New and untested players, some backed by Wall Street, have helped borrowers pile up billions in loans. What could go wrong?

By Matt Phillips

A decade after reckless home lending nearly destroyed the financial system, the business of making risky loans is back.

This time the money is bypassing the traditional, and heavily regulated, banking system and flowing through a growing network of businesses that stepped in to provide loans to parts of the economy that banks abandoned after 2008.

It’s called shadow banking, and it is a key source of the credit that drives the American economy. With almost $15 trillion in assets, the shadow-banking sector in the United States is roughly the same size as the entire banking system of Britain, the world’s fifth-largest economy.

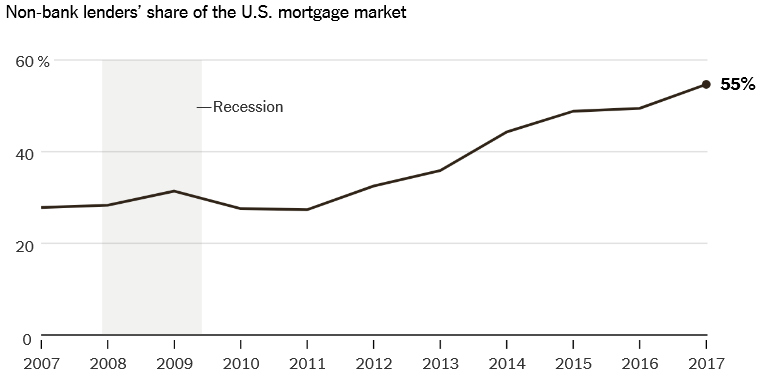

In certain areas — including mortgages, auto lending and some business loans — shadow banks have eclipsed traditional banks, which have spent much of the last decade pulling back on lending in the face of stricter regulatory standards aimed at keeping them out of trouble.

But new problems arise when the industry depends on lenders that compete aggressively, operate with less of a cushion against losses and have fewer regulations to keep them from taking on too much risk. Recently, a chorus of industry officials and policymakers — including the Federal Reserve chair, Jerome H. Powell, last month — have started to signal that they’re watching the growth of riskier lending by these non-banks.

“We decided to regulate the banks, hoping for a more stable financial system, which doesn’t take as many risks,” said Amit Seru, a professor of finance at the Stanford Graduate School of Business. “Where the banks retreated, shadow banks stepped in.”

Safe as houses

With roughly 50 million residential properties, and $10 trillion in amassed debt, the American mortgage market is the largest source of consumer lending on earth.

Lately, that lending is coming from companies like Quicken Loans, loanDepot and Caliber Home Loans. Between 2009 and 2018, the share of mortgage loans made by these businesses and others like them soared from 9 percent to more than 52 percent, according to Inside Mortgage Finance, a trade publication.

Is this a good thing? If you’re trying to buy a home, probably. These lenders are competitive and willing to lend to borrowers with slightly lower credit scores or higher levels of debt compared to their income.

They also have invested in some sophisticated technology. Just ask Andrew Downey, a 24-year-old marketing manager in New Jersey who is buying a two-bedroom condo. To finance the purchase, he plugged his information into LendingTree.com, and Quicken Loans, the largest non-bank mortgage lender by loans originated, called him almost immediately. “I’m not even exaggerating,” he said. “I think they called me like 10 or 15 seconds after my information was in there.”

Quicken eventually offered him a rate of 3.875 percent with 15 percent down on a conventional 30-year fixed-rate mortgage of roughly $185,000. Eventually he found an even better offer, 3.625 percent, from the California-based lender PennyMac, also not a bank.

“I really didn’t reach out to any banks,” said Mr. Downey, who expects to close on his condo in Union, N.J., this month.

The downside of all this? Because these entities aren’t regulated like banks, it’s unclear how much capital — the cushion of non-borrowed money the companies operate with — they have.

If they don’t have enough, it makes them less able to survive a significant slide in the economy and the housing market.

