Fundamentals are clearly deteriorating for top lenders. Goldman Sachs’ recent diversification drive makes it only a partial exception.

By Aaron Back

JPMorgan lowered its outlook for net interest income this year to $57.5 billion. Photo: Victor J. Blue/Bloomberg News

Banks are showing symptoms of late-cycle exhaustion.

Quarterly results from a trio of big U.S. lenders showed slowing loan growth and declining net interest margins. Goldman Sachslooks less impacted than peers thanks to a well-timed diversification drive but, if the economic cycle does turn, none look attractive.

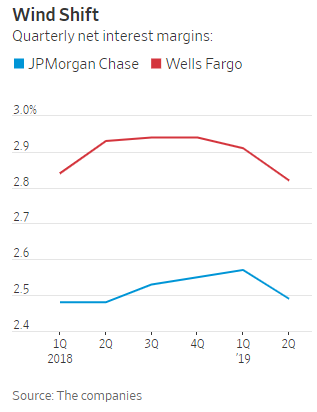

JPMorgan Chaseand Wells Fargoboth reported muted second-quarter results on Tuesday that beat analyst estimates yet did little to excite investors. At JPMorgan core loans rose just 2% from a year earlier, slowing from 4% growth the prior quarter and 8% for all of 2018. At Wells Fargo loan growth remained essentially flat for the second straight quarter. Shares of the two lenders were little changed Tuesday morning.

Net interest margins also ticked down at both banks, at least partly due to lower long-term rates during the quarter. At JPMorgan the margin fell to 2.49% from 2.57% the prior quarter, and at Wells Fargo to 2.82% from 2.91%. In particular, Wells Fargo cited the impact of early refinancing of mortgages which force the bank to reinvest mortgage-backed securities at lower rates.

Most significantly, JPMorgan lowered its outlook for net interest income this year to $57.5 billion, from an earlier forecast of more than $58 billion. On a conference call, new Chief Financial Officer Jennifer Piepszak clarified that if there is more than one Federal Reserve rate cut this year, the actual income figure would be even lower. Markets currently deem three rate cuts by the end of the year to be the most likely scenario, according to CME Group. If that comes to pass, there is further downside to bank earnings.

These headwinds are less impactful for Goldman Sachs, though, because much of its lending business is brand new, particularly to consumers. This gives it more white space to expand into and makes year-earlier comparisons less challenging. In the second quarter, Goldman’s net interest income soared 39.5% from a year earlier to $872 million. Its shares were up around 2% Tuesday morning.

The timing of Goldman’s expansion into consumer lending is also fortuitous, as that business remains a bright spot for many banks. The risk is that an economic downturn will cause losses, especially on the kind of unsecured consumer lending with which Goldman is experimenting.

Given the small scale of this lending, though, any fallout would be manageable for the bank, at least in this cycle. On the other hand, many of Goldman’s core businesses, from trading to investment banking, are highly cyclical. Its shares are no place to hide out if a recession is coming.

That goes for the whole banking sector of course. On a conference call with reporters Tuesday, JPMorgan Chief Executive James Dimon dismissed fluctuations in net interest income as mere “wind,” encouraging investors instead to focus on measures of its fundamental business expansion such as branch openings and deposit growth. That may be true over the long run, but for now, investors would do well to notice which way the wind is blowing.

0 comments:

Publicar un comentario