How BlackRock’s $15.2bn purchase of BGI transformed the global asset management industry

Attracta Mooney and Peter Smith

Larry Fink bet his entire firm on the BGI acquisition and it took tremendous courage © Alex Wheeler/FT, AP, Bloomberg

During the dark days of the financial crisis, BlackRock boss Larry Fink flew to San Francisco. As banks and insurers grappled to stay afloat and governments and central banks propped up the financial system, Mr Fink had his eye on a big prize.

His destination was the headquarters of Barclays Global Investors, the asset management arm of troubled British bank Barclays. Under pressure to find cash to shore up its balance sheet, Barclays had to sell assets.

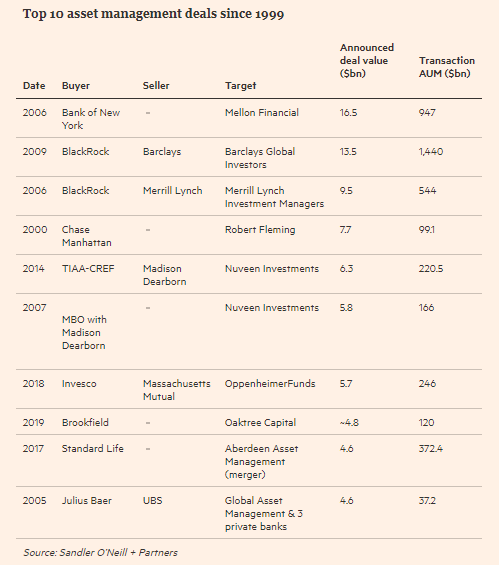

Mr Fink swooped. In March 2009, he began negotiating with Bob Diamond and John Varley, then president and chief executive of Barclays respectively. The $15.2bn cash-and-stock deal they announced in June transformed BlackRock into a financial services colossus and ultimately changed the shape of the global investment industry. Barclays, in turn, managed to avoid a government bailout but it has since been accused of selling its crown jewel.

“We would not have been able to do the BGI purchase if it wasn’t for the financial crisis,” Mr Fink told the Financial Times as BlackRock marks the 10-year anniversary of what some describe as the deal of the decade.

In one stroke the purchase made BlackRock the world’s largest fund manager, with $2.8tn in assets. Ten years on, it oversees $6.5tn and has a market value of more than $74bn.

More importantly, it ensured the company, which was then best known as an active fixed income manager, had a large foothold in part of the asset management industry known as passive investing. BGI, through its iShares brand, was a leader in exchange traded funds, where funds passively track an index of shares instead of making active bets on stock prices of different companies. Since 2009, assets managed in ETFs globally have ballooned from just over $1tn to a record $5.4tn.

Mr Diamond, executive chairman of BGI at the time, said: “What the BGI deal gave BlackRock was a huge franchise in passive indexing and quantitative capabilities.”

Amin Rajan, chief executive of Create-Research, the asset management consultancy, says BGI turned BlackRock into an investment powerhouse.

“The deal vaulted it into an unassailable pole position — for now at least,” he said. “As for the industry, the deal has shown that scale, built on actives and passives under one roof, can shift the centre of gravity away from small and mid-tier [asset] managers. It has also served to promote fees as the north star of the industry via intensified competition.”

But the deal almost did not happen. While Mr Fink was in talks with Barclays, the bank agreed a $4.4bn sale of the iShares unit to CVC Capital Partners, Europe’s leading buyout group.

“We heard rumours about the CVC deal two months before it was announced [in April], and I was talking to Bob Diamond and John Varley throughout that two-month period,” he said.

“I was expressing why they should be focusing on us, why doing the whole transaction would be better for Barclays and better for BGI.”

“Barclays had a ‘go shop’, and they used CVC as a stalking horse, basically, to get other people interested. We were the only firm that was given an exclusive right to buy all of BGI, not just iShares,” said Mr Fink.

Mr Fink kept pushing and by June, BlackRock and BGI were finalising financial terms but at the last minute there was another roadblock. “The deal almost got away from us but that’s another long story. I can’t talk about it, but we did delay the deal by a weekend,” said Mr Fink.

A person close to the situation said Mr Fink spent 48 hours calling in favours as he frantically searched for fresh sources of capital from sovereign wealth funds and hedge funds to finance the deal. Mr Fink had to find new backers because he could not get “full transparency” into where bankers were sourcing capital from, some of which was to come from Middle East investors.

At BGI, staff watched nervously. One senior figure from the time said: “In any M&A situation you would rather be on the acquiring side. There was a certain amount of trepidation. There was a pretty significant cultural difference between the two.”

When BlackRock’s purchase was finally announced, some were incredulous at the size of the deal. Some said Mr Fink spent too much for the low-margin business, while others highlighted the $175m break fee extracted by CVC.

A private poll of institutional investors by Create-Research at the time found that just 28 per cent thought the deal would be a game-changer, with 35 per cent believing the merged company would be an unwieldy giant. “Naysayers have been confounded,” said Mr Rajan.

