero. He would use the borrowed money to repair our rickety

infrastructure and to stimulate the economy.

It is

an appealing idea – in theory. In reality, I have no faith that our political

class would spend the cash wisely. More likely, Washington politicians would

collude to distribute the money to their cronies, who would build useless

highways and bridges to nowhere. The taxpayers would end up stuck with more

debt, and our infrastructure would be little better than it is now.

The

fact that this is a “monumentally” bad idea doesn’t mean it will never happen.

There’s an excellent chance it will

happen. Yellen and the Fed are clearly looking in that direction.

Yellen

might face one small problem on the road to NIRP: no one is completely sure if

the Fed has legal authority to enact such a policy. An Aug.

5, 2010, staff memo says that the law authorizing the Fed to pay interest on excess

reserves may not give it authority to charge

interest.

This

potential snag is interesting for a couple of reasons. With last month’s

release of this memo, we now know the Fed was actively considering NIRP less

than a year after Bernanke himself said publicly that “no one will lend at a

negative interest rate.” Meanwhile, some at the Fed were clearly examining the

possibility.

What

else was happening at the time? The bond-buying program we now call QE1 had

just wrapped up in June 2010. The Fed launched QE2 in November 2010. This memo

came about because the Fed realized it needed to do more and was considering

options. QE2 apparently beat out NIRP as the crazy policy du jour.

The

question of the legality of negative rates came up again in congressional

testimony a couple of weeks ago. Rep. Patrick McHenry (R-NC) directly asked

Yellen if the Fed had authority to impose negative interest rates. According to

press

reports, she skirted a definitive answer:

In

the spirit of prudent planning we always try to look at what options we would

have available to us either if we needed to tighten policy more rapidly than we

expect or the opposite. So we would take a look at [negative rates]. The legal

issues I'm not prepared to tell you have been thoroughly examined at this

point. I am not aware of anything that would prevent [the Fed from taking

interest rates into negative territory]. But I am saying we have not fully

investigated the legal issues.

We

know the Fed was

investigating the legal issues as long ago as 2010. I would be shocked to learn

that they did not investigate those issues thoroughly in the six subsequent

years. Various Fed officials – including Yellen – have openly speculated about

NIRP. The Fed’s legal team should be disbarred for malpractice if it hasn’t fully investigated

yet. I think Yellen’s testimony was a way to deflect the potential controversy

as long as possible. I believe the Yellen Fed will telegraph the markets about

negative rates prior to implementing them, but evidently Yellen feels it is too

soon to send that signal now.

Of

course, Yellen also says she is “not aware of anything that would prevent” a

NIRP move. So she may do it and then blame her lawyers if someone cries foul.

By then the policy would be in place and probably irreversible. In Washington,

forgiveness comes easier than permission does.

In the

same testimony, Yellen hinted that the previously forecast March rate hike is

probably off the table now. We will get new “dot plot” forecasts, though. It

will be interesting to see how dovish they are.

As

I’ve said, I am firmly convinced that the Fed will not raise the federal funds

rate even to 1% this year. December may well have been the last hike we will

see for some time. I can see the Fed holding steady for several months. And

they are clearly getting ready to introduce negative rates during the next

recession. They are already telling banks to get ready for them, too.

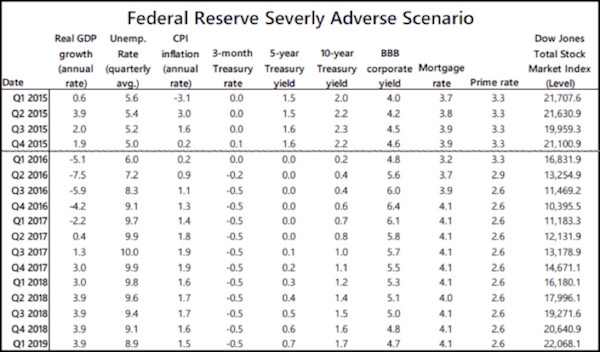

The

Dodd-Frank Act requires the Fed to conduct yearly “stress tests” on major

banks. They do this by giving the banks a set of hypothetical economic

scenarios. They released this

year’s scenarios on Jan. 28.

The

“severely adverse” scenario instructs banks to test their systems for a deep

recession, a 10-year Treasury yield as low as 0.2%, 5-year notes yielding 0%,

and a -0.5% 3-month T-bill yield from Q2 2016 through 2019.

