Buttonwood

The markets’ apparent calm over Brexit is deceptive

Investors’ hopes for the best may yet be dashed

FOR all the sound and fury of the Brexit negotiations, it has seemed at times as if the financial markets have been barely affected. But as with the swans that glide on the Thames, a serene surface conceals some frantic paddling underneath.

The pound is the most reliable indicator of the Brexit mood. A rule of thumb is that, if the headlines point to a “hard” Brexit (creating trade barriers with the EU), sterling will fall; signs of a “soft” Brexit (something that is close to the current relationship) will cause it to rise.

But some feedback processes are at work. The big fall in the pound in the immediate aftermath of the referendum has led to a gradual rise in imported inflation. The annual inflation rate hit 3.1% in November, requiring Mark Carney, governor of the Bank of England, to write to Philip Hammond, the chancellor, to explain why the target (of 2%) had been missed. The bank has already raised interest rates once. More rises may follow, and expectation of such rises supports the pound.

The need for monetary tightening is not simply a result of higher import costs, which might prove temporary. More worryingly, the Bank thinks that the trend rate of growth of the British economy has fallen (a view it shares with the Office for Budget Responsibility, the government’s forecasting arm). In part, this is because Britain faces a more difficult future after Brexit; in part it is a recognition that the economy’s productivity was dented by the 2008 financial crisis.

If the trend growth rate falls, that brings forward the time when a tighter labour market begins to be translated into faster wage increases and into broader inflation. In turn, this means the central bank may have to act more quickly to push up interest rates.

When it comes to the bond and equity markets, the Brexit effect has to be seen in light of global trends: historically low bond yields and a widespread stockmarket boom. Ten-year gilt yields fell below 1% in the aftermath of the referendum, and are still below their level at the end of May 2016. But bond yields can drop for two reasons. The optimistic one is that the bonds look more attractive to investors, so the price rises and the yield falls. The pessimistic one is that investors become less sanguine about the economic outlook and shift into bonds because they are less risky.

It is tempting to assume the pessimists are wrong; after all, the stockmarket is up and it would suffer if economic growth were thought to be at risk. But the analysis is made more complicated by the presence of a lot of multinationals in the FTSE 100 index. Their prospects are not wholly reliant on the British economy. And their overseas earnings are worth more, in sterling terms, after the pound’s fall.

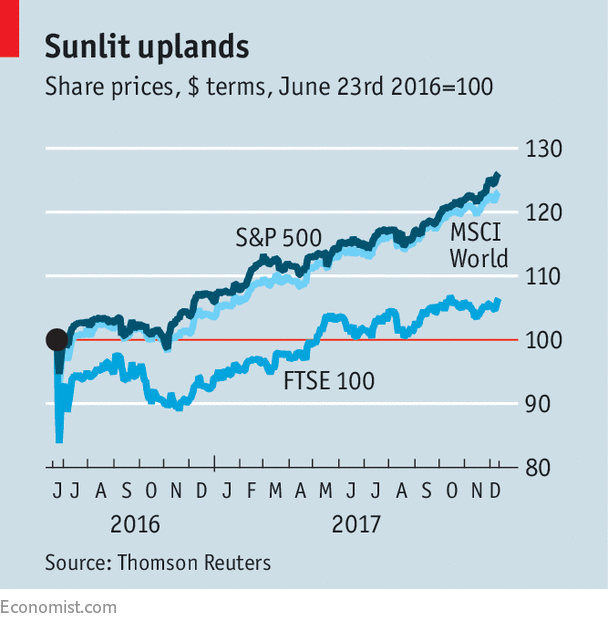

In relative terms, British equities have not been performing well. Measured in dollar terms, the FTSE 100 has risen by just 6% since the referendum, compared with gains of 23% in the MSCI World index and 26% in the S&P 500, America’s main benchmark (see chart). In both dollar and sterling terms, the FTSE 100 index has been one of the worst-performing developed markets in 2017. A survey of global fund managers by Bank of America Merrill Lynch in November found that a net 37% have a lower-than-normal weighting in British equities.

Nevertheless, there has been no dramatic stockmarket sell-off and the pound is above its post-referendum lows. Investors have tended to ignore the nationalist rhetoric and assume that rationality will triumph in the end. The trading links between Britain and the EU are too important to jeopardise. Furthermore, the process has become elongated. Since a two-year transition deal seems likely, the crunch point for trade may not occur until 2021. As a result, investors choosing how to allocate assets in 2018 may decide not to worry about Brexit too much.

One school of thought is that the process will turn into BINO (Brexit In Name Only) with Britain staying in the single market—in effect, remaining in the EU but without having any influence over the rule-making process. That is the logical consequence of the deal that has been reached over the Irish border; if Northern Ireland stays aligned both with the regulations prevailing in the Irish republic and in the rest of Britain, the implication is that Britain stays in the single market.

But that also leaves scope for disappointment among investors later, when the British government tries to reconcile the various contradictory promises it has made. That is another thing with swans; they look beautiful, but they are bad-tempered birds which can give a nasty whack with their wings.

0 comments:

Publicar un comentario