With companies having gorged on cheap money, a reckoning may be coming

Andrew Edgecliffe-Johnson in New York and Peggy Hollinger, Joe Rennison and Robert Smith in London

Since 1925, the Grand Ole Opry has featured the music of countless country and bluegrass stars, from Bill Monroe to Dolly Parton.

As Ryman Hospitality Properties built a hospitality and entertainment empire around the original Nashville radio show, the parent company’s debt grew to over $2.5bn, but its chairman insisted that its balance sheet was “really strong”.

That held through last week, when Ryman’s buildings escaped the tornado that hit Nashville, but another storm has since ripped through corporate debt markets. As coronavirus fears have consumed investors, warnings over the potential of a rising debt load to push companies towards collapse are beginning to be tested.

After Ryman’s hotel customers cancelled 77,000 room nights last week, at a potential $40m cost to revenues, Standard & Poor’s placed its credit rating on watch for a potential downgrade.

The rating agency’s response shows how a public health crisis is prompting a sudden reassessment of corporate credit risk, raising doubts about borrowers that had long been seen as stable. That is changing how markets view sectors from cruise lines to retailers, forcing companies as large as Boeing and United Airlines to review their borrowings, and posing the risk of financial institutions being saddled with problem loans.

As Colin Reed, Ryman’s chairman, said last week: “We’ve had lots of experience in this type of thing, but this is a little weird.”

-------------------------

Companies have gorged on cheap debt for a decade, sending the global outstanding stock of non-financial corporate bonds to an all-time high of $13.5tn by the end of last year, according to the OECD, or double where it stood in December 2008 in real terms.

Borrowing costs had tumbled after central banks lowered interest rates to jolt their economies following the 2008 financial crisis. Investors, starved of yield from safer government bonds, saw lending to riskier companies as a way to juice returns.

“There’s a large universe of middle market companies that on the back of an 11-12 year credit cycle have continually been able to borrow and reborrow from one lender to another,” observes Mohsin Meghji of M-III Partners, a turnround veteran who has restructured companies from Sears to Sanchez Energy. “These companies have been limping along by virtue of rates having been very low. They haven’t really deleveraged.”

Ruchir Sharma, chief global strategist at Morgan Stanley Investment Management, estimates that one in six US companies does not earn enough cash flow to cover interest payments on its debt. Such “zombie” borrowers could keep putting off the crunch as long as debt markets kept letting them refinance. But now a reckoning is coming.

The consequences showed up most vividly this week in the oil and gas sector as a price war between Riyadh and Moscow compounded the market’s coronavirus concerns, plunging almost $110bn of US energy company bonds into distressed territory.

“The timing of this is a massive punch in the gut for US upstream oil and gas companies,” Mr Meghji warned.

But the risks extend far beyond oil and gas. As Paloma San Valentin, managing director for the Americas at Moody’s, put it this week, there is now a “growing risk to corporate credit quality around the world”.

-----------------------

The phones have started ringing at restructuring groups as directors and investors seek advice on how to navigate the uncertainty.

Rating agencies, still smarting from their reputation for moving slowly in the last crisis, are already sounding the alarm on companies that are most exposed to travel cancellations, disrupted supply chains and consumers’ deferred discretionary spending.

Moody’s has lowered its sales forecast for the auto industry and cut its outlook for the airline, lodging and cruise industries to negative. The US cinema operator National Amusements joined cruise ship companies such as Carnival and Royal Caribbean on S&P’s “watch negative” list.

Bonds from US car-rental company Hertz have been smashed, with yields on its longer-dated bonds hitting 10 per cent. Cinema chain AMC saw a £500m bond that was trading close to face value at the start of the year fall as low as 66 pence in the pound on Wednesday.