Mr Fink’s confidence in his purchase was due to several factors.

As a large fixed income manager, BlackRock was in regular talks with many governments as the financial crisis unfolded. “We had a strong belief in early 2009 that governments worldwide were going to do whatever they needed to do to stabilise the world,” he said.

Mr Fink was also no stranger to an acquisition. In 2006, he and Susan Wagner, a former BlackRock vice-chair who now sits on the board, spearheaded the purchase of Merrill Lynch Investment Management, successfully integrating it into the BlackRock business.

“We could not have done BGI without MLIM, and it’s important to put it in that context,” said Mr Fink. “We went from a $360bn bond firm, and then we buy MLIM, and then we became heavily involved in retail, we became heavily involved in equities, and we became a global firm.”

BlackRock also had an edge that helped with its due diligence on BGI as well as its integration.

BGI’s bond division was already a client of Aladdin, BlackRock’s risk management technology platform that is now commonly used in the asset management industry. “We could quickly analyse the whole fixed income component of BGI [as part of due diligence ],” said Mr Fink. “Aladdin gave us confidence that we were going to be able to, more than any other firm, do a big acquisition and integrate on to a common platform.”

“We’re going to have one technology platform as integration is completed. We are going to have one organisation. We’re not going to have silos; we’re going to have one organisation,” Mr Fink recalled.

He believed that merging the technology platforms immediately after the acquisition would expedite the stitching together of the cultures.

Even so, BGI’s integration took three years and was a “hard slog” according to one former employee.

Mr Fink was also convinced that ETFs, a relatively new way of investing that had caught BlackRock’s attention a few years earlier, would become a large component of the investment market.

“We did a strategy piece for internal purposes only and that was on this growing new product call ETF,” said Mr Fink. “The conclusion of that strategy, and this is 2007, was that it would be very difficult for us to get into that business unless we did an acquisition.”

BGI was the acquisition BlackRock had waited for, and its timing was brilliant.

As markets soared on the back of quantitative easing, passive funds delivered strong returns and investors piled in, while many active managers have struggled to outperform. BlackRock now oversees $4.44tn in passively managed (index and iShares ETFs) assets, two-thirds of the New York group’s total, compared with $1.64tn at the end of 2009. At the time of the deal, iShares had $300bn in assets, five years later it crossed $1tn and is now just under $2tn.

For Barclays, the big question is whether it sold the wrong part of its business. A former Barclays banker close to the BGI sale said the bank was required by the UK regulator to raise capital. “We got a phenomenal deal: we bought it for $500m in 1996 and sold it in 2009 for $15.2bn. Whether with hindsight we’d have been better to sell the Barclaycard business is another question,” said the banker.

In recent months Barclays has fought a painful battle with Edward Bramson, an activist investor pushing the bank to shrink its underperforming investment bank.

“Barclays shareholders would have done much better if Barclays had kept BGI and sold off all the rest,” said Cliff Weight, director of ShareSoc, a UK association for small shareholders. He added that although the sale was “probably quite a good deal at a difficult time”, Barclays’ error was selling its large minority stake in BlackRock.

Barclays secured a 19.9 per cent BlackRock stake as part of the BGI deal, which was valued at $13.5bn when announced but rose to $15.2bn when it completed six months after a 62 per cent surge in BlackRock shares.

“Selling that stake in 2012 turned out to be a bad move,” said Mr Weight.

The divergence in fortunes of the respective shareholders has been stark. BlackRock has outperformed Barclays by 470 per cent in common currency terms since the BGI deal. During the decade Barclays shares have dropped more than 40 per cent, while BlackRock is up 160 per cent.

Few rival asset managers have kept pace with BlackRock. Its sheer scale coupled with the popularity of passives has meant BlackRock has dominated the pricing war, putting huge pressure on rivals’ profit margins.

The pressure has led to a wave of industry consolidation, including Aberdeen Asset Management falling into the arms of Standard Life, Janus Capital merging with Henderson and Invesco buying OppenheimerFunds.

Jim McCaughan, former chief executive of Principal Global Investors, the $413bn US fund manager, said the BGI sale was a milestone. “It was the deal of the decade, certainly in asset management and maybe in financial services more broadly.”

Joe Linhares, a former executive at BGI who switched to BlackRock, said: “BlackRock buying BGI and keeping it together was a critical moment . . . for the industry as a whole.” Like other former BGI staff, Mr Linhares no longer works at BlackRock but his peers hold top jobs in the industry.

A former colleague of Mr Linhares said there was a culture clash. “Culture is a factor in why so few BGI people stuck around. BlackRock has become a juggernaut but it did a good job at taking BGI and making it the biggest.”

Another senior figure in the investment industry who has worked at both Barclays and BlackRock said: “Larry Fink bet his entire firm on the BGI acquisition. And it took tremendous courage. Not everyone was aligned. It was really Larry seeing the trend and making a call on a product that he thought was going to be important. It was hugely important for BlackRock.”

0 comments:

Publicar un comentario