Long Covid May Be Long Tail of Risk for Insurers

Uncertainties about mortality and health risk from the pandemic might expose insurers to extended illness in coverage for workers

By Telis Demos

Patient loads were checked at a California hospital last year. Potentially millions of people may continue to suffer from long Covid./ PHOTO: K.C. ALFRED/ZUMA PRESS

Patient loads were checked at a California hospital last year. Potentially millions of people may continue to suffer from long Covid./ PHOTO: K.C. ALFRED/ZUMA PRESSThis is the third column in a three-part Heard on the Street series on long Covid.

Insurers are used to dealing with the unexpected, but trying to figure out the Covid-19 pandemic’s lasting effects might be especially challenging.

Tough questions have emerged about how the more than one million U.S. Covid-19 deaths, and millions more cases, will alter the future mortality and disability risk profile of the population.

On the one hand, Covid-19 killed many people who were already ill and there is now widespread vaccination, alongside new treatments for those who do get sick.

On the other hand, many people put off preventive treatments.

And potentially millions may continue to suffer from a constellation of symptoms considered indicators of what is known as long Covid.

“We are at an inflection point, and exactly where risk goes isn’t yet clear,” says Stuart Silverman, principal and consulting actuary at Milliman, which works with insurance companies.

Already, Covid-19’s impact on life, disability and other insurers has extended beyond deaths.

That includes things such as workers’ compensation claims.

In the past, getting sick with a contagious illness such as the flu you may have caught at work might have been unusual to claim.

But 20 U.S. states adopted some form of so-called coverage presumption measures during the pandemic generally for people such as front-line workers and others who needed to work in-person, according to the National Council on Compensation Insurance.

Brian Schneider, senior director for insurance at Fitch Ratings, estimates that in 2020 about 10% of all workers’ comp claims were related to Covid-19.

Many claims were to recover lost wages, but others involved extended medical treatments.

A study of thousands of claims by the Workers’ Compensation Insurance Rating Bureau of California found that about 11% of claims for mild Covid infections also involved workers receiving medical treatments for long Covid symptoms in the four months following acute care.

That jumped to about 36% and 40%, respectively, for severe and critical cases.

“The potential long-term cost impacts of long Covid on healthcare systems and disability insurance programs are also increasingly concerning,” WCIRB wrote in the recent study.

It also aims to further “explore estimating the extent of permanent disability associated with Covid-19” in workers’ comp.

Many special presumption measures have expired, according to the NCCI.

But greater prevalence, awareness or medical certainty about long Covid could extend discussion of these benefits.

Other forms of income-protection insurance also could be affected.

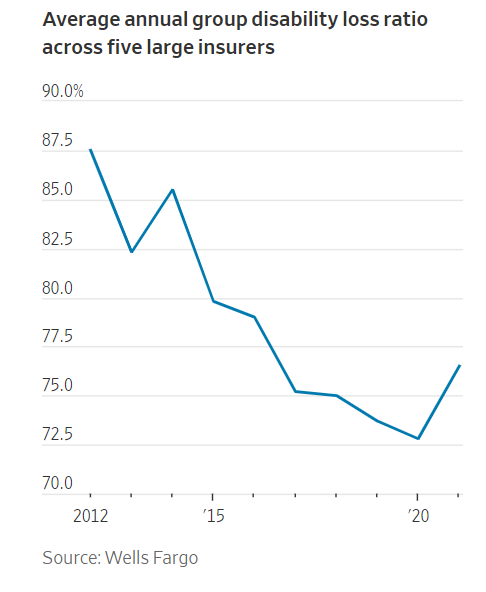

Last year, large publicly listed insurers saw an uptick in loss ratios—a measure of the cost of claims as a share of premiums collected—for group disability policies, which are often offered by employers.

The average ratio across five large public insurers was around 73% in 2020 and then jumped almost 4 percentage points in 2021, according to figures tracked by insurance analysts at Wells Fargo.

Partly that reflects normalization from low levels in the early stages of the pandemic.

But insurers also are preparing for some potential lingering Covid claims.

“We are seeing a modest amount of claims coming in from long Covid meet the definition of a long-term disability,” Christopher Swift, chief executive of Hartford Financial Services Group, told analysts on a call earlier this year, which “is dictating some of the pricing expectations that are changing” to cover some of that risk.

Insurers aren’t yet working with a universal definition of long Covid, according to Jeremy Lane, head of life-and-health products for the Americas at Swiss Re.

A clearer definition could help insurers forecast risk, similar to how they managed the emergence of conditions such as Lyme disease or chronic fatigue syndrome, he said.

There are offsetting trends, too.

The rising adoption of vaccines and other treatments may mean that people might more quickly return to work or avoid future illness.

And a strong labor market means fewer people are worried about future earnings and might be less likely to pursue disability claims.

Fears about long Covid might also drive more sales of disability policies which, if priced sufficiently, could drive profitable growth.

But this also raises the possibility that the future could see claim pressure both from job insecurity and extended illness.

Lingering illness and a weakening economy could make for a tough combination.

0 comments:

Publicar un comentario