Global economy survives the China and commodity shocks – so far

Gavyn Davies

Summary

Recent turbulence in global financial markets has been widely attributed to fears that a hard landing in China could lead to a sharp slowdown in activity growth in the rest of the world, including in the US and other developed economies. With global markets likely to be very sensitive to small changes in activity data in the months ahead, activity “nowcasts” should be a particularly useful tool for investors.

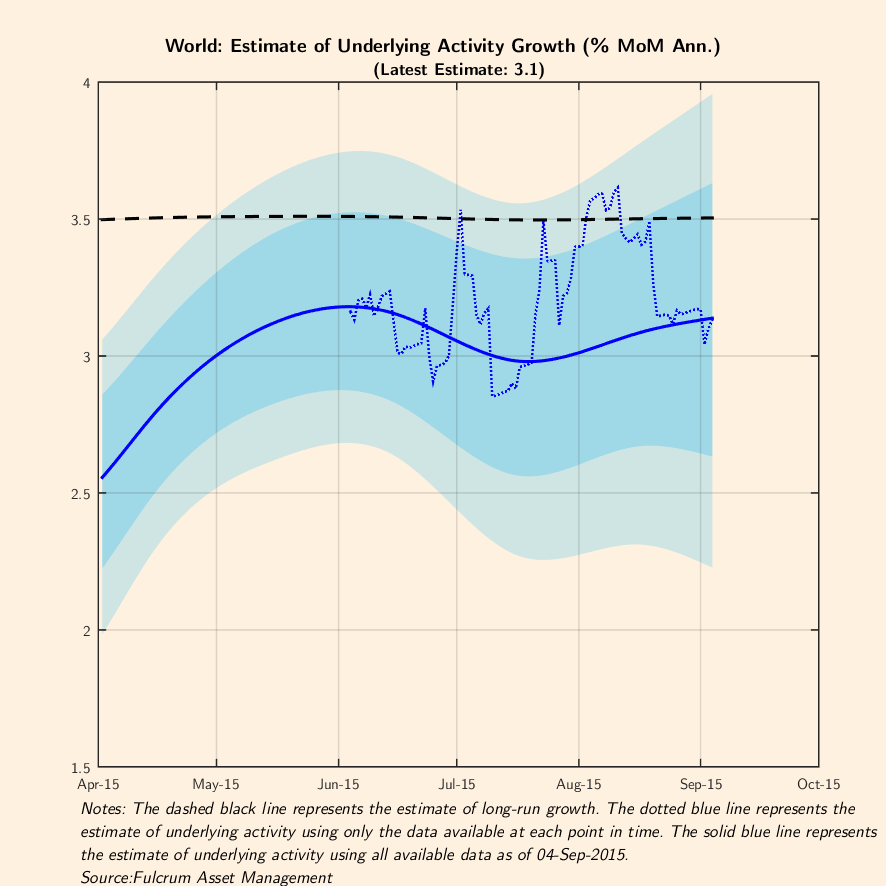

In this month’s global growth report card, we find little evidence that the feared global hard landing is actually happening, so far at least. According to the Fulcrum “nowcast” models, the global activity growth rate has remained virtually unchanged at around 3.1 per cent this month. This is around 0.4 per cent below the model’s estimate of the long run trend, and is similar to the growth rate recorded since spring 2015.

