Stocks Have Had Enough Of The Bond Rally

by: The Heisenberg

Summary

- This week, the global growth scare went into overdrive.

- Bonds are on fire, thanks to a trade war that is no longer just a trade war, according to the likes of Ray Dalio.

- Stocks, it would appear, are in no mood to stomach any further trade escalations and would really appreciate it if the bond rally abated.

- Bonds are on fire, thanks to a trade war that is no longer just a trade war, according to the likes of Ray Dalio.

- Stocks, it would appear, are in no mood to stomach any further trade escalations and would really appreciate it if the bond rally abated.

If there's one overarching theme that pervades almost all of the commentary I've read this week, it's that market participants have finally woken up to why recent escalations in the dispute between Washington and Beijing matter more than previous escalations.

Note that I didn't include the word "trade" before "dispute". That's because it's now clear that at least one party to this worsening quarrel has designs on curtailing the other side's economic development.

In other words, this isn't just about righting historical trade injustices or leveling the proverbial playing field.

In other words, this isn't just about righting historical trade injustices or leveling the proverbial playing field.

If you don't believe me, just ask Ray Dalio, who on Wednesday said the following:

As I have explained for a while, the US-China conflict is much more extensive than a 'trade war.' It is an ideological conflict of comparable powers in a small world. It’s about 1) China emerging to challenge the power of the US in many areas and 2) these two countries having two different approaches to life - one that’s top down and one that’s bottom up.

Without weighing in on the multitude of normative questions that arise when one country cites "national security" and trade "fairness" to justify actions clearly designed to undermine another nation's global economic ambitions, suffice to say Beijing is fully apprised of the possibility that this isn't all about reducing the bilateral trade deficit. Over the past three weeks, Chinese state media has run accusatory commentary after accusatory commentary in an effort to lay bare what China believes is an increasingly nefarious crackdown.

Importantly, none of the above is debatable. I'm not expressing an opinion here. Indeed, that's the whole point. Over the past two weeks, analysts and traders have come to begrudgingly accept what experts (e.g., former government officials who have spoken to media outlets about the situation) have been saying all month. Namely that the Huawei ban, the Hikvision news and other prospective actions on the US side, and, on the Chinese side, overt nods to weaponizing (economically speaking) China's dominance over rare earths are all manifestations of a widening conflict that goes well beyond the Trump administration's desire to shrink the deficit.

The rare earths story has grabbed all manner of headlines over the past 48 hours. For anyone who wants a reasonably comprehensive take on the situation, you can find one here, but for our purposes, just note that what's critical for markets isn't so much the threat of China actually playing the rare earths card. On Tuesday and Wednesday, Chinese media effectively confirmed that Xi's visit to a rare earths processing plant earlier this month was intended to send a message. Part of that message involves simply reminding the US that China accounted for nearly 80% of global REE mine supply last year. But markets heard something more. Simply put, markets interpreted the rare earths news as just another indication that this dispute is spiraling further and further out of hand.

As Dalio put it in the same linked post excerpted above, "history shows that countries in conflict have seen that such conflicts can easily slip beyond their control." Ray means that in a broader (and scarier) sense, but sticking with markets, the concern now is that what was everyone's worst-case scenario is now the base case. It appears to be a foregone conclusion that at least some further escalations are coming, with the most well-telegraphed being tariffs on the remainder of Chinese exports to the US.

I've been over and over the various estimates of how an all-out trade war will mechanically impact growth and inflation (see here, for instance). And I've also spilled gallons of digital ink explaining that it is impossible to catalogue all of the second-order effects (e.g., how a trade-related selloff across equity markets could accelerate thanks to the liquidity-volatility-flows feedback loop, how a widening of credit spreads occasioned by risk-off behavior could have ramifications for an over-leveraged corporate sector, etc.). Some of those discussions are tedious. But there wasn't anything tedious or subtle about how expectations of further trade friction impacted markets on Tuesday and Wednesday, when traders witnessed bonds attempting to price in the assumed deleterious effect of a worst-case scenario on global growth.

