Goldman: Machines Are Taking Over Markets

By Alex Kimani

“Liquidity is the new leverage”: That was the ominous warning fired by Goldman Sachs’ head of Global Credit Strategy, Charles Himmelberg, admonishing traders about the dangers of the ongoing algorithmic transformation in the markets, including the toxic combination of Quant Funds and High-Frequency Trading and how they put the bond and equities markets at high risk of a systemic event.

What he meant was this: The heavy use of leverage has historically been responsible for most market crashes, but right now it's liquidity—or, more specifically, the lack of it--that's likely to be their undoing.

But how does that work?

HFT traders and quant funds are likely to withdraw liquidity from the market during periods of market stress when, ironically, it's needed the most.

As machines continue taking over trading roles in the market, the inability of human market liquidity providers to process complex information as quickly as their computer counterparts might lead to large drops in liquidity that could precipitate a market crash.

Machines Take Over the Markets

This was not the first time that the Wall Street analyst has chimed in heavily on the subject. In fact, he’s done so repeatedly since the February 5 market crash.

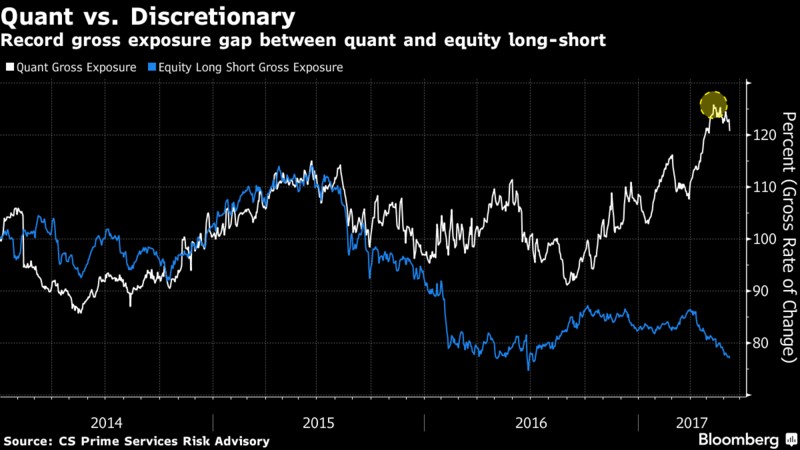

And just as well, because robots have truly taken over equities trading.

JPMorgan estimates that passive and quantitative trading now account for 60 percent of all equities trading, double from a decade ago. Meanwhile, human discretionary investing accounts for a mere 10 percent of trading volume.

Quantitative trading is a complex type of trade encompassing high-frequency trading, algorithmic trading and statistical arbitrage using a combination of sophisticated statistical models, fiendish mathematical models and computer modeling to automate the process of monitoring markets and making trades entirely using robots.

(Click to enlarge)

Source: Bloomberg

Robots Wreak Havoc

This is not mere babbling by an armchair analyst but serious stuff by a non-tinfoil hat-wearing Goldmanite.

There's ample evidence that HFT and QT are to blame for some of the most memorable flash crashes. The most recent flash crash of February 5 was pinned on robots and the role of high-risk volatility instruments which Credit Suisse, the issuer, thankfully banned. Others include the Peet's Coffee and Tea incident of 2012, the Knight Capital sell-off and the 2010 flash crash.

Goldman offers compelling validation. The image below shows how HFTs behave around major world news events. The right chart shows how HFTs' participation rate drops from 50 percent about 10 minutes before the announcement to 33 percent at the time of release. The chart on the left shows how overall market depth declines sharply around the time of news release.

(Click to enlarge)

Source: Zero Hedge

This HFT reluctance to provide market liquidity is what Goldman is talking about. HFTs tend to pull back whenever they realize that fundamental information entering the market is likely to give human traders an advantage.

Himmelberg offers two key pieces of advice to traders to avoid finding themselves on the wrong side of these HFT trades:

• Avoid being lulled into a sense of complacency even during times of macroeconomic stability.

• Carefully consider the quality of trading liquidity even for the most-heavily traded markets.

Consider 'vol of vol' when hedging market risk and don't be fooled by fat tails.

And that puts paid the common belief that there's copious liquidity parked across all asset clases.

What he meant was this: The heavy use of leverage has historically been responsible for most market crashes, but right now it's liquidity—or, more specifically, the lack of it--that's likely to be their undoing.

But how does that work?

HFT traders and quant funds are likely to withdraw liquidity from the market during periods of market stress when, ironically, it's needed the most.

As machines continue taking over trading roles in the market, the inability of human market liquidity providers to process complex information as quickly as their computer counterparts might lead to large drops in liquidity that could precipitate a market crash.

Machines Take Over the Markets

This was not the first time that the Wall Street analyst has chimed in heavily on the subject. In fact, he’s done so repeatedly since the February 5 market crash.

And just as well, because robots have truly taken over equities trading.

JPMorgan estimates that passive and quantitative trading now account for 60 percent of all equities trading, double from a decade ago. Meanwhile, human discretionary investing accounts for a mere 10 percent of trading volume.

Quantitative trading is a complex type of trade encompassing high-frequency trading, algorithmic trading and statistical arbitrage using a combination of sophisticated statistical models, fiendish mathematical models and computer modeling to automate the process of monitoring markets and making trades entirely using robots.

(Click to enlarge)

Source: Bloomberg

Robots Wreak Havoc

This is not mere babbling by an armchair analyst but serious stuff by a non-tinfoil hat-wearing Goldmanite.

There's ample evidence that HFT and QT are to blame for some of the most memorable flash crashes. The most recent flash crash of February 5 was pinned on robots and the role of high-risk volatility instruments which Credit Suisse, the issuer, thankfully banned. Others include the Peet's Coffee and Tea incident of 2012, the Knight Capital sell-off and the 2010 flash crash.

Goldman offers compelling validation. The image below shows how HFTs behave around major world news events. The right chart shows how HFTs' participation rate drops from 50 percent about 10 minutes before the announcement to 33 percent at the time of release. The chart on the left shows how overall market depth declines sharply around the time of news release.

(Click to enlarge)

Source: Zero Hedge

This HFT reluctance to provide market liquidity is what Goldman is talking about. HFTs tend to pull back whenever they realize that fundamental information entering the market is likely to give human traders an advantage.

Himmelberg offers two key pieces of advice to traders to avoid finding themselves on the wrong side of these HFT trades:

• Avoid being lulled into a sense of complacency even during times of macroeconomic stability.

• Carefully consider the quality of trading liquidity even for the most-heavily traded markets.

Consider 'vol of vol' when hedging market risk and don't be fooled by fat tails.

And that puts paid the common belief that there's copious liquidity parked across all asset clases.

0 comments:

Publicar un comentario