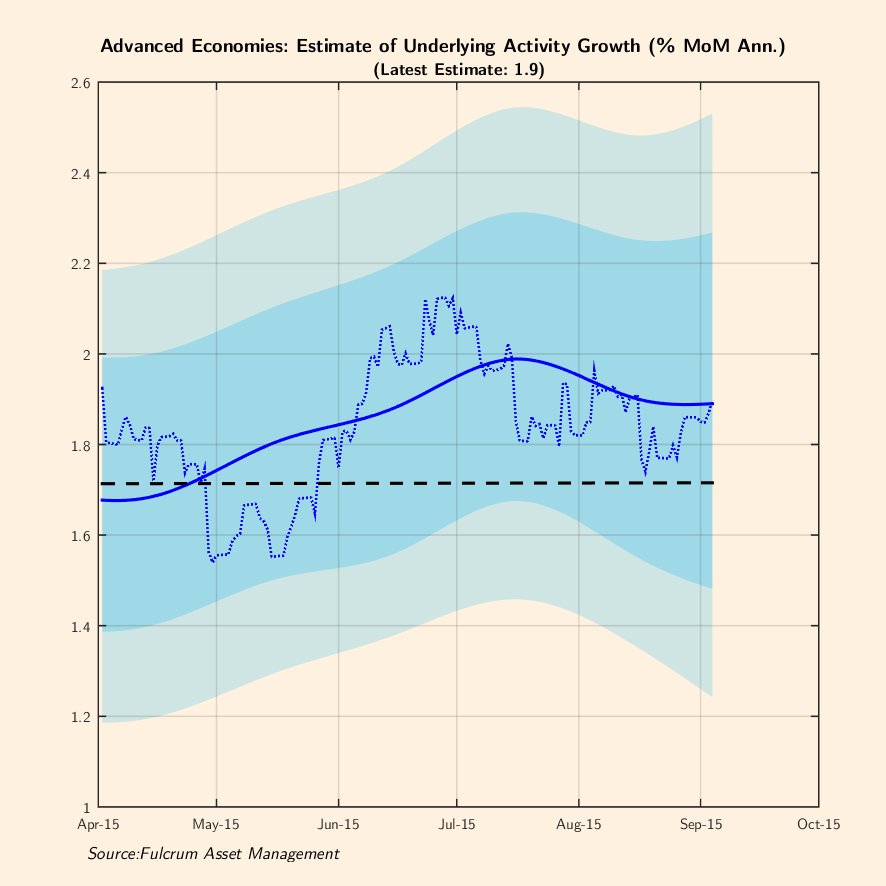

The advanced economies have continued to grow steadily, with the latest estimate of 1.9 per cent being slightly above trend (1.7 per cent), and also a little above the growth rates recorded in the spring.

