COVID-19: A Crisis the Fed Can’t Fix

By John Mauldin

For the last 3+ years, I have maintained it would take an “exogenous” event to send the United States into recession. Historically suboptimal growth? Sure, but sub-3% growth isn’t a recession.

The coronavirus obviously qualifies as an exogenous event. But that doesn’t mean a textbook two-quarter recession, although it certainly may. Financial markets aren’t waiting to find out what COVID-19 will do.

Much of the selling is fear of the unknown. The modern world hasn’t faced anything quite like this, and it’s coming at a time when the economy is vulnerable for other reasons.

Much of the selling is fear of the unknown. The modern world hasn’t faced anything quite like this, and it’s coming at a time when the economy is vulnerable for other reasons.

We actually face two concurrent crises. One is about public health, the other about the economy and markets. They won’t necessarily track each other. We might find the virus is less deadly and infectious than feared but that the fear itself (plus the control and containment measures) harms the economy.

After talking to economists and medical researchers this week, I am pretty confident in two things.

First, this is going to be a long slog. The virus will spread slowly but widely. The containment measures are simply buying time. There’s no need to panic, but we should all take common-sense protective measures.

Second, as usual, I am the “Muddle Through guy.” I think we’ll get through this. Not without some damage and tragic loss of life, but it won’t be the end of the world. This is not the zombie virus. I wasn’t thinking of viruses when I said the 2020s would be the Decade of Disruption, but COVID-19 may mark the beginning of it.

Here’s the worst part: The Federal Reserve and other central banks can’t bail us out this time. Their tools aren’t designed for this kind of problem. Powell, Lagarde, Kuroda, and others are all making their ritual pledges to “stand ready” with support. They may even be serious. But they have little to offer. Rate cuts are not vaccines.

We may soon, after a dozen years in monetary policy training wheels, find out if we can still ride a bike.

Y2K Redux

Longtime readers may recall these letters began in the late 1990s when I was writing about the “Y2K” computer problem. Looking back, it is hard to believe how much fear it generated. Some people literally headed for the hills. I said, consistently, we would have problems but get through them. And that’s more or less what happened. A few little glitches, then it was over.

However, the problem was real. Many vital systems would have stopped working on 1/1/2000 had they not been painstakingly rebuilt. We avoided catastrophe because smart people got to work and prevented it. Having that fixed date helped focus their efforts. The coronavirus is different in that regard; experts are sure it will spread, but they can’t say how fast.

This week I spoke with (among other experts) Dr. Joseph Kim, the CEO of Inovio. His company (like several others) is working on a COVID-19 vaccine. He’s been in this field many years and knows how these diseases spread. And he believes this one is not going to care about borders. The outbreaks we are now seeing in South Korea, Italy, and other places are only the beginning. Similar clusters will eventually appear in the US.

This virus’s unique challenge is its ability to spread via “asymptomatic” carriers. With SARS and Ebola, it’s very obvious that someone is sick and contagious. They are relatively easy to avoid. Infection mainly happens with medical personnel and family caregivers. With COVID-19, you can seem perfectly healthy, have no fever or other symptoms, but still carry the virus and spread it to others.

You can also catch the virus, recover, and never know you were infected. We don’t know how often that happens, which makes evaluating the data difficult. The Chinese data seems to show about a 2% fatality rate among the people who show symptoms and are diagnosed positive. That’s not necessarily everyone who is infected, so the true fatality rate could be lower.

Dr. Mike Roizen said the problem is we don’t know how many people actually have had the virus and how many died as a result. In calculating a fatality rate, we know neither the numerator nor the denominator with truly accurate precision for the equation. As we get more accurate data, we can make better assessments.

That being said, Dr. Roizen and Dr. Kim both told me this virus is far deadlier than our standard influenza. It appears about 20% of symptomatic people are sick enough to need hospital care, even though most ultimately recover. That’s enough to potentially strain our healthcare resources, generating second-order effects as people with other medical conditions have to wait for treatment.