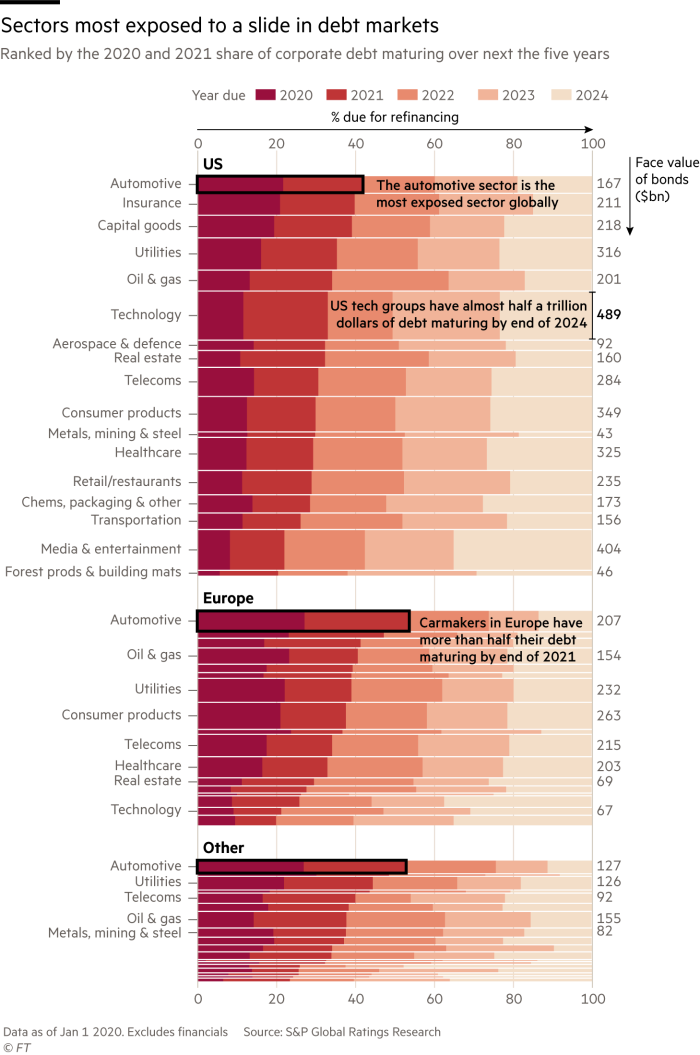

Meanwhile, carmakers, electronics groups and chemicals companies all remain vulnerable because of supply chain interruptions.

The market swings are also changing the calculus on mergers and acquisitions, posing a test to leveraged deals like the recent €17.2bn private equity deal to buy Thyssenkrupp’s lifts business.

And they have raised new doubts about companies with turbulent pasts that had been trying to earn back investor confidence. Bonds in WeWork, the lossmaking office company, have dropped from about 90 cents on the dollar to 68 cents.

The tally of defaults that preceded the market’s coronavirus shudder provides some pointers to where the exposure may be most acute. Eight of this year’s 20 large defaults have come from the consumer sector, S&P found, including US retailer Pier 1 Imports. A bankruptcy filing from McClatchy extended the sorry record of advertising-dependent local newspaper owners, and while there have been only two oil and gas defaults so far this year, the rating agency expects that number to rise.

At 282 companies in December, S&P’s “weakest links” list of low-rated junk bonds on which it has a negative outlook was at its longest since the crisis era of July 2009.

Such lists fail to capture how many smaller companies are at risk of falling into financial trouble. Julie Palmer, regional managing partner of Begbies Traynor, a UK restructuring group, estimated that 490,000 UK companies were already displaying signs of distress before the virus hit. “If coronavirus affects even 5 per cent, that would double the rate of corporate insolvencies,” she said.

Big banks were likely to focus on the largest corporate clients, putting smaller companies “well back in the queue”, said Campbell Harvey, finance professor at Duke University’s Fuqua business school. “These small and medium-sized firms are often crucial links in the supply chain. If these links are broken, it will be much more difficult to recover from a recession,” he warned.

-------------------

More than $320bn of US debt sitting on the lowest rung of the investment grade ladder now yields more than 5 per cent, according to Ice Data Services figures, previously a rate attached to much riskier companies.

The list includes household names, from General Motors and Ford to embattled retailers Nordstrom and Kohl’s. One name on the list, Occidental Petroleum, slashed its dividend this week to guard against further declines.

Restructuring experts said investors scanning for vulnerability should watch those companies with largely fixed capacity and high costs which would be hard hit by a significant drop in demand. Almost $840bn of bonds rated triple B or below in the US are set to come due this year and roughly $270bn of US bonds now trade below 90 cents on the dollar. Many companies have already been locked out of refinancing or selling new debt.

Ryman Hospitality Properties built a hospitality and entertainment empire around the former Grand Ole Opry. Hotel customer cancellations due to the coronavirus have left the company’s bonds at risk of a credit rating downgrade © (c) Giuliachristin | Dreamstime.com

Several companies, even in hard-hit sectors such as airlines and cruise lines, have managed to refinance. Often, though, lenders were imposing new demands such as interest rate floors or “material adverse clause” provisions, noted Jennifer Daly, a partner at King & Spalding, the law firm.

Others are in a worse plight. Intu, the UK shopping centre owner, now faces a painful debt restructuring after its planned £1.5bn rights issue collapsed last week.

The debt market is now pricing in material uncertainty around an upcoming €725m bond maturity for CMA CGM, even though the French shipping group has stressed that it has enough cash to repay the bond without raising new debt.

Veterans of past crises note that this one will also present opportunities, both for well-capitalised lenders with a long-term focus and for companies with stronger balance sheets.

“If you are running a business and have five-year horizons . . . [coronavirus] is not going to be the only thing that matters,” said Ian Stewart, chief economist of Deloitte. Governments may well step in to avoid strains on corporate balance sheets turning into a wider solvency crisis. He adds: “Policymakers are massively incentivised to act on this.”

As they navigate a suddenly changed lending market, companies are weighing both greed and fear.

“In the market at least, it’s hard to tell what’s spreading more quickly, the fear or the virus itself,” said King & Spalding’s Ms Daly. “My advice to clients universally has been ‘wash your hands, protect against the downside and then don’t waste a crisis’.”

That may fall short of a country and western lyric. But it is more comforting than the Grand Ole Opry refrain to which some corporate borrowers can now relate: “Too much month at the end of the money.”

0 comments:

Publicar un comentario