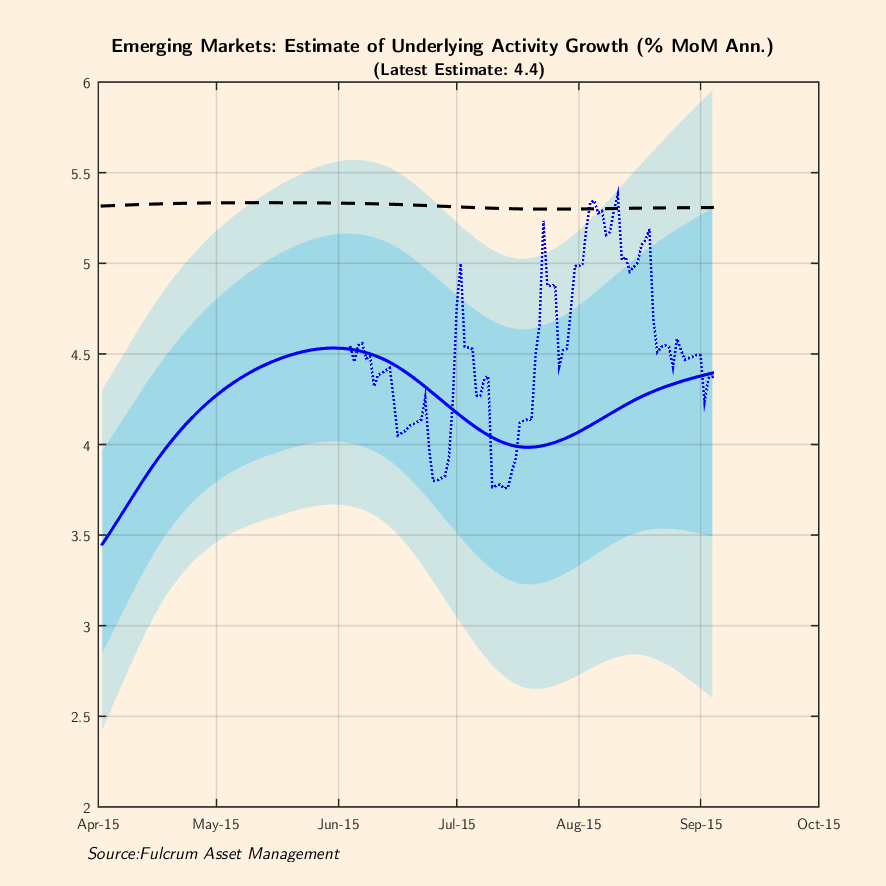

On the other hand, the emerging market economies (EMs) continue to struggle, and are currently growing at 4.4 per cent, which is almost a full percentage point below trend.

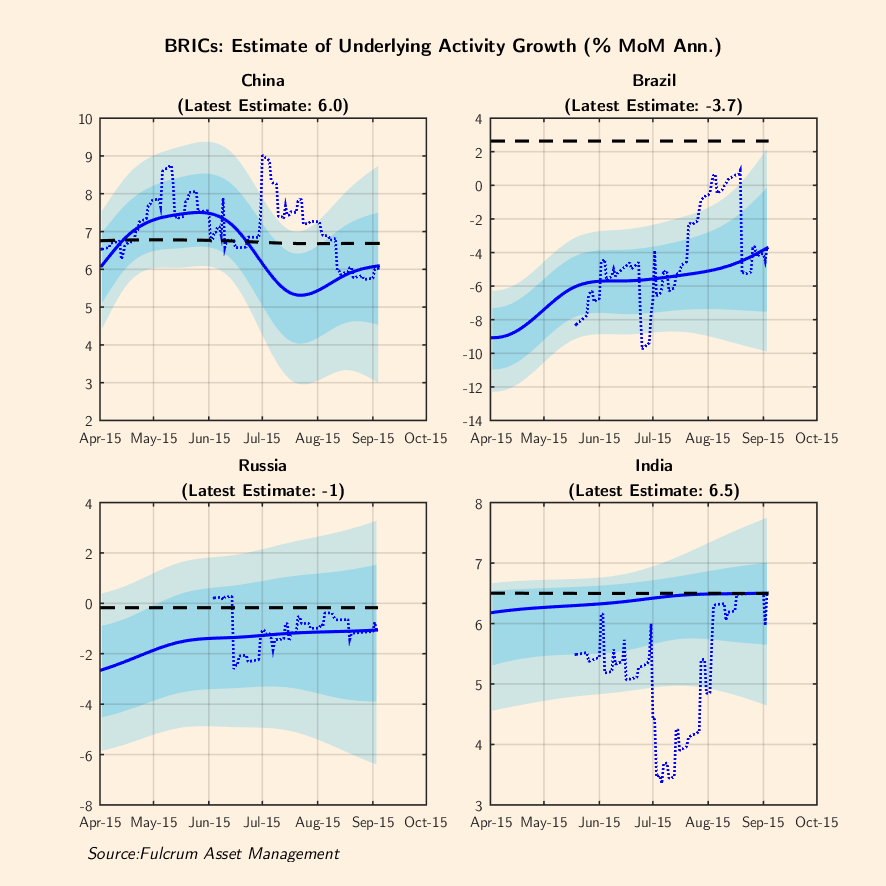

Commodity driven economies have, of course, been particularly badly hit. Both Brazil and Russia are still mired in deep recessions, with little sign of improvement, and Chinese activity has dipped again in August, after apparently rebounding in the aftermath of the piecemeal policy easing that was announced in April.

