Oct. 22, 2014 3:53 AM ET

Summary

- The S&P 500 has rallied 5.7% in 4 days, an impressive performance.

- We believe debt market dynamics and central bank expectations have fueled the move.

- Next week's FOMC statement is likely to produce significant volatility.

Impressive Performance for US Equity Markets

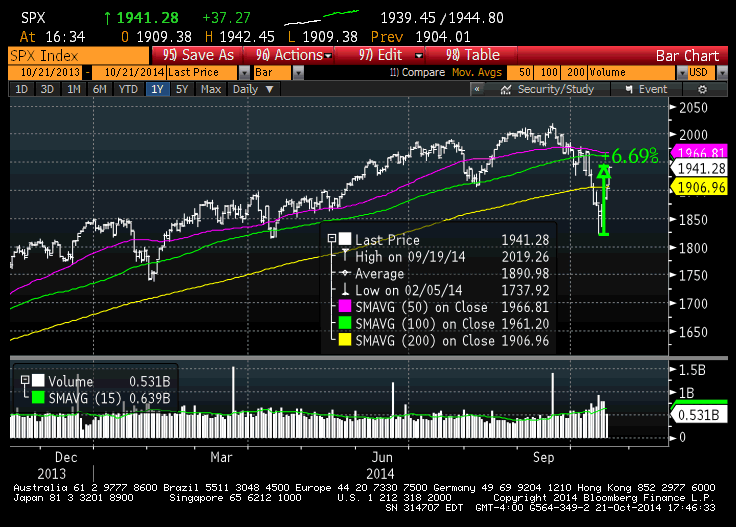

US stocks had a fourth straight impressive day today, with major averages rising nearly 2% or more. After plunging last week, the S&P 500 (NYSEARCA:SPY) is less than 4% off of the all-time high of 2019. The chart below shows the current technical posture.

(click to enlarge)

As can be seen, the S&P 500 burst through the 200 day moving average today with impressive force. The next area of technical resistance should be located at the 1960-1966 area, corresponding to the 50 and 100 day moving averages. We believe it is important to examine the underpinnings of the powerful four day rally in order to understand what might lie in store.

Fixed-Income Markets Are Telegraphing Fed Policy Change

We believe that a great deal of the recent rally can be explained using changes in expectation regarding the future path of the Fed Funds interest rate. The following chart shows the Eurodollar curve on October 1st in green and the same curve today in brown.

(click to enlarge)

As a quick primer, Eurodollar futures have nothing to do with the euro or dollar as currencies.

Eurodollar futures are ways for hedgers and speculators to bet on the future Fed Funds rate.

Subtracting the Eurodollar futures contract value from 100 gives one the contract's current expectation of future Federal Reserve-set interest rates. As an example, if the December 2016 Eurodollar futures are trading at 98.50, it means that the traders of that contract expect that the Fed Funds rate will be at 1.50% in December 2016.

At the beginning of this month, December 2016 Eurodollar futures were trading at 97.80, implying a 2.2% Fed Funds rate at the end of 2016. Due to recent market volatility, traders have now bid up this contract to 97.38, a full 58 basis points higher. Similar moves occurred in all maturities of the Eurodollar curve, meaning investors have unanimously pushed out their expectations for how fast Janet Yellen and the Fed will raise interest rates.

Perhaps on its own, this change in expectations would be unremarkable, and actually understandable given the recent volatility expansion. However, due to the Fed's mandate to increase communication started a few years back, we know that we have a massive disparity developing in investors' expectations versus the Federal Reserve's.

The following chart is from the Federal Reserve's September publishing of their Staff Economic Projections. These are a direct depiction of FOMC members' views regarding the Fed Funds rate that is published every 3 months. The following chart shows how many members expect in which year the Fed will begin raising interest rates.

(click to enlarge)

As can be seen, the vast majority (14/17) members expected that the Fed Funds rate would be raised in 2015. These opinions were culled during the FOMC meeting ended on September 17th.

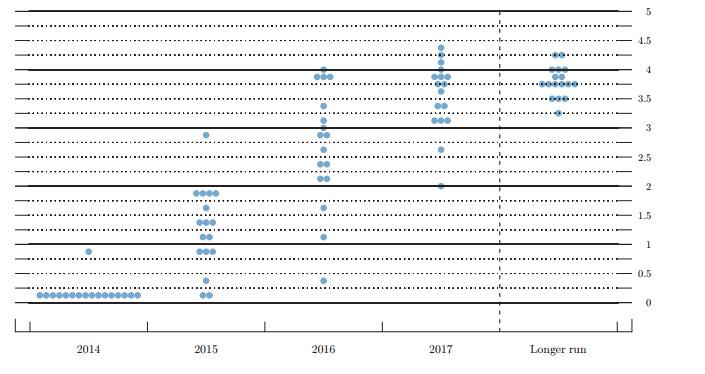

The following chart shows a more detailed view of FOMC participants' interest rate views. The dots correspond to members' views regarding rates.