COVID-19 is unlikely to disappear in warm weather. Hong Kong is always warm and that does not seem to be stopping the virus. The likeliest scenario is that the world now has, in effect, another flu-like virus that will be with us for years. If clinical trials are positive, one or more of the vaccines currently in development could be ready later this year. Many biotech companies are working on it. Moderna said it plans Phase 1 trials to start in April. Dr. Kim cautiously (which is his way) said Inovio’s trials should begin in late spring or early summer.

Multiple vaccines will compete, and we will see which is the most effective. But we are, at minimum, several months away from that point, and the virus is still spreading.

In the absence of reliable information, well-meaning people will try to fill the void and make matters worse. A lot of misinformation is spreading on social media, and sometimes in real media, too. I saw one story calling it an “infodemic.” That’s funny but accurate.

We have better data on the economic impact.

Supply Chains Unlinked

We see many comparisons of this virus to the 2003 SARS outbreak. That one also began in Asia and quickly spread worldwide. There was great concern at the time, but the economic damage proved minor.

China’s economy is both much bigger now and more integral to world trade. Chinese GDP is up 4X since then, and its share of worldwide trade flows has grown 10X.

Businesses all over the world depend on Chinese-made components and raw materials, many of which can’t be sourced elsewhere, at least not at the same prices.

And “just in time” production means producers don’t have much inventory on hand.

Right now, it is dwindling as Chinese factories and ports are either shut down or operating at much-reduced capacity.

Here’s how one expert described it to South China Morning Post.

“It really is death by a thousand cuts,” said John Evans, managing director of Tractus Asia, a company that has 20 years’ experience helping firms move to China, but which over the past two has had more enquiries from businesses looking to leave. “This is a black swan event and I don’t think we’ve seen anything like it in recent history, in terms of the economic and supply chain impact in China and across the globe.”

As I write this, China’s travel restrictions have eased, and businesses are starting to reopen. But schools remain closed, which suggests they are not confident the outbreak is truly under control. Beijing is letting local governments set their own rules, so conditions vary greatly across the country.

The economic problem is that inability to obtain one critical component can shut down an entire factory. In this situation, 95% or even 99% may not be good enough. We could be weeks away from some US and European producers running out of input materials. Then what? Plant closures and probably layoffs.

Worse, some Chinese producers depend on parts from the West, which they may stop buying if their own factories stay closed. That’s not only a potentially huge problem for US semiconductor makers but others as well.

And it’s not just China and not just the virus. Growth was already weakening for other reasons, such as the trade war.

Here’s David Rosenberg.

The bottom line is that the coronavirus occurred with much of the world experiencing anemic growth after a year in which supply chains were already negatively affected by all the tariff actions.

“Phase One” did not completely ameliorate that condition. World growth was the weakest in a decade in 2019 and the latest move by the IMF was to trim this year’s outlook. And that was before the coronavirus, which has imposed tail risks for the global economy and financial markets.

A tail risk in the sense that we have such little knowledge about this coronavirus, why it is spreading, or how to treat it. The spread of the virus outside of China to South Korea, the other economic giants in Asia, and to Italy, is particularly worrisome.

The only thing we know with certainty is that South Korea is a massive exporter and much of its outbound manufacturing shipments are inputs into the global production process. So, the implications for disruption to global supply chains are significant, irrespective of the slowing in the rate of infections in China.

The cat is out of the bag.

David’s point about South Korea is important. The outbreak there could well lead to the kind of industrial paralysis seen in China. That would have a quick and severe impact on companies in Japan, North America, Europe, and everywhere else. The Italy outbreak could have a similar but smaller result. Italian authorities responded quickly, but people infected there have already spread it throughout Europe.

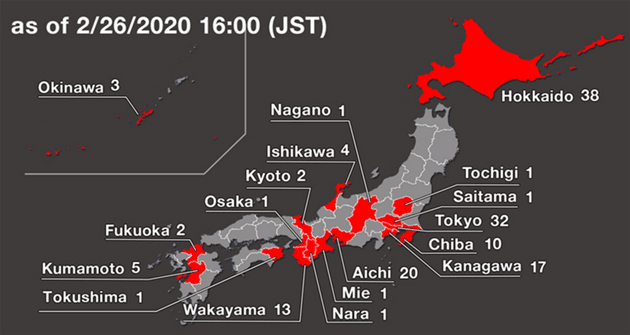

Meanwhile, here’s a map of cases in Japan (excluding cruise ship passengers). Note the cluster in Aichi. That’s Toyota headquarters and a heavy manufacturing region.