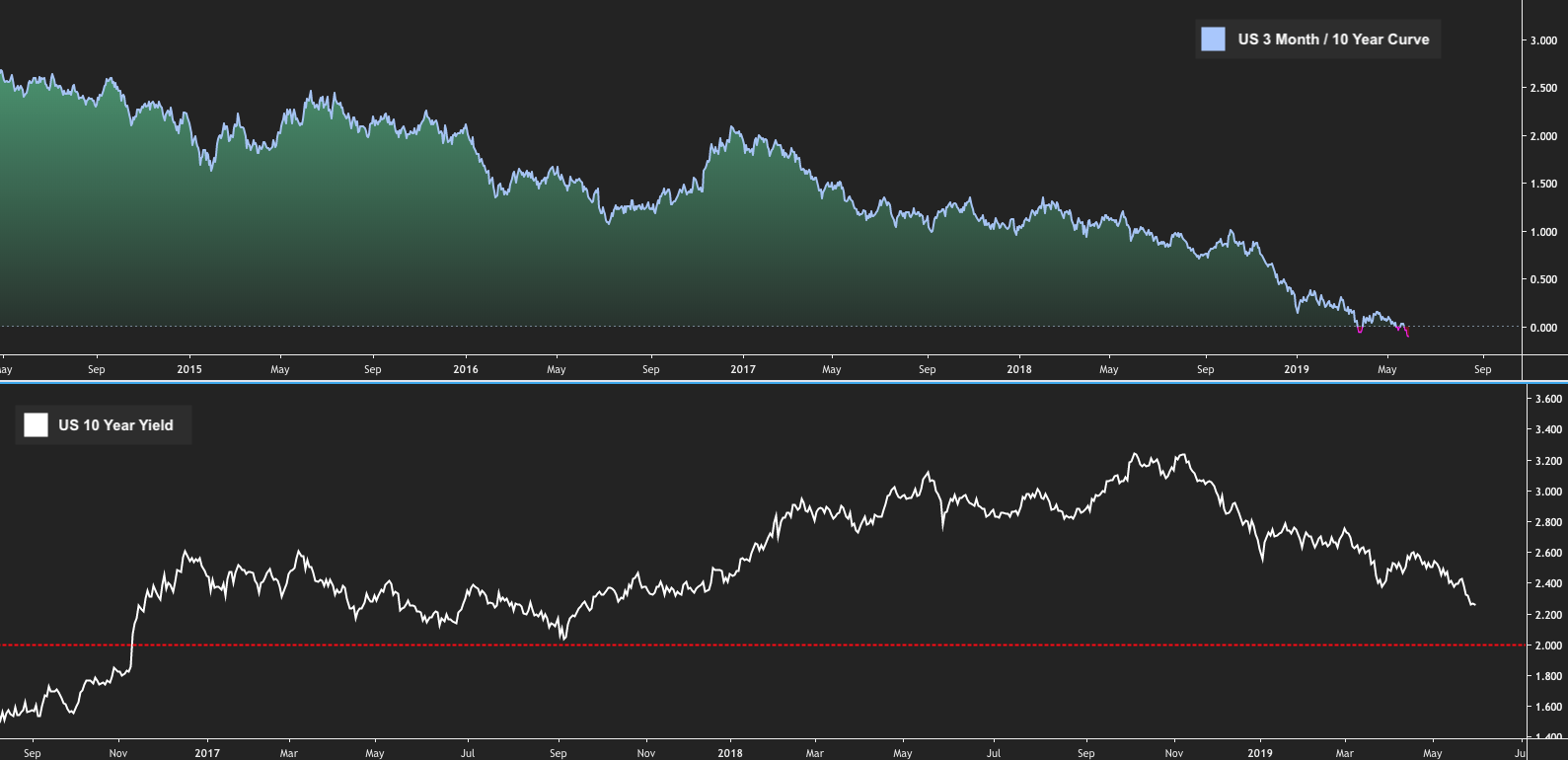

There's little utility in documenting each and every notable highlight from the action across rates and bonds for this platform. There were myriad events worth flagging, including Aussie 10-year yields trading through the RBA cash rate, a similar situation in South Korea and German yields nearing record lows, and those who want the full treatment can read more in "Marking To Misery". But for the sake of brevity, US investors should simply note the fresh "since 2017" lows in US 10-year yields and, relatedly, the deepening inversion of the 3-month/10-year curve.

(Heisenberg)

Obviously, the 3-month/10-year inversion feeds into the "imminent recession" narrative, and Bloomberg ran an entire feature article on Wednesday about the prospect of 10-year yields sinking below 2%.

