The great QE write-down

Quantitative easing has cost hundreds of billions of dollars

Was it worth it?

A stack of Japanese 10,000 yen banknotes move along a conveyor at the National Printing Bureau plant in Tokyo / image: getty images

A stack of Japanese 10,000 yen banknotes move along a conveyor at the National Printing Bureau plant in Tokyo / image: getty imagesIn the decade and a half since the global financial crisis, rich-world central banks have bought trillions of dollars’ worth of bonds in an attempt to stimulate their economies.

Now the bill is coming due.

At the last count America’s Federal Reserve had a paper loss of $911bn on its $8.2trn securities portfolio.

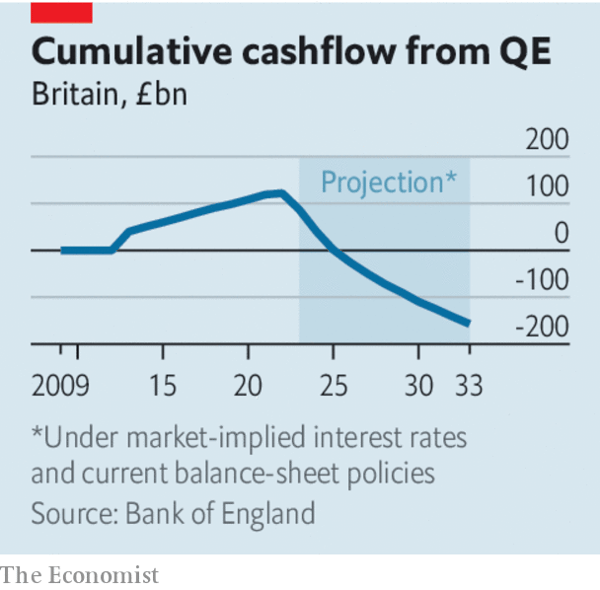

On July 25th the Bank of England said that, under reasonable assumptions, the Treasury will have to transfer about £275bn ($353bn) between 2023 and 2033 to cover the bank’s cash outflows.

On July 28th the Bank of Japan surprised markets by lifting its cap on long-term bond yields, from 0.5% to 1%.

For every 0.25-percentage-point rise in the yields of Japanese bonds across all maturities, we calculate, the central bank’s vast bondholdings will fall in value by about $58bn—an amount worth 1.5% of Japanese GDP.

Central banks can create money and so cannot go bust.

But letting them bleed cash is inflationary unless taxpayers cover the losses.

The rising costs of fulfilling this obligation make it important to determine whether quantitative easing (QE) has been worth the expense—and whether such mass bond-buying should be used the next time the economy needs stimulus.

To carry out QE, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields.

The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves.

The coupon payments they receive on the bonds, however, have remained fixed.

Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost.

Paper losses would crystallise.

Instead policymakers are doing their best to gloss over the issue.

The European Central Bank announced on July 28th that it would stop paying interest on the minimum cash balances banks are required to hold for financial-stability reasons, in effect levying a hidden tax on the banking system.

(“We’re disappointed and somewhat surprised,” said Deutsche Bank, which will lose over €200m, or $220m, per year.)

Unlike the Bank of England, the Fed will not receive infusions from the government.

Instead, when the Fed starts making profits again, it will pocket them rather than sending them to the Treasury.

Payments will resume only after the central bank has recouped the cash it is currently losing.

So far, the Fed owes itself about $80bn.

These tactics do not alter the fact that the great QE write-down is adding to the burden on fragile government budgets, which have been stretched by the financial crisis, the covid-19 pandemic and ageing populations.

The losses are all the more embarrassing since much pandemic-era QE turned out to be counter-productive.

Central banks kept buying bonds long after it was necessary: the Fed bought its last Treasury in March 2022, when inflation was already 8.5%.

Not long after, policymakers realised that they had applied too much stimulus and raised rates sharply.

That central banks lost money as inflation persisted is just another reason they came to look foolish.

Does recent experience mean qe should be forsworn the next time the economy really does need stimulus?

Central bankers should be guided by the circumstances.

The first rule they should follow is not to hold back during a financial crisis.

In late 2008 the Fed’s balance-sheet doubled in size as markets seized up and the central bank acted as a lender of last resort.

It repeated the trick—almost—in the spring of 2020, as the onset of the pandemic caused investors to “dash for cash”.

Hoovering up assets when markets panic is more likely to produce profits than losses, but even if such interventions lose money, they are worthwhile.

Even hundreds of billions of dollars would be a price worth paying to avoid a 1930s-style financial cataclysm after which unemployment soars, which today would cause damage costing tens of trillions of dollars.

When markets are calm QE’s power as a stimulant to growth and inflation is harder to judge.

The median estimate calculated in one literature review is that buying bonds worth 10% of GDP reduces ten-year government-bond yields by a mere half a percentage point.

Moreover, central banks themselves are the source of many of these estimates, and have an incentive to overstate the impact: researchers have found that the authors of papers reporting larger effects of QE on growth subsequently enjoy more promotions.

It is thus plausible that the true bang-for-buck from buying bonds is poor.

Certainly it has been recently in Japan, where the central bank has wasted money defending a bond-market peg, only to lift it and take losses.

The second rule, therefore, should be to resort to QE only when all other options have been genuinely exhausted.

Even after interest rates fall to zero and cannot be cut further, central banks can be clear about their intention to keep interest rates low for a long time—a promise which may be reinforced by QE, but is hardly dependent on it.

Governments can cut taxes or raise spending as a stimulus, as they did on a vast scale during the pandemic.

Crucially, they can fund that fiscal stimulus by issuing long-term debt, which unlike the reserves created by qe will not strain budgets if rates rise.

Bond-buying should stay in the emergency arsenal, just in case.

But in future central banks should be less trigger-happy.

0 comments:

Publicar un comentario