by: Hard Assets Investor

March 08, 2010

Julian Murdoch

Last Friday, gold closed up 1.5 percent for the week to end at $1135.20/oz, thanks to a U.S. dollar that couldn't decide if it was strengthening or weakening. Of course, whether the gains continue remains to be seen, but for gold bugs, it seems one thing is certain: Gold demand has never been higher.

Last Friday, gold closed up 1.5 percent for the week to end at $1135.20/oz, thanks to a U.S. dollar that couldn't decide if it was strengthening or weakening. Of course, whether the gains continue remains to be seen, but for gold bugs, it seems one thing is certain: Gold demand has never been higher.Or has it?

Last month, the World Gold Council released its annual supply and demand report on the yellow metal, and it revealed more than a few surprises.

2009: A Down Year For Demand

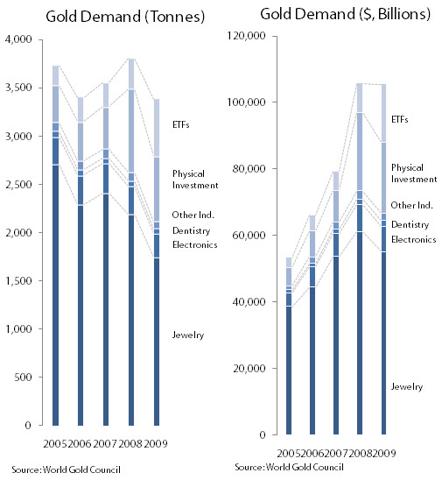

In reality, total gold demand actually fell in 2009, down 11 percent year-over-year. But due to the higher average price per ounce in 2009, the dollar value of gold demand remained roughly the same.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/3/8/saupload_gold_chart_2_thumb1.jpg)

{kind=link}

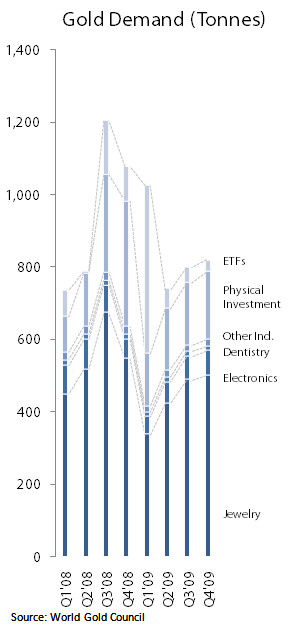

As we've previously discussed, demand for gold comes from lots of different places: ETFs, bars and coins, jewelry, dentistry, electronics and some minor industrial uses. And while some applications inherently drive demand more than others, it's interesting to see how demand has shifted from quarter to quarter.

ETF Demand: Not As Strong As Before

For starters, mom-and-pop investors in gold ETFs just aren't having that big an impact on gold's overall demand. In fact, so far in 2010, investment into gold ETFs has been sluggish: Bullion held by the SPDR Gold Trust (NYSE Arca: GLD) has fallen to 1,115.51 metric tons - down 1.6 percent for the year. That's a big change from the 45 percent inventory increase GLD saw last year.

But that 45 percent figure is misleading. Taken as a whole, 2009 was a great year for GLD and other gold ETFs, but quarter-to-quarter, the picture is less clear. As Lara Crigger discussed in last week's Riding The Gold Bubble, the majority of ETF demand hit in the first quarter, as lower gold prices and the hangover from 2008's market meltdown drove hordes of investors toward safe-haven investments. But it didn't last. ETF investment demand dropped precipitously over the next three quarters, and although it still rose 87 percent year-over-year in 2009, ETF demand long term is definitely on the wane:

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/3/8/saupload_gold_chart_1.jpg)

{kind=link}

Even those folks buying physical coins and bars backed off the gas pedal after the insane demand of the 2008/2009 fall and winter. As ETF investing dropped 67 percent from Q4 2008 to Q4 2009, so too did so-called bar hoarding fall 55 percent year-over-year. Even coin sales, which remain constrained by greater supply concerns, were down 8 percent year-over-year.

A (Slight) Recovery In Traditional Demand

Instead, we began to see some slight indications of recovery in jewelry demand. Although the rebound remained slow, some areas such as China showed year-on-year growth; the country saw a 6 percent increase in gold tonnage demand, which translates to a 19 percent increase by value.

But we shouldn't get carried away: Most markets didn't fare nearly as well, with gold jewelry demand in tonnes dropping 20 percent for the year and 10 percent in value.

In fact, electronics was the only sector that saw year-over-year gains in demand in Q4 2009. The World Gold Council cites the economic downturn as a good thing in this case, as it led to a decline in overall electronics inventories. That, in turn, resulted in a modest uptick in semiconductor sales for 2009, which raised immediate demand for gold 25 percent over Q4 2008.

Still, applications where gold remains optional, like dentistry, continued to suffer, given the high prices. Dentistry demand fell 5 percent year-over-year; other industrial applications were down 13 percent.

Cash For Gold's Effect On Supply

According to the World Gold Council, total gold supply was up 11 percent year-over-year in 2009, primarily due to a spike in recycled gold entering the market in the first quarter:

"Over the year as a whole, the supply of recycled gold exceeded historical norms," the World Gold Council said in its report. That is, the flood of cash-for-gold exchanges put 2009's supply near all-time highs, despite the fact that central banks once again were net buyers of gold.

"Over the year as a whole, the supply of recycled gold exceeded historical norms," the World Gold Council said in its report. That is, the flood of cash-for-gold exchanges put 2009's supply near all-time highs, despite the fact that central banks once again were net buyers of gold.Gold supply is expected to continue to rise this year, with major producing nations like Australia talking about 10-11 percent increases in production in 2010; ABARE recently estimated its production would jump around 10 percent.

The End Effect On Gold

So what about prices? That's where the balance comes in.

At this point, there's little question that ample gold supply exists to meet current demand, but most of the flexibility will come from scrap, which is hugely price sensitive. In its announcement, ABARE argued gold would average $1080/oz for 2010—before crashing down to $900 again on oversupply. That's a far cry from HSBC's suggestion that gold could go as high as $5,000/oz in five years.

Me? I tend to follow supply and demand, and right now, the market's coming off four straight quarters of oversupply. Given that, it's actually quite impressive the metal managed to rally $200 since last March. But I'm not inclined to think $5,000/oz—or even a more modest $1,500/oz—is anywhere in the cards until we see real demand start outstripping real supply.

0 comments:

Publicar un comentario