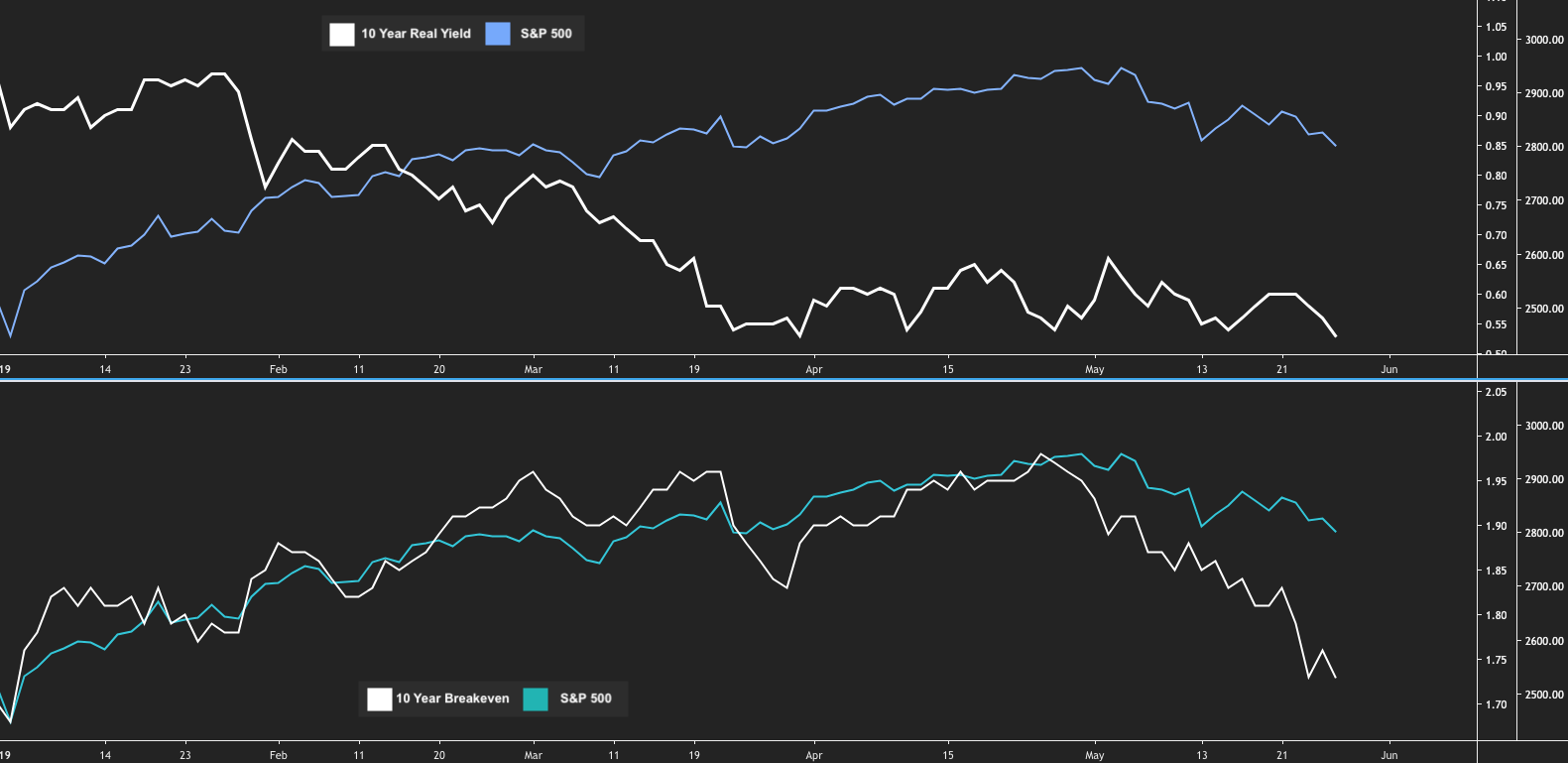

When you think about this, do note that what's changed lately is that breakevens have fallen sharply since late last month. All year long, casual observers pointed to the disconnect between equities and bond yields and insisted that "something had to give". Over that period, declining real yields were bolstering risk appetite, while rising breakevens (in tandem with crude prices) made a case for stabilizing growth expectations. Recently, however, breakevens have led the way lower for yields, and that isn't something stocks are prepared to stomach given what it says about growth.

(Heisenberg)

That's why you're seeing stocks now starting to "catch down" to bond yields. Goldman underscored the point in a note out Monday evening. "As breakeven inflation closely follows market measures of global growth, it has now taken the lead for the recent decline in US rates, which moved lower alongside equities", the bank wrote.