(click to enlarge)

As can be seen, the majority of the FOMC expect rates to be 0.75% or higher at the end of 2015, and 2% or significantly higher by the end of 2016.

Since this publishing of the Staff Economic Projections, worldwide equity markets have been roiled by Ebola, global growth concerns, and a myriad of other given reasons for increased volatility.

Investors have been so spooked by the gyrations that they now believe the Federal Reserve's posture has fundamentally changed towards a much more accommodative stance.

At this point, the market's expectation of the Fed Funds rate at the end of 2015 is 0.75%, whereas the Fed's median end of 2015 expectation is 1.25%. The December Eurodollar expectations are even more out of line, with the market's expectation being 1.62% Fed Funds rate at the end of 2016 versus the Staff Economic Projection median of 2.75%.

Essentially, investors are betting a (slightly less than) 10% correction in the S&P 500 is enough to get the Fed to completely abandon their projections and push interest increases out in a major way. Given recently dovish statements such as Bullard's implication that the Fed could perhaps delay the end of quantitative easing and the well-chronicled dovish tendencies of Janet Yellen, it is easy to see why the market expects this. However, the reflexive nature of the market's change in expectations is bound to perplex the Fed in next week's meeting.

Federal Reserve in Very Awkward Situation Given Market Rally

At the time that Bullard suggested last week that the Fed could have a major departure from stated policy and continue QE rather than end it next week, the S&P 500 was trading at 6 month lows and threatening to plunge even more. Given the violent pullback of -9.84% in just under a month, Fed officials were understandably concerned about market contagion, especially considering highly negative developments in European and the Hong Kong market.

However, the powerful rally of the last few days puts the Fed in an extremely awkward situation. At this point, the S&P 500 is less than 4% off the all-time high, hardly a concerning plunge when ignoring the volatility that occurred in the meantime. Going into next week's meeting, the Fed must be relieved that the market has corrected itself and found footing, but on the other hand they too can see the market's drastic change in interest rate expectations.

The Fed's conundrum is, do we make accommodative interest rate language changes to the FOMC statement and risk fueling even more speculative behavior, or do we risk rocking the boat and sending financial markets reeling again by making no change and reiterating our data-driven stance, which would be viewed as hawkish? The decision faced by the FOMC will only get more convoluted if and when financial markets rally over the coming week.

Conclusions

We believe the stock market rally has been fueled by investors' expectations for lower future interest rates and a highly accommodative Federal Reserve stance. However, it is highly probable that both of these conditions are not mutually sustainable.

Our view that equity markets are rallying simply due to decreased interest rate expectations is highly worrisome. Given the stage of the cycle the Fed has painted us in, investors' expectations could snap back considerably if the Fed does not continue to disseminate accommodative chatter.

We believe that a rallying stock market will only embolden the Fed to begin policy normalization in the path they envisioned and published just over a month ago. This would cause interest rate expectations to reset dramatically, triggering a severe correction in bonds and Eurodollar futures, which could also trigger a renewed correction in equities if investors are disappointed.

On the other hand, we believe the stabilization of fixed-income products at current prices could only be justified by further volatility and financial market turmoil, which would be accompanied by lower equity prices.

What this means for investors is that a simultaneous move upwards in the bond and stock market from current levels is unlikely. Either the stock market, bond market, or both will fall from current levels to justify the other.

Trade Recommendation

Given the severe retraction in the VIX and implied volatility across the board, investors could use put options to effectuate a position given this thesis.

Traders could purchase the November 22nd 117 put on the TLT ETF (NYSEARCA:TLT) to bet on rising interest rates for $0.60 while simultaneously purchasing the November 22nd 190 put on SPY for $2.02. Given that volatility of bonds will be much more subdued than equities, traders could purchase this combination of options in a 2.5:1 ratio, meaning 2.5 put options on TLT for each 1 on SPY.

For longer-term minded investors considering whether the current rally in the S&P 500 should be bought or sold, we would advise a position on the sidelines. While the rally of the past few days has been impressive, we note that such wild volatility is rarely the sign of a healthy market. While we fully acknowledge a move back to the all-time highs is possible, it is no better than an even money trade at this point. We would advise longer-term investors to be defensive here and reevaluate in light of the Fed's decision and subsequent market reaction next week.

0 comments:

Publicar un comentario