Economies can survive a stock market crash

If a correction is due to higher rates and stronger growth, it would not matter much — except to investors

Martin Wolf

“The long, long bull market since 2009 has finally matured into a fully-fledged epic bubble.

Featuring extreme overvaluation, explosive price increases, frenzied issuance, and hysterically speculative investor behaviour, I believe this event will be recorded as one of the great bubbles of financial history, right along with the South Sea bubble, 1929, and 2000.”

Thus did Jeremy Grantham, legendary investor and co-founder of GMO asset management, greet the new year.

Is he right and how much would it matter to the world if he were?

We can indeed, as Grantham told the FT, observe classic symptoms of mania: the rise of amateur traders, frenzied interest in once obscure companies, soaring prices of speculative assets such as bitcoin and hot businesses like Tesla, and the emergence of special purpose acquisition companies, or Spacs.

These are vehicles for the acquisition of unlisted companies and so a way around initial public offering rules.

They are modern versions on a vastly bigger scale of the company allegedly created during the early 18th century’s South Sea bubble, “for carrying on an undertaking of great advantage, but nobody to know what it is”.

That bubble ended badly.

Will this time be different?

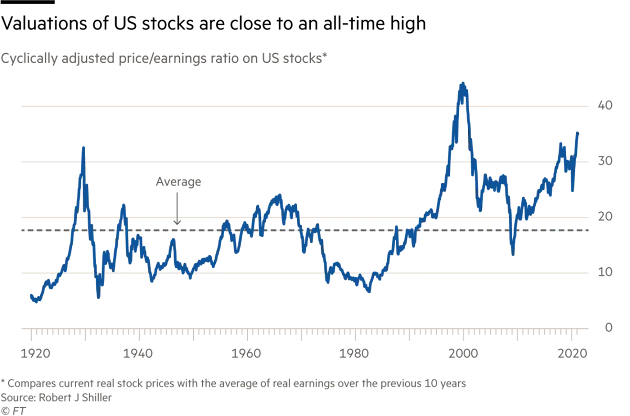

Today’s excesses can be captured in the cyclically-adjusted price/earnings ratio, invented by the Nobel-laureate Robert Shiller.

This indicator is now at peaks previously seen only in the late 1920s and late 1990s.

Yet, as I noted in December 2020 and as Shiller had previously, this might be justified by ultra-low nominal and real interest rates.

So the market must be vulnerable to a sharp rise in interest rates.

But is such a rise plausible? Yes: the recent small rise in yields in long-term government bonds could go further.

As the OECD states in its Interim Economic Outlook: “Global economic prospects have improved markedly in recent months, helped by the gradual deployment of effective vaccines, announcements of additional fiscal support in some countries, and signs that economies are coping better with measures to suppress the virus.”

This is good news.

But if, as a result, monetary policy tightened sooner and yields rose more than generally expected, that good news might be bad for markets.

Yet, even if a market correction hurt investors, would it matter that much for the economy as a whole?

As the late Paul Samuelson asserted: “The stock market has forecast nine of the last five recessions.”

Still less do market corrections imply economic depressions.

A stock market crash would only devastate the economy if policymakers let it do so — as after the crash of 1929.

The results then were so dire only because the policymakers’ response was so foolish.

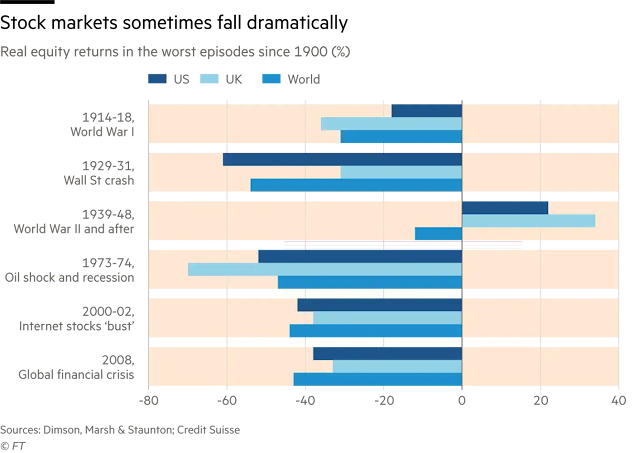

There are two ways in which a big stock market correction of the kind Grantham expects might be linked to a significant economic crisis.

The first is if it is a big enough shock on its own to cause economic meltdown. This is very unlikely: the wealth effects of falling stock markets on spending are real but modest.

The second is if the crash is part of an inflationary surge of the kind seen in the 1970s, or of a financial crisis triggered by waves of bankruptcy and the failure of financial institutions, as happened in the 1930s and threatened to recur in 2008.

Neither can be ruled out entirely.

The economic recovery from Covid-19 may prove far stronger, and the consequences for price and wage inflation more powerful, than conventional wisdom expects.

This is a bigger risk now than in the aftermath of the 2008 financial crisis.

Yet it is still a modest one.

Stress tests by central banks and the IMF on core financial institutions indicate that they are robust.

But there are other possible channels for financial disarray.

One is the high levels of indebtedness in non-financial corporate sectors of high-income countries; another is the exposure of borrowers outside the US to shocks to dollar funding.

The combination of a huge US fiscal loosening with sharper than expected monetary tightening might destabilise emerging economies.

This happened before, notably in the 1980s debt crisis.

In brief, a stock market correction is possible as Covid-19 comes under control, economies normalise and interest rates rise.

But, in itself, this is not something to worry about much, especially as the effects of a stronger than expected economy versus higher than expected interest rates should offset each other.

Far more serious would be a debt crisis that damages core institutions, freezes markets and creates mass bankruptcies.

Happily, this looks containable, given the tools available to policymakers.

Still, unexpectedly high inflation and interest rates could significantly destabilise the world economy for a while.

In the longer run, the world economy would be less fragile if spending were less dependent on aggressive monetary policies and huge accumulations of private debt.

There are three obvious ways to achieve such a reduction in fragility: improved incentives for private investment; high and sustained levels of productive public investment, and; greater redistribution of income from high-income savers to low-income spenders.

What we should want is a world economy in which Grantham can be right about the prospects for a stock market crash — yet that does not really matter.

We should also want a world economy where nominal and real interest rates can rise sharply, as economies strengthen and inflation rises, and yet all of this turns out quite well.

This may even be the world we live in.

The next few years will show us if we do.

0 comments:

Publicar un comentario