While they don’t have a nationwide regulator that ensures safety and soundness like banks do, the non-banks say that they are monitored by a range of government entities, from the Consumer Financial Protection Bureau to state regulators.

They also follow guidelines from the government-sponsored entities that are intended to support homeownership, like Fannie Mae and Freddie Mac, which buy their loans.

“Our mission, I think, is to lend to people properly and responsibly, following the guidelines established by the particular agency that we’re selling mortgages to,” said Jay Farner, chief executive of Quicken Loans.

Risky business loans

It’s not just mortgages. Wall Street has revived and revamped the pre-crisis financial assembly line that packaged together risky loans and turned those bundles into seemingly safe investments.

This time, the assembly line is pumping out something called collateralized loan obligations, or C.L.O.s. These are essentially a kind of bond cobbled together from packages of loans — known as leveraged loans — made to companies that are already pretty heavily in debt. These jumbles of loans are then chopped up and structured, so that investors can choose the risks they’re willing to take and the returns they’re aiming for.

If that sounds somewhat familiar, it might be because a similar system of securitization of subprime mortgages went haywire during the housing bust, saddling some investors with heavy losses from instruments they didn’t understand.

If investors have any concerns about a replay in the C.L.O. market, they’re hiding it fairly well.

Money has poured in over the last few years as the Federal Reserve lifted interest rates. (C.L.O.s buy mostly loans with floating interest rates, which fare better than most fixed-rate bonds when interest rates rise.)

Still, there are plenty of people who think that C.L.O.s and the leveraged loans that they buy are a potential trouble spot that bears watching.

For one thing, those loans are increasingly made without the kinds of protections that restrict activities like paying out dividends to owners, or taking out additional borrowing, without a lender’s approval.

Roughly 80 percent of the leveraged loan market lacks such protections, up from less than 10 percent more than a decade ago. That means lenders will be less protected if defaults pick up steam.

For now, such defaults remain quite low. But there are early indications that when the economy eventually does slow, and defaults increase, investors who expect to be protected by the collateral on their loan could be in for a nasty surprise.

In recent weeks, warnings about the market for C.L.O.s and leveraged loans have been multiplying. Last month, Mr. Powell said the Fed was closely monitoring the buildup of risky business debt, and the ratings agency Moody’s noted this month that a record number of companies borrowing in the loan markets had received highly speculative ratings that reflected “fragile business models and a high degree of financial risk.”

Small, subjective loans

Leveraged loans are risky, but some companies are seen as even too rickety, or too small, to borrow in that market.

Not to worry. There’s a place for them to turn as well, and they’re called Business Development Companies, or B.D.C.s.

They’ve been around since the 1980s, after Congress changed the laws to encourage lending to small and midsize companies that couldn’t get funding from banks.

But B.D.C.s aren’t charities. They’re essentially a kind of investment fund.

And they appeal to investors because of the high interest rates they charge.

Their borrowers are companies like Pelican Products, a maker of cellphone and protective cases in California, which paid an interest rate of 10.23 percent to its B.D.C. lender, a rate that reflects its high risk and low credit ratings.

For investors, an added appeal is that the B.D.C.s don’t have to pay corporate taxes as long as they pay 90 percent of their income to shareholders. Shareholders eventually pay tax on that income, but in a tax-deferred retirement account like an individual retirement account, the structure can amplify gains over time.

So, naturally, B.D.C. assets have grown fast, jumping from roughly $10 billion in 2005 to more than $100 billion last year, according to data from Wells Fargo Securities and Refinitiv, a financial data provider.

Some analysts argue that risks embedded in B.D.C.s also can be hard to understand. Because B.D.C.s own loans in small companies that aren’t always widely held or traded, there are often no public market prices available to use to benchmark the fund’s investments.

B.D.C.s have also been increasing leverage to bolster returns. It means they’re using more borrowed money, to make these loans to high-risk borrowers. That strategy can supercharge returns during good times, but it can also make losses that much deeper when things take a turn for the worse.

0 comments:

Publicar un comentario