The dangers lurking in our messy and unpredictable world

Fragilities in the global economic system are real and must be confronted

Martin Wolf

© James Ferguson

© James FergusonLast week, I discussed five long-term drivers of the world economy — demography, climate change, technological advance, the global spread of knowhow and economic growth itself.

This week I will look at shocks, risks and fragilities.

Together, I suggest, all these shape the economy in which we live.

A “shock” is a realised risk.

Risks, in turn, are almost all conceivable.

In Donald Rumsfeld’s helpful phraseology they are “known unknowns”.

But their likelihood and severity are unknown.

We are surrounded by such risks — further pandemics, social instability, revolutions, wars (including civil wars), mega-terrorism, financial crises, collapses in economic growth, reversals in global economic integration, cyber-disruptions, extreme weather events, ecological collapses, huge earthquakes or eruptions by super-volcanoes.

All of these are imaginable.

The realisation of one raises the likelihood of at least some of the others.

Moreover, known fragilities increase the likelihood or at least the likely severity of such shocks.

As the Global Risks Report 2024 from the World Economic Forum demonstrates, we live in just such a high-risk world.

It is not so much that anything can happen.

It is rather that a sizeable number of quite conceivable somethings might happen, possibly at much the same time.

The recent past has shown this clearly: we have suffered a pandemic, albeit a relatively mild one by historical standards, two costly wars (in Ukraine and the Middle East), an unexpected surge in inflation and an associated “cost of living crisis”.

Moreover, these disturbances followed not long after the multiple financial crises of 2007-15.

Not surprisingly, these shocks have proved damaging and destabilising.

They are likely to impose long-term costs, especially on more vulnerable countries and people.

But we can see a piece of good fortune: the inflation shock looks likely to fade relatively soon.

Consensus forecasts for inflation in 2024 have changed very little since January 2023.

In January 2024, they were 2.2 per cent for the eurozone, 2.6 per cent for the US and 2.7 per cent for the UK.

Central bankers are mostly desperate to avoid the mistake of loosening too soon and so are far more likely to do so too late.

Consensus forecasts for growth in 2024 are consequently low, but not negative, so far.

The future of the current wars is far more uncertain.

They might be resolved, fade away or explode into something bigger and more damaging.

Such uncertainty, history tells us, is in the nature of war.

Moreover, how they end might — indeed, probably will — create further risks.

At one end, there might be peaceful settlements of both conflicts. At the other, there might be a mere pause before still worse hostilities.

What happens in the future depends not only on how the driving forces continue to operate, when (and how) recent shocks work themselves out, and which risks are realised.

It also depends on the fragilities in the system. Four stand out.

The first set is environmental.

We are engaged in an irreversible experiment with the biosphere, largely, but not exclusively, in relation to climate.

As the human economy grows, so is its impact on the biosphere likely to expand, too.

It will take a big effort to avoid making the environment still more fragile.

So far, we have failed to reverse the trends and so the fragility of the environment will grow.

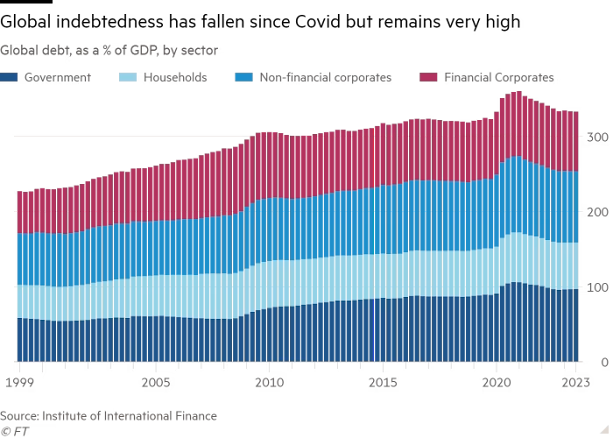

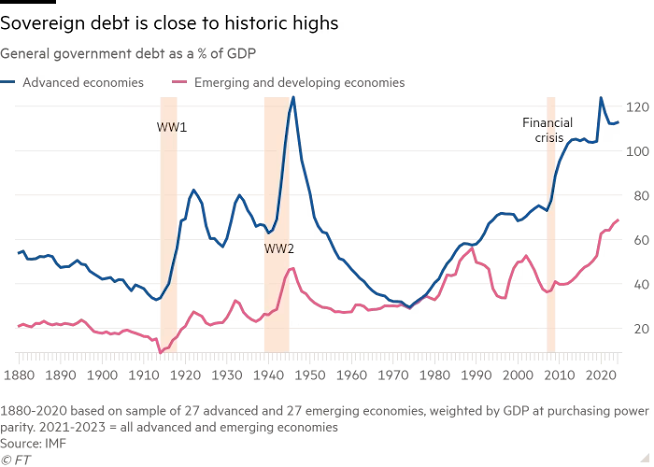

The second set is financial.

Over time, the quantity of debt, both public and private, has tended to rise.

Often, this has been sensible, indeed essential.

The difficulty is that people come to rely on both the soundness of their claims and their ability to finance and, when necessary, refinance their debts.

Economies rely on the confidence of creditors in their debtors.

If anything causes a big shock to such expectations, mass bankruptcy might trigger deep depressions, with ghastly economic and political consequences.

With today’s high indebtedness, an extended period of high interest rates might trigger such shocks.

The third set lies in domestic politics.

We are living in what Larry Diamond of Stanford has called a “democratic recession”.

There is growing hostility to fundamental norms of liberal democracy, even in western countries.

As I have argued elsewhere, this is rooted in economic disappointment, policy failures, and disruptive social changes.

That has lowered the legitimacy of conventional politicians and raised that of populist demagogues.

This then makes our politics fragile.

The final set lies in geopolitics.

The combination of changes in relative economic power with the emergence of a bloc of authoritarian powers centred on China has cemented divisions in the world.

These can be seen in today’s conflicts.

The resulting distrust threatens our capacity to summon the co-operation needed to secure “prosperity, peace and planet”.

In a world in which the dangers of conflict and the cost of failure to co-operate are so great, this final fragility might be the most important.

If we do not find a way to co-operate, we are likely to fail to manage many of the risks.

That, in turn, will make further big shocks more likely and harder to deal with.

Ours is indeed a messy and unpredictable world.

This is not because we do not know anything.

On the contrary, we know a great deal.

The problem is that we also know that the world is unpredictable and complex.

The crucial response must be to reduce fragilities, manage shocks, plan for risks and understand the fundamental drivers.

Moreover, since many of these are global, we must think globally, too.

Humanity’s habitual myopia and tribalism will not work.

Alas, it is hard to imagine we will outgrow them in the near future.

0 comments:

Publicar un comentario