Is

this “severely adverse?” It’s far less adverse than what Japan has already

experienced. BOJ purchases have driven Japanese government bond yields negative

10 years out the curve. Rates are also negative far out the yield curve all

over Europe, even in countries that don’t deserve such rates, let alone midterm

rates with even a one or a two handle.

The

stress test scenarios aren’t a forecast, per se, but they mean the Fed at least

sees those conditions as possible. The whole exercise is pointless if the

scenarios could never happen. I think this stress test scenario is the clearest

sign yet that the Fed views NIRP as a legitimate alternative.

It

doesn’t mean NIRP is guaranteed. I believe Yellen when she says their policy is

“data-dependent.” They are no more prescient about the future than the rest of

us are. All they can do is look at the data and try to respond appropriately. I

don’t envy them that job.

I

think the Fed is right now in a position much like the one that was portrayed

in that 2010 staff memo. They see their last big move as not having had the

desired effect and are considering a new set of options. NIRP is on their list.

Having

decided to put NIRP on the list, the Fed has to make sure the banking system

can handle it. Whether it can is far from clear right now. The technology

issues alone could unleash chaos if the Fed went negative without warning. I

think putting negative rates in the stress test scenarios is the Fed’s

not-so-subtle message to Wall Street: “Get ready; this could really happen.”

If

Europe’s experience means anything, it seems likely our banks aren’t ready yet. Consider

this Mar.

4, 2015, Wall Street Journal

story.

Widespread

negative interest rates, once only a theoretical possibility, have become a

real-life problem for Europe’s financial system.

From

Sweden to Spain, banks, brokers and other financial firms are grappling with

technical and legal glitches thrown up by negative rates, forcing them to

redesign computer systems, tear up spreadsheets and redraft legal contracts.

The

issue echoes the scrambles around the Year 2000 computer bug and the launch of

the euro, when some bank systems couldn’t handle the introduction of a new

currency, said Kevin Burrowes, head of U.K. financial services at

PricewaterhouseCoopers. A handful of malfunctioning computer programs can cause

“huge problems,” while working around problems manually makes more controls

necessary and increases the risk that something could go wrong, Mr. Burrowes

said.

Preparing

for NIRP is a far smaller challenge than preparing for Y2K, which required

years of reprogramming and hundreds of billions of dollars, but it is still a

huge project. Some reports say European banks are still dealing with the

programming issues. And technology is only part of the problem. Think of all

the contracts and other legal documents that might need rewriting and

renegotiation. If nothing else, the Fed just stimulated the securities and

contract law businesses.

One

small example from my personal experience: I have been involved in the

management of several large commodity funds over the past 25 years. Back in the

day, commodity funds had a significant advantage in that they could put 90% of

their money into short-term government bonds to generate the capital for their

futures contracts. This interest offset a lot of their fees in the ’80s and

’90s. Not so much today. I suspect that many of the organizational documents

required still state that such funds will use short-term Treasuries as their

cash base.

Requiring

these funds to lose ½% would mean they start in the hole. Not what a fund

manager wants to do. But it has to be short-term cash, as the money has to be

available on very short notice since it’s the collateral for a futures

contract. I’ve sat and thought about this and still haven’t come up with a way

around this. I wonder how many other funds will have the same issue. (We will

discuss this subject in further depth in a few paragraphs.)

The

Fed is specifically warning banks, but NIRP will affect the whole economy. If

you own any kind of business or you are an active investor, I expect that NIRP

will create significant headaches for you. Are you ready?

Most

of us have no idea whether we’re ready, but we might be able to find out.

Here’s a simple test. Go to whatever accounting software or spreadsheet program

you use, find the interest rate setting and see if it will let you enter a

negative number.

If it

won’t accept a negative rate at all, now might be an excellent time to update

your software.

If the

program does let you show a negative rate, dig a little and see how that rate

affects the rest of your bookkeeping. Most of us have created numerous Excel

spreadsheets. You know that if you get your programming off a little bit, you

end up with ##### signs in some of the cells. When you enter negative

interest rates into your software, you may find similarly weird things

happening. They could be good-weird or bad-weird, but in either case you might

want to consult your brokerage firms, investment advisors, accountants, and tax

advisors about possible consequences.