There is no sign of much generalised improvement in activity in other emerging economies in Asia, where trade flows continue to slow sharply.

However, it is important to note that there are some isolated bright spots, including India and Korea, that have prevented a nose-dive in overall EM activity this month. Furthermore, while China has slowed, it has only done so to the extent that has happened several times in the past couple of years. The latest picture is therefore one of below trend, but not collapsing, growth rates in the emerging world. Whether the developed economies will catch the EM disease with a time lag remains to be seen but, since they should gain from the commodity shock, this is far from inevitable.

China experiences a bumpy slowdown

Market commentary in August has focused almost exclusively on the supposed “downward shock” to Chinese activity, but there is still great uncertainty surrounding the extent of this slowdown. According to our “nowcast” models, activity growth has slowed to 6.0 per cent, thus eliminating the short term bounce to around 7.5 per cent that followed the easing in fiscal and monetary policy announced in April.

Part of this renewed slowdown is probably the result of temporary factory closures to reduce pollution ahead of major events. Furthermore, there has been another round of monetary and pseudo-fiscal easing announced in August, and this is likely to be seen in the data shortly. A rebound in activity data to around 7 per cent in 2015 Q4 therefore seems probable.

Why, then, has this latest slowdown triggered such pessimism about the Chinese economy?

There are several reasons: scepticism abounds about the accuracy of Chinese economic data (see last month’s report); Chinese commodity-related sectors have slowed much more than the rest of the economy; the tail risks identified by the activity models (shown by the blue zones in the graphs) have increased; and policy announcements have been confused and contradictory, undermining market confidence in the ability of the authorities to control the deleveraging of the economy. As Martin Wolf has argued, a “discontinuity” in China is now clearly conceivable, but the data suggest that it has not happened yet.

Commodity shock hits other emerging economies

The rest of the emerging world has, of course, been hit by weakness in export sales to China, but a more important factor has been the impact of the commodity shock, which stems from over supply by the commodity producers as well as from the China demand factor. Among the largest emerging economies, Brazil and Russia have been particularly impacted by this shock, but its effects are widespread throughout Africa, the Middle East and Latin America.

Reliable “nowcasts” are available for only a handful of EMs, largely because of lack of available economic data. Nevertheless, they cover much of the emerging world’s GDP. Overall, the latest estimates show EM activity growth at 4.4 per cent, little changed from recent months.

The decline in China has been offset by a large rebound in Korean activity, as the recent fears about a MERS epidemic have faded.

Downside risks in the EMs clearly remain severe. Capital outflows are leading to much tighter domestic monetary conditions in many economies, and political risks are concerning in countries like Brazil and Turkey. Worries about the ability of many economies to service their corporate dollar debt are increasing, and would do so further if the Federal Reserve raises interest rates later this month.

DMs unaffected by the weakness in EMs

Now for the slightly better news: the developed market economies (DMs) seem to have been largely immune to the EM slowdown, up to and including the business survey data that have been published very recently. The DMs as a bloc have continued to record activity growth of about 1.9 per cent, which is slightly better than it was in the spring.