Japanese Prime Minister Shinzo Abe has asked schools to close throughout Japan.

If the map keeps reddening, factory workers may be told to stay home, too, even if their plants can get the parts they need.

This would cascade through the world economy.

Fed Futility

We all learn by experience. For a dozen years now, investors have been rewarded for buying every market dip. Indexes always recovered to new highs, often because central banks delivered some kind of stimulus, or at least promised to do so.

So in one sense, seeing this week’s losses as another buying opportunity is rational. Possibly time will show that’s what it was, but count me dubious.

We have known for a long time something would pop the balloon. It proved to be Teflon-coated, impervious to everything bears could throw at it. But bears didn’t create this virus.

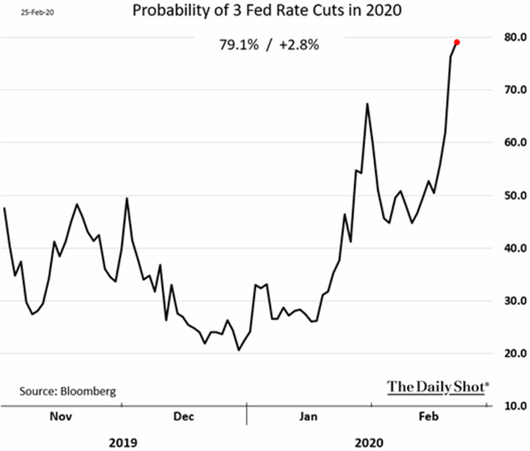

Nonetheless, investors are increasingly convinced the Fed will respond with more rate cuts. At year-end 2019, the futures-implied probability of three rates cuts this year was only 20%.

Now it’s up to 80%.

Note, any rate cuts would be on top of the existing T-bill purchase program and repo market liquidity injections. I think those are more likely to be expanded than reduced.

If it happens, the Fed will be in full-on stimulus mode, akin to 2008–2009.

But it probably won’t have the same kind of effect.

Peter Boockvar explained this week.

A rate cut won't bring Chinese factories back online any quicker. And a rate cut won't get people flying and traveling again until the virus peters out. Either way, the US bond market has already eased for them. The US 10-year yield at 1.37% [now 1.18%! – JM] has essentially cut rates by 25 [45] bps over the past two weeks for those looking to refi or purchase a home.

Lower rates may ease the cost of buying a car but with car prices at record highs (not hedonically adjusted), it won't do much. Credit card rates with 3 Fed rate cuts are still near 17% so another rate cut or two won't help much here.

And with respect to a rate cut encouraging more capital spending, the cost of capital clearly hasn't been a binding constraint on any capital decision for years. Will a rate cut or two 'ease financial conditions', aka goose asset prices? Maybe but maybe not.

Monetary policy tools just aren’t designed for this situation. All they can do is stimulate demand, and virus containment measures will make any such demand hard to fill. Fiscal stimulus might help but would also increase the already massive deficit.

In China, the government and central bank are responding with targeted loans to affected businesses rather than macro policy changes. That’s probably the right move, but with debt at such high levels, they really had no choice.

That’s the big risk here. I think investors are about to learn central banks won’t always be there for them in every situation. If the delicate faith that’s kept markets rising should break, then what? It’s a long way down.

So what do we do? In my case, this doesn’t change investment strategy. I am not a buy-and-hold advocate. I’m in funds and professionally managed accounts that can move out of the markets or directly hedge when necessary. Some have already done so. I expect others will do likewise if conditions worsen.

As an aside, bond markets are acting as if this is a massively deflationary event.

Some Silver Linings

- We must remember that 86% of Americans are employed in the service industry/related areas. The manufacturing industry won’t simply shut down, either. Absent multiple large outbreaks in cities across the US, which would cause serious changes in consumer behavior, the US could prove more resilient than some others. This will be contained at some point and business and consumer life move on.