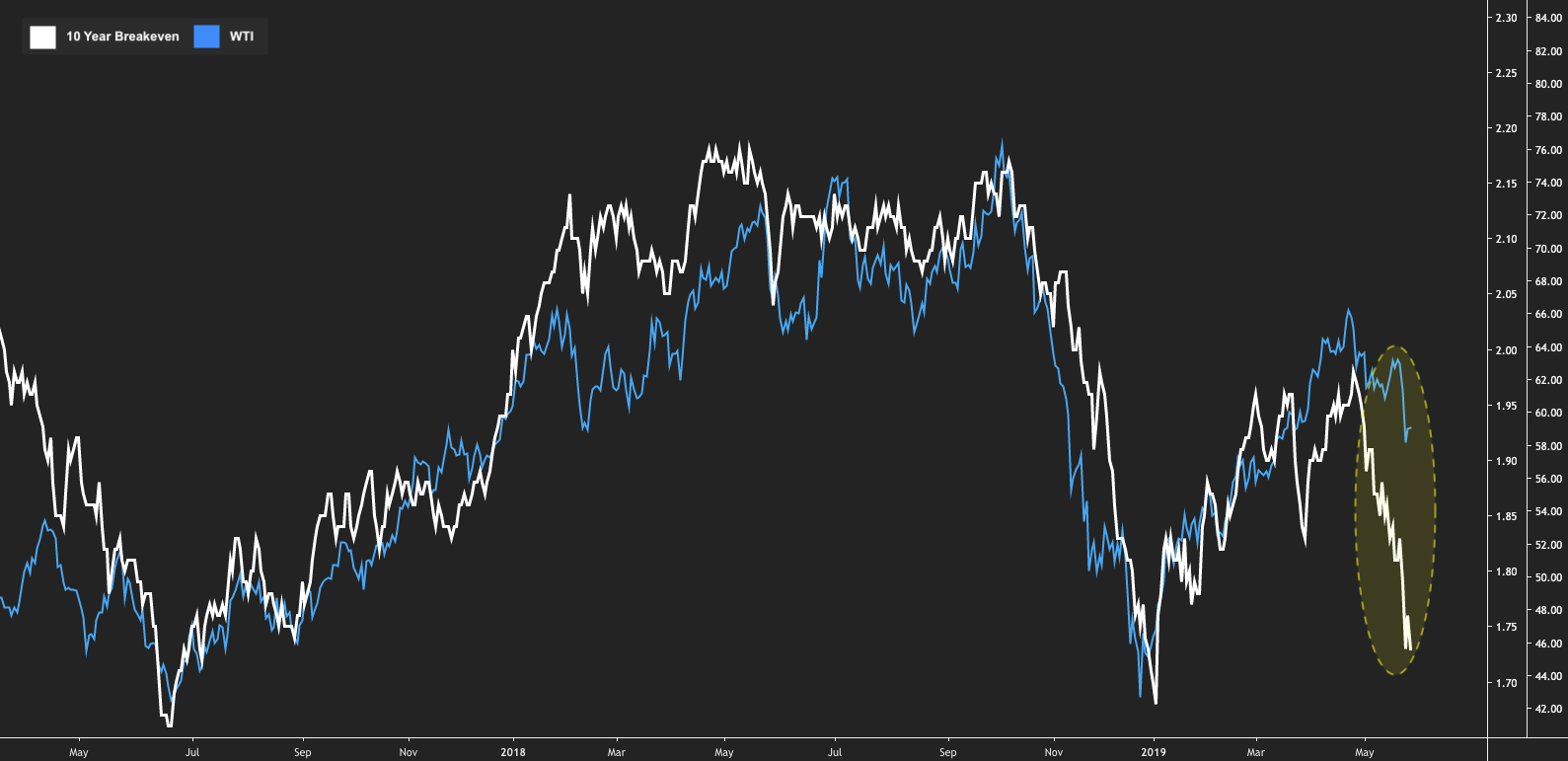

It's also worth noting that this isn't just down to oil. Sure, crude has sold off recently on global growth jitters (despite persistent supply concerns tied to Venezuela and Iran), but the rapidity of the drop in breakevens outpaces the declines in crude.

(Heisenberg)

You should also note that the convexity flows dynamic I've talked about in these pages a couple of times (and on my site ad nauseam) likely comes into play on a further rally down to 2.20% (or so) on 10s. Any further signs of weakness in the US economy will obviously exacerbate this situation.

All of that said, and while completely acknowledging that the standoff between Washington and Beijing now threatens to spiral, undercutting the global economy in the process, I would still note that even if things do continue to deteriorate, the recent bond rally has run a long way in a short period of time. Simultaneously, rampant expectations for Fed easing and bets on multiple rate cuts from, for instance, the RBA suggest many market participants are now expecting the worst for the global economy and believe this is going to be a one-way trade from here on out.

Although I wouldn't be totally surprised to see 10-year US yields below 2% in six months, I wouldn't be surprised to see them far higher than they are now either.

Although I wouldn't be totally surprised to see 10-year US yields below 2% in six months, I wouldn't be surprised to see them far higher than they are now either.

One thing is for sure: Stocks have had enough of the bond rally for now. Especially to the extent it's predicated on well-founded global growth worries.

0 comments:

Publicar un comentario