While

you’re at it, think about how the rest of the Fed’s “severely adverse” scenario

might affect you. Here is the guidance the Fed gave the Banks:

(Yes,

I know they spelled severely

wrong. Clearly the Fed needs a new proofreader along with new policies. That

said, you just can’t catch all the mistakes. There are at least three

professional editors who read my letter prior to publication, and misteaks

still happen.)

I

didn’t even mention the Fed’s stock market scenario in the right column above.

It shows the Dow dropping almost to 10,000 by the end of this year and

recovering very slowly. In a world where anything is possible, I suppose it is

prudent to ask what if

questions. I do not see the Dow’s dropping 10,000 points this year, but in a

deep recession? That plunge would not be out of the realm of historical

precedent. If banks are planning for adverse scenarios, it would be a good idea

for you to do so, too, even if you think there is no chance in hell those

scenarios will play out. Contingency planning is simply prudent management.

Don’t let a recession catch you without a plan.

The

problems posed by negative rates are mostly practical in nature, but they come

with some deeply disturbing side effects. In the discussion above I didn’t

venture into the theoretical problems of misallocation of capital, the negating

of Schumpeter’s creative destruction cycle, the even more intense repression of

savers and retirees, and the absolute devastation negative rates would wreak up

on pension, endowment, and insurance company portfolios.

In a

world of ultralow rates, pension funds that are targeting 7½% growth in order

to meet their funding needs 20 years out will find those targets are impossible

to attain (as they are today, only moreso). It is not yet obvious to the

general public how deeply underfunded pensions are, because pension funds are

still assuming that future returns will be in the 7½-8% range. That pension or

annuity you are counting on for your retirement is most likely in serious

trouble. And as people get older and have no practical way to go back to work,

pension funds that are forced to reduce payments in 10 or 15 years (and some

even sooner) will destroy the lifestyles of many of our elderly. You think

there is a violent backlash among voters today? Just screw around with

pensions…

So

what would make central bankers around the world agree that negative rates are

a solution to our current economic malaise? And that, with all their known negative consequences,

not to mention their unknown

unintended consequences, negative rates are better than the

alternative?

I have

been trying to devise an explanation of the negative rates proposition that

most people can grasp by likening prevailing economic theories to a religion.

Everyone understands that there is an element of faith in their own religious

views, and I am going to suggest that a similar act of faith is required if one

is believe in academic economics. Economics and religion are actually quite

similar. They are belief systems that try to optimize outcomes. For the

religious that outcome is getting to heaven, and for economists it is achieving

robust economic growth – heaven on earth.

I

fully recognize that I’m treading on delicate ground here, with the potential

to offend pretty much everyone. My intention is to not to belittle either

religion or economics, but to help you understand why central bankers take the

actions they do.

This

explanation will need a little set-up. I have noted before, in an effort to be

humorous, that when you become a central banker you are taken into a back room

and given gene therapy that makes you always and everywhere opposed to

deflation. Actually, this visceral aversion is imparted during academic

training in the generally elite schools from which central bankers are chosen.

This

is our heritage; it’s learning derived not only from the Great Depression but

from all of the other deflationary crashes in our history, too, not just in the

US but globally. When you are sitting on the board of a central bank, your one

overriding rule is never to allow deflation to occur on your watch. No one

wants to be thought responsible for bringing about another Great Depression.

And

let’s be clear, without the radical actions taken in 2008–09 to bail out the

banks, drop rates to the zero bound, and institute quantitative easing, we

would likely have been facing something similar to the Great Depression. While

I don’t like the manner in which we chose to bail out the banks, some form of

bailout was a necessary evil.

Think

deflationary depressions can’t happen today? Clearly, they can. Greece, for all

intents and purposes, has sunk into a massive deflationary depression. That

reality is not necessarily reflected in the prices of their goods, which are

denominated in euros. No, the deflationary depression in Greece is in their

labor market.

Normally,

when a sovereign country gets into financial trouble (generally because of too

much debt), it will devalue its currency so that the prices of products it

imports go up and labor costs and the prices of products it sells abroad go

down. But since Greece could not devalue its currency (the euro), it was

essentially forced to allow its labor costs to fall drastically. Since it is

basically impossible to go to everyone in Greece and say, “You need to take a

25% cut in your pay, even though the prices of everything you’ll be buying will

still be in euros,” the real world simply produced massive Greek unemployment –

precisely what you would expect in a deflationary depression. Greece will

likely continue to suffer for a very long time, whereas if the Greeks had left

the euro, defaulted on their debts, and devalued their currency, they would

likely be enjoying a quite robust recovery.

