China Won’t Spoil the Fed’s Soft Landing

The Chinese economy’s reopening will put upward pressure on oil demand and inflation—but probably less than you think

By Nathaniel Taplin

Petroleum demand in China is deeply tied to its industrial sector./ PHOTO: CFOTO/ZUMA PRESS

Petroleum demand in China is deeply tied to its industrial sector./ PHOTO: CFOTO/ZUMA PRESSThe ghosts of past China booms are haunting U.S. investors this Christmas.

Specifically, the prospect that China’s reopening could lift oil prices—and thus complicate the Federal Reserve’s campaign to bring down inflation—has some investors tossing and turning in their sleep.

They should rest easier.

The country’s reopening will boost global oil demand, but almost certainly by much less than many market participants seem to expect.

The main point to note here is that unlike those of the U.S. and most advanced economies, China’s petroleum demand is still deeply tied to its industrial sector—the housing-driven, energy-intensive heavy industrial complex in particular.

The U.S. transport sector accounts for close to 70% of American petroleum demand.

But in China, industry and construction together accounted for nearly half of oil demand in 2020: gallons and gallons of paint and petrochemicals and fuel for excavators and other construction vehicles, for example.

Transport was just 31%.

In 2019, before the pandemic, transport was still just 34%.

All of this means that the crucial swing factor for Chinese petroleum demand is still housing and industry, rather than consumers per se—especially because China’s factory performance is tied to a lot of trucking demand as well.

Past Chinese stimulus campaigns have indeed boosted global oil prices, but that is primarily because they juiced up activity in construction and heavy industry, rather than consumer transport.

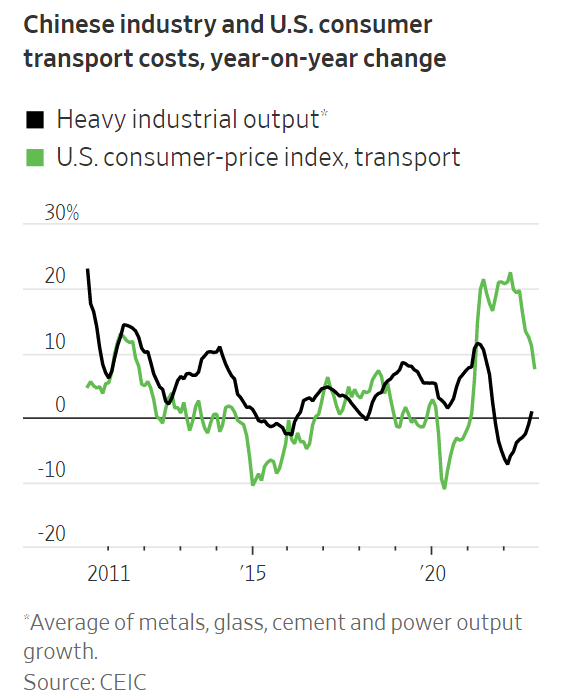

Chinese heavy industrial production has only a modest correlation to the U.S. consumer-price index as a whole, but it has tracked the transport component of CPI pretty well for much of the past decade.

And although China’s consumer sector will eventually recover once it struggles through its Covid-19 exit wave, the housing market has yet to bottom out—and a substantial rebound in actual construction will take even longer.

At the same time, Chinese exports are likely to remain lackluster as the U.S. and Europe struggle.

In other words, even assuming China’s consumer recovery next spring and summer doesn’t disappoint—which it very well could, given the scars of the past three years—the nearly half of Chinese oil demand tied to industry seems very likely to be stuck in slow-growth mode for most of 2023.

That should limit the real impact of China’s reopening on global oil demand and U.S. inflation, at least until quite late in the year.

The Fed has plenty to worry about and investors also have many reasons to doubt its ability to execute the ever-elusive soft landing.

But fear of a rampant China sucking down the world’s oil supply probably shouldn’t be one of them, barring much stronger measures from Beijing to boost the housing market and construction in early 2023.

0 comments:

Publicar un comentario