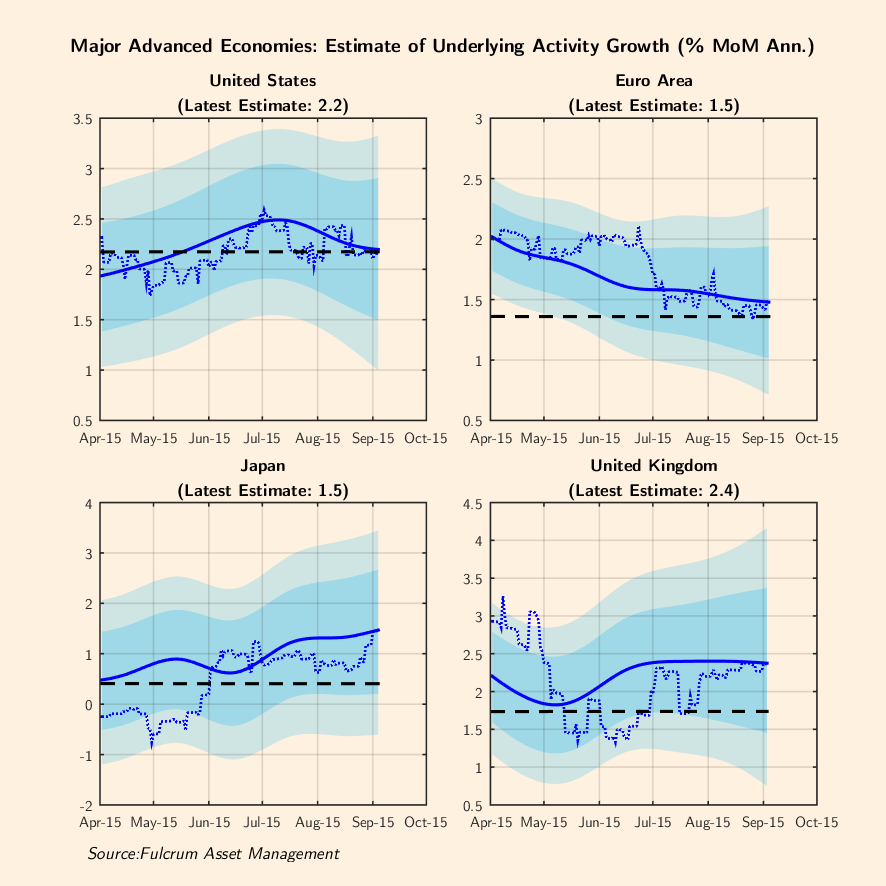

The United States activity is growing at 2.2 per cent, close to the mid point of its recent range, while the eurozone is recording growth at 1.5 per cent, which is slightly lower than the growth rate observed during much of the summer months. Japanese activity growth has risen slightly to 1.4 per cent, while the UK has remain in healthy territory at 2.4 per cent.

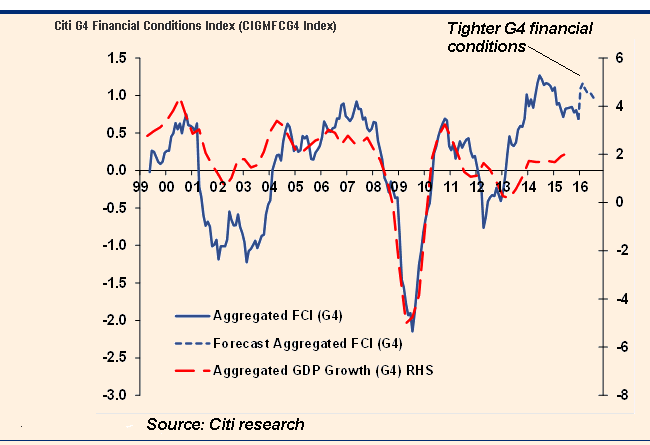

It is not surprising that the China/commodity shock would have a less contractionary effect on the DMs than the EMs, because most advanced economies are commodity importers. However, there has also been a tightening in monetary conditions in the DMs as a result of recent turbulence in global financial markets, which has led to a rise in credit spreads, in real exchange rates and a fall in DM equities.

This monetary tightening represents an additional channel in which economic and financial trouble in the EMs can potentially lead to a slowdown in activity in the US and the eurozone. It is something that the Fed should be very seriously pondering before adding fuel to the flames by raising US interest rates at the September FOMC meeting.

———————————————————————————————————-

Footnotes

The full set of regular graphs and tables that are included with this report card each month are attached here.

The previous monthly report cards for March, April, May, June, July and August 2015 are also attached for convenience.

0 comments:

Publicar un comentario