Why China’s Central Bankers Are Still Worried

China’s economy grew 4% from a year earlier in the fourth quarter—faster than expected. But December data should give investors pause.

By Nathaniel Taplin

Passengers show their Covid-19 testing results to enter Xian North Railway Station in China./ PHOTO: STRINGER/VIA REUTERS

Passengers show their Covid-19 testing results to enter Xian North Railway Station in China./ PHOTO: STRINGER/VIA REUTERSAfter a tumultuous 2021 marked by near-disaster in the property sector and a widening crackdown on other previously fast-growing industries such as internet technology, China’s economy demonstrated a bit of spark Monday.

New figures showed fourth-quarter growth at 4% year over year, slower than the third quarter’s 4.9% but still well above the 3.3% consensus estimate among economists polled by FactSet.

Still, policy makers clearly don’t see much to celebrate: On Monday the People’s Bank of China also announced a 0.1 percentage point cut to two of its key policy rates.

The upbeat data shouldn’t be so surprising, particularly for October and November.

Although China’s economy still struggled in the fourth quarter, it benefited from the absence of two big problems from the third quarter: the midsummer Delta variant outbreak and late summer power shortages.

Resilient exports supported manufacturing investment, and the slow trickle of monetary easing since July appears to have helped stabilize weak infrastructure investment.

Single-month December data released alongside gross domestic product was largely bad, however, particularly for consumers and the all-important housing sector.

Retail sales rose just 1.7% year over year, the weakest growth in over a year.

And with China still fighting multiple Covid-19 outbreaks in mid-January—including some linked to the hyper-contagious Omicron variant—the prospects for January and February look bleak too.

More worrying, mortgage lending appears to have retreated in December, after a noticeable bump in November: Growth in seasonally adjusted medium- and long-term loans to households slowed to 9.5% from 14.3% month on month annualized, according to Goldman Sachs.

Housing sales also fell back.

With infrastructure investment still struggling to accelerate and consumers hunkering down, it is difficult to imagine a floor for overall Chinese growth without more definitive signs of a bottom in real estate.

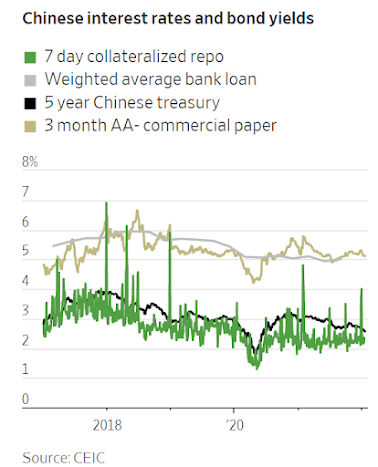

Even after today’s modest policy rate cuts, monetary easing so far still looks conservative compared with past cycles—and many market rates are still relatively high.

More help will be needed to head off a deeper slowdown in the first half of 2022.

0 comments:

Publicar un comentario