Volatility Like It's The 1930s

- Economists have been noting similarities between this year and 2011 for several months now. But another year might be a better comparison: 1937.

- 2011 says stocks are going to rally up, but 1937 says prepare for the downturn. Which should we believe?

- December holiday rally may have been an early Christmas present given to investors in October. The signs of oddity and abnormality are all around.

Historical spreads may better explain current unusual times if we consider a series of events that began in the late 1920s that correlate to what's been happening in the market since the financial crisis:

1) Debt limits have reached the bubble top, causing the economy and markets to peak (1929 and 2007).

2) Interest rates hit zero amid "depression" (1931 and 2008).

3) Money printing starts, kicking off a "beautiful deleveraging" (1933 and 2009).

4) The stock market and "risky assets" rally (1933-1936 and 2009-2014).

5) The economy improves during a cyclical recovery (1933-1936 and 2009-2014).

6) The central bank tightens, resulting in a "self-reinforcing downturn" (1937 and 2015?).

Let's say 1937 is happening again, let's take a look at current "abnormal" economic conditions that explain some investing parallels:

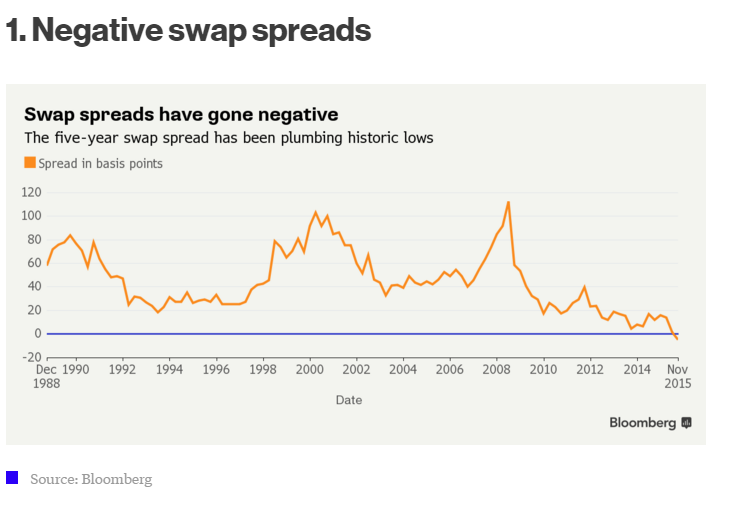

Swaps

(click to enlarge)

What does a market where pricing mechanisms have been playing musical chairs by central bankers look like? Swap spreads may provide some clues. Interest rates as expressed by five-year interest rate swaps have dipped below negative, an abortion that likely wasn't in the text books to which Keen or other economists are familiar with.

The odd dichotomy extends to the interest rate repo market, where an unusual spread is showing signs of a fracturing repo rate market. This is followed by corporate bond inventories by large dealer banks gone negative for the first time since the Fed began collecting such data.

Add to this synthetic derivatives are trading more liquid than cash credit amid a market environment where correlations are breaking down.

Volatility

(click to enlarge)

With rates near zero in an expanding economy, the Fed doesn't have much room to maneuver.

Taking a closer look at the end of a super cycle, otherwise known as long-term debt cycles, central banks are pushing on a string and their ability to stimulate the economy is more likely to fail than succeed. Such tightening ominously drew mental corollaries to 1937, when debt limits reached a bubble top, interest rates hit zero, and money printing proved a secular stagflation during a well-executed deleveraging.

It happened in 1937, and there are significant comparisons to the 2008 crash and today to point of historical equivalents. This raises an important question: will there ever be a good time to tighten?

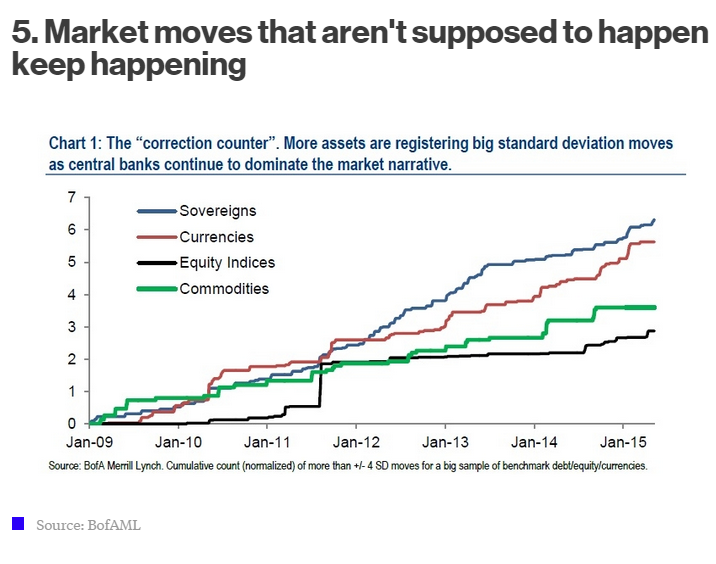

Markets Moves: Say What?

(click to enlarge)

Conclusión

If you aren't convinced yet, then consider these four differences when comparing this and four years ago:

1. Earnings are declining, while expanded in 2011.

2. The 12% correction stocks witnessed this year was also less than the 19% plunge equities experienced four years ago.

3. At the lows, this year's price-to-earnings multiple was 45% higher than it was at its trough in 2011.

4. We are further along in the business cycle now than we were four years ago.

The lesson is that investors need to understand patience and volatility. To take advantage of future opportunities, consider keeping a small portion of your overall portfolio in cash. I choose 10%, though your willingness to patiently wait in low-yielding cash may justify a different percentage.

Make a plan ahead of time for how to deploy the cash if stocks fall, so that you won't get caught up in the heat of the moment.

Mine is to put one-third of my cash hoard into my usual array of stock funds if prices fall 20% from a recent high, another third if they fall 30%, and the remainder if stocks fall 50% - which happens a few times a century, judging from history.

Another option is to invest in an actively managed mutual fund that keeps a significant amount of its assets in cash. I suggest AMG Yacktman Focused Fund S (MUTF:YAFFX) or Tweedy, Browne Global Value Fund (MUTF:TBGVX). Such funds can take advantage when opportunity strikes and fully invested competitors are caught flat-footed.

However, during the past recession, prominent bankers, businessmen, etc. were all wrong in most of their predictions.

My conclusion: use your own judgment and do your own thinking.

0 comments:

Publicar un comentario