Greece’s

present is a possible near future for other countries in Europe (Portugal is

likely to be next, and Italy will surprise everyone with its severe banking

problems), which is why the European Central Bank is so desperately fighting

the deflationary impulse embedded in the very structure of the European Union.

Now,

the United States is clearly not Greece. However, we are subject to the same

laws of economics.

By

definition, recessions are deflationary. Whenever we enter the next recession,

we are going to do so with interest rates close to the zero bound. Most of the

academic research both inside and outside the Fed suggests that quantitative

easing, at least in the way the Fed did it the last time, is not all that

effective. If you are sitting on the Federal Reserve Board, you do not want to

allow deflation to happen on your watch. So what to do? You try to stimulate

the economy. And the one tool you have at hand is the interest-rate lever.

Since rates are already effectively at zero, the only thing left is to dip into

negative-rate territory. Because, for you, allowing a deflationary malaise to

set in is a far worse thing than all of the potential negative consequences of

negative rates put together. It’s a Hobson’s choice; you see no other option.

Let’s

do a little sidebar here. There’s lots of discussion in the media of the

possible moves the Federal Reserve could make. Some people talk about the Fed’s

buying the government’s infrastructure bonds, or buying equities or corporate bonds,

or even doing the infamous “helicopter drop” of money into outstretched

consumer hands. Those are not legal options for the Fed. The Fed is actually

fairly restricted in what it can purchase. All of these outside-the-box

transactions would require congressional approval and amendment of the Federal

Reserve Act.

I can

tell you that there is almost no stomach in the leadership of Congress or at

the Fed to bring up the Federal Reserve Act for congressional action. Everyone

is worried about potential mischief and political sideshows. Quite frankly, if

the Federal Reserve decides that it wants to do more quantitative easing, I

would much prefer that Congress authorize the Fed to purchase a few trillion

dollars of 1% self-liquidating infrastructure bonds – or, as a last resort, to

do an actual helicopter drop. The infrastructure bonds would create jobs and

give our children something for their future, a much healthier outcome than the

ephemeral boosting of stock and bond prices yielded by the last rounds of quantitative

easing. In those instances, the benefits of QE went primarily to the well-off.

But I digress.

The

reigning academic orthodoxy for central bank believers is Keynesianism. Saint

Keynes postulated that consumption is the fundamental driver of the economy. If

the country is mired in recession or depression, then government and monetary

policy should be geared toward increasing consumption in order to spur a

recovery. Keynes argued that the government should be the consumer of last

resort, running deficits as deep as necessary during recessions. (He also

advocated paying down the debt during the good times, prudent advice roundly

ignored.)

The

current belief in vogue is that another way to increase consumption is to get

businesses and consumers to borrow money and spend it. Hopefully, businesses

will invest it and create new jobs, which will in turn enable more consumption.

One way to stimulate more borrowing is to lower the cost of borrowing, which

the Federal Reserve does by lowering interest rates. The opposite is also true:

if inflation is a problem, the Fed raises rates, taking some of the

inflationary steam out of the economy.

How

would negative rates work? The Federal Reserve would charge a negative interest

rate on the excess reserves that banks deposit at the Fed. Note this is not a

negative interest rate on all deposits, just on “excess reserves” on deposit at

the Fed. An excess reserve is a regulatory and political concept that is a

necessary feature of the fractional reserve banking systems of the modern

world. Banks are required to maintain a reserve of their assets against

possible future losses from their loan portfolios. The riskier the assets the

banks hold, the less those assets count towards the required level of reserves.

Reserves are required to keep a bank solvent. Banks are closed and sold off

when their reserves and capital are depleted below the allowed levels.

Any

reserves in excess of the regulatory requirements are counted as “excess.” The

theory is that if the central bank charges banks interest on their excess

reserves, the banks will be more likely to lend that money out, even if at a

lower rate, in order to at least make something on those reserves. Right now,

banks are paid by the central bank for their excess reserves on deposit. Given

the level of excess reserves at the Fed, these interest payments amount to

multiple billions of dollars that are fed into the banking system each quarter;

and that is one of the reasons why US banks have been able to get healthier in

the wake of the Great Recession.