- Last week, only a few US labs could test for the coronavirus. Clearly, we were massively unprepared, but that is changing fast. As you read this, already 93 labs should have testing facilities. A bedside diagnostic is coming, too, as 70 companies are working on it. The FDA is changing its procedures to allow confirmation at labs other than at the CDC’s main headquarters. This will ease concern by quickly separating actual COVID-19 cases from common colds and flu.

I expect the number of labs which can administer tests to increase dramatically over the next few weeks. New testing kits will come online. I can imagine hospital administrators and staff are beginning to think about how they would handle an outbreak in their city.

- There is a high probability that vaccines will be available by the end of the year/early next year. We may all be getting an annual vaccine for COVID-19 along with the flu shot.

- This may seem counterintuitive, but in a certain sense, COVID-19 provides a massive wake-up call to the world. We were not prepared. I, perhaps optimistically, think that will be different in the future. This is not the “zombie virus” of the post-apocalyptic movie genre, but it should make mankind in general, and countries in specific, start thinking about the next, perhaps more serious outbreak.

- On the economic front, I think it is safe to say that supply chains will be radically different by 2022. Technology was already bringing manufacturing closer to the consumers. I expect that trend to accelerate. That should mean significant capital investment after the COVID-19 problem is contained, providing a nice economic stimulus.

- Governments everywhere (including the US) need to think about the supply chain vulnerability of certain critical necessities. I don’t mean T-shirts and auto parts. I am thinking of medicines and medical supplies, many of which are now produced in China. Do we need multiple sources? Are some items so critical we should produce them in multiple places within countries? Just asking… This should begin now.

- As of Friday, there were 60 cases of coronavirus in the United States, the bulk of which were from one cruise ship. All but one could be traced to either a cruise ship or a person or spouse coming from China. We should expect more, but for now, it seems to be spreading slowly here.

- I think the base case is that China and Europe enter recession. I would think the US is a coin toss. Because we don’t know of the extent of the potential outbreak, it’s really hard to say. The foreign slowdown will have an effect, but recession isn’t inevitable.

On a personal level, I think we should all just exercise common sense. I asked Dr. Kim if he was cutting back on his travel, including his international travel. His answer was no, life has to go on. Other frequent international travelers I know expressed the same sentiments. Some say they will avoid China, more because they don’t want to land in quarantine upon return than fear of getting the virus. Mike Roizen said he will still be traveling within the US, where he is already scheduled.

Of course, follow official advice if you live in an affected area, but we can’t all seal ourselves into bubbles. I will be traveling to New York in two weeks and plan many dinner meetings as well as other business meetings. As my wife Shane said about my future travel, “Stay calm and wash your hands.”

I have no way of knowing how far the market will fall. But I do expect this current problem will be solved and life will return to normal. This will represent a good, and perhaps great, buying opportunity.

How to Find the Opportunity I See Everywhere

Okay, I just spent a letter talking about the crisis du jour. But it doesn’t change my long-term outlook. I am still bullish on humanity and bearish on government. The problems and the opportunities I see everywhere aren’t going away. I seem to find more every week.

I have structured this year’s Strategic Investment Conference to both help you avoid the problems and find the opportunities. We will talk about more specific investment opportunities than in previous years. Today, I don’t want to go into a long list of the fabulous speakers and faculty who will be there, as you can see them on the website. While the information they give us will be invaluable, most attendees say they get as much or more from their discussions with their fellow attendees… people like you who can share their ideas.

I learn more at the conference, too. Attendees point me to new thoughts and research. They show me new opportunities. I truly think this year’s SIC will the best and most informative ever. You need to be there May 11–14 at the fabulous Phoenician resort in Scottsdale, Arizona. Get there a day early and golf with me. Pamper yourself and your spouse at their fabulous spa while you pick up portfolio-boosting ideas.

Don’t procrastinate. There has never been a better year to come to the SIC. Learn more here.

Instead of my normal personal section, I will simply wish you a great week and hit the send button.

Your Muddle Through analyst,

|

John Mauldin

Co-Founder, Mauldin Economics |

0 comments:

Publicar un comentario