Consumers

and businesses would borrow this cheaper money from the banks and presumably

spend it or otherwise put it to use, thereby stimulating the economy and

vanquishing the evil of deflation. In theory, as the economy recovers, interest

rates are allowed to rise back above the zero bound.

Of

course that was the theory when we went to zero rates some six years ago. At

some point the economy would recover and the Fed would normalize rates. Except

the economy never got to a place where the Fed felt comfortable raising rates

even minimally – until last December. And now the high priests of the FOMC are

signaling that it might be longer than they originally thought before they

swing their incense orbs and raise rates again.

There

are some (including me) who would argue that, rather than focusing on

consumption, monetary and fiscal policy should focus on increasing production

and income. By lowering (repressing) the amount of income savers get on their

money, you push savers into riskier assets. That is generally not what you tell people to

do with their retirement portfolios, (nor can we overlook the fact that the

country is getting older). Thus if interest rates are artificially low because

of Fed policy, that reduces the amount of money retirees have to spend. The

Federal Reserve and central banks in general seems to think it’s better to have

consumers borrow than save.

It’s a

Keynesian conundrum. If nobody spends and everybody saves, the economy slows

down. While it may be a good thing for you individually to save and prepare for

your retirement, if everybody does so at the same time the economy plunges into

recession.

Now

let’s get back to the intersection of economics and religion. There are

multiple competing economic theories on the government’s role in monetary

policy making. The operative word is theories.

Each is an attempt to describe how to manage a vastly complex modern economy.

Some see too much debt as the cause of our current malaise. Others think that

lowering taxes would allow consumers and businesses to keep more of their

income and hopefully spend it.

In the

not too distant human past, shamans and soothsayers conjured theories about how

the world worked and how to predict the future. Some examined the entrails of

sheep, while others read meaning into the positions of the stars (or whatever

their prevailing theory dictated) and told leaders what policies they should

pursue. An astute priest would pretty quickly figure out that the best route to

priestly job security was to foretell success for the

politician’s/king’s/tribal chief’s pet policy course.

In

today’s world, economists serve exactly the same function. They skry their data

sets – a latter-day version of throwing the bones – and then, based on the

theory by which they believe the data should be interpreted, they confirm the

orthodox policy choices of their political masters – and so their careers

prosper.

This

is not to disparage economists – not at all. They really do try to come up with

the best possible policies – but the range of policy alternatives is

constrained by the economists’ (and the general society’s) belief system. If

you believe in a Keynesian world, then you will prescribe lower rates and more

fiscal stimulus during times of recession.

If, however,

you believe in a competing model, such as the Austrian theory postulated by

Ludwig von Mises, then you believe that smaller government, far less fractional

reserve banking (if any at all), and a gold standard are appropriate. A

recession should be allowed to “clear,” permitting defaulting borrowers to

reduce their debts and putting the assets that collateralized their loans back

on the market at reduced prices, thereby encouraging businesses to employ those

now-cheaper assets in income-producing activities. (This is a very simplified

explanation.)

There

are other competing theories, each with its own model of how the world works.

There is convincing logic and a believable rationale behind each theory. If we

had adopted an Austrian model in 2008–09, we would have had a much deeper

recession and unemployment would have risen higher, but the recovery would

theoretically have come more quickly as prices cleared and debt was resolved.

However, that period of time before the recovery began would have been devastating

to the millions of families who would have faced even more crippling

unemployment than we saw. That is an experiment we did not conduct, so we will

never truly know whether that path might have been less painful in the long

run.

Austrians

are willing to face a series of small recessions as part of the price of

maintaining a free economy, rather than postponing recession and trying to

fine-tune what is supposedly a free market economy by means of monetary and

fiscal policy. An analogy would be the theory that allowing small and

controllable forest fires today might prevent a large, utterly devastating

forest fire in the future. Nassim Taleb’s important book Antifragile

makes a strong case that businesses, markets, and whole societies are much

better off if they allow relatively minor random events, errors, and volatility

to correct as quickly as possible rather than continually patching them over to

avoid short-term pain. Decentralized experimentation in the economy by numerous

complex actors capable of taking risks works better than a directed economy

that encourages the buildup of excessive risk throughout the entire economy.

The

problem is, there really is no one clearly right answer as to which economics

belief system is best. I know what I believe to be the correct answer, but that

belief is based on the way I understand the world – and the world is vastly

more complex than anyone’s theory can be. No theory allows for a perfect

solution for all participants. Rather, each theory picks winners and losers,

with the overall objective of creating an economy that has maximal potential to

grow and prosper.

(Sidebar:

Let me tell you where Bernie Sanders and I agree. He rails against the

privileges of Wall Street, crony capitalists, corporate insiders, and

lobbyists, and the political favors and laws they get passed that benefit them

and not Main Street. The deck is stacked in their favor. In that he is right.

But his and my solutions to the problem are not similar, as he wants to create

even more regulation and taxation, and I would prefer to remove all of the tax

preferences and greatly reduce the regulatory morass that favors large

businesses over small. I don’t want the government involved in picking winners

and losers; that’s the role of the marketplace.)

So

this is what it comes down to: The reigning academic theory/belief system is

Keynesianism. The head Keynesians are signaling that they are going to give us

negative rates. In fact, according to their theory, it would be irresponsible not

to do so. They believe that if they sit back and allow the economy to sort

itself out, the outcome would be far worse than anything that could be wrought

by the intended and unintended consequences of negative interest rates.

We can

differ with those in charge, but the experiment with negative rates is going to

happen, and we need to begin to adjust – to think through how to position our

portfolios and our investment strategies, our businesses, and our lives.

The

Fed is run by True Believers. Just as Christianity or Islam or any other

religion has believers that range across a spectrum of faith and beliefs, so

does Keynesianism. At the Fed, these are deeply held beliefs: our central

bankers are well convinced that the facts demonstrate the validity of their

belief system.

I am

reminded of the apologetics courses that I took in seminary (yes I graduated

from seminary in 1974 – go figure). Apologetics courses basically teach you

reasoned arguments in justification of a particular view, typically a theory or

religious doctrine. We would look for logic and evidence that our particular

version of Christianity was the correct and true position. Apologetics gave us

the techniques and facts that would back us up!

I am

not really trying to equate religion and economics, but I am saying that both

rely on belief systems about how the world works, and that the behavior of

believers is modeled on those systems. Paul Krugman tells us that fiscal

stimulus and quantitative easing didn’t give us enough of a recovery simply because

we didn’t do enough. If we had just believed more, had more faith in the

effectiveness of Keynesian doctrine, we would now be well on our way to the

economic promised land!

The

fact that neither Europe nor Japan nor the United States have seen a recovery –

that much of Europe is either in recession or on the borderline of recession,

that Japan is dealing with severe deflationary pressures, and that the US is

visibly slowing down does not create a question in Keynesian minds with respect

to the correctness and effectiveness of their policies. I believe that both

Japan and Europe are going to double down on quantitative easing and negative

rates in their respective countries, and the US will soon follow.

I am

glad I am not a central banker. The pressure to “do something” in the midst of

a crisis must be horrific. To feel a responsibility and not be able to respond

would be emotionally draining. I do not envy any of them. I think my own

current belief system would probably take us in the optimal direction over the

long term, but I can assure you that in the short term quite a few of my fellow

citizens would not be happy with the process. And whether it is I or the

Keynesians selling a particular theory, promising people pie in the sky doesn’t

help them much to deal with the problems they face here and now.

The

fact is that all of these economic theories have at their core political views

about how the economy should be organized and managed. Including mine. That

doesn’t necessarily mean mine is right and theirs is wrong. To determine the

“rightness” of a theory, you generally try to conduct controlled experiments

that give reproducible results. That kind of gold-standard research is simply

not possible in today’s world. So we actually are forced to rely upon our pet

theories as to how the world works. I am certainly not a believer in moral

equivalency, but until one operative theory is thoroughly discredited (as

communism was) it can remain the controlling theory for a long time.

I have

a lot more to say and will do so in the future, but this letter is getting

overly long, and I need to close it. I leave you with one of my favorite Yogi

Berra quotes: “In theory there is no difference between practice and theory. In

practice there is.” In theory the economy should respond to stimulus, and an

economy that is demonstrably overburdened with debt should be pushed to

increase that debt. In practice, the outcome may not be quite as salutary as

the theory suggests. Adjust your world accordingly.

Your

meditating on belief systems analyst,

John Mauldin

0 comments:

Publicar un comentario