The ECB confronts the zero lower bound

November 3, 2013 2:51 pm

by Gavyn Davies

The startling success of this action has tended to shift attention away from more mundane matters, such as the overall stance of monetary conditions for the euro area as a whole. But the recent decline in inflation has raised serious questions about whether the monetary stance is anywhere near appropriate for an economy in such a depressed state.

This is problematic for the ECB, since it has already fired almost all of the conventional monetary ammunition available to it. And it has never followed the example of other major central banks in considering that quantitative easing is needed to ease policy at the zero lower bound for interest rates. It may soon have to face up to this issue.

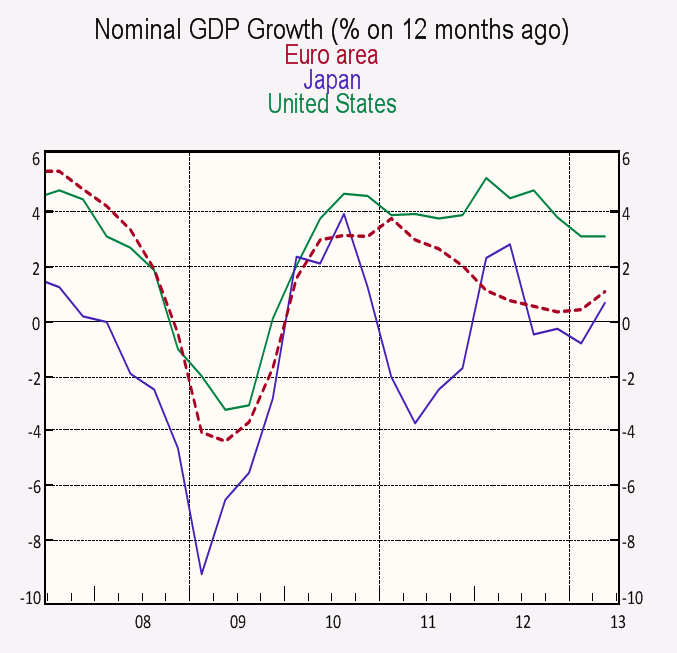

Many of the economic symptoms displayed by the euro area in recent months suggest that monetary conditions have remained overly tight, despite a reduction in policy rates in May, and Mr Draghi’s limited use of forward guidance in July. Nominal GDP is rising at only 1 per cent per annum, which is nearer the Japanese than the American rate. Unemployment has been rising along with the exchange rate, and the central bank’s balance sheet has been declining rapidly. Excess liquidity held by the banking sector at the ECB has fallen by over E600 billion in about a year. Broad monetary growth has been subdued, with credit to the corporate sector continuing to decline at an annual rate of -5 per cent.

Most central banks would take these symptoms as proof that monetary policy should be eased, and eased significantly. But the ECB has always ploughed its own furrow. Although the Governing Council may well be ready to indicate on Thursday that a 25 basis points reduction in policy rates is in the offing, there is no sign that they think that a more drastic re-appraisal of their monetary stance is appropriate. If the central bank is in the wrong ball-park for monetary conditions, it seems to have every intention of staying there.

The ECB’s Policy Reaction Function

This conclusion follows from the monetary policy reaction functions which they have tended to use in the past. When Mr Draghi promised to keep interest rates “at present or lower levels for an extended period of time”, he suggested that the precise length of time could be gauged by extracting

“a reaction function and, from there, estimate what would be a reasonable extended period of time”.

In other words, the ECB is expecting to follow its normal policy rule, which is used for translating inflation and unemployment (or the output gap) into the appropriate level of interest rates.

A problem with Mr Draghi’s guidance, however, is that there are many such reaction functions that can be estimated, with very different implications for the appropriate level of short rates. Furthermore, the size of the output gap is very uncertain, given the extent of the post-2008 decline in real GDP relative to its previous trends.

By plugging in a relatively large estimate for the output gap, it is certainly possible to derive reaction functions which suggest that ECB interest rate policy is several hundred basis points too high. David Mackie at J.P. Morgan published a paper last week with just such an estimate. Given the constraint of the zero lower bound, this suggests that they should be contemplating a more dramatic shift in strategy, such as area-wide quantitative easing, if only to get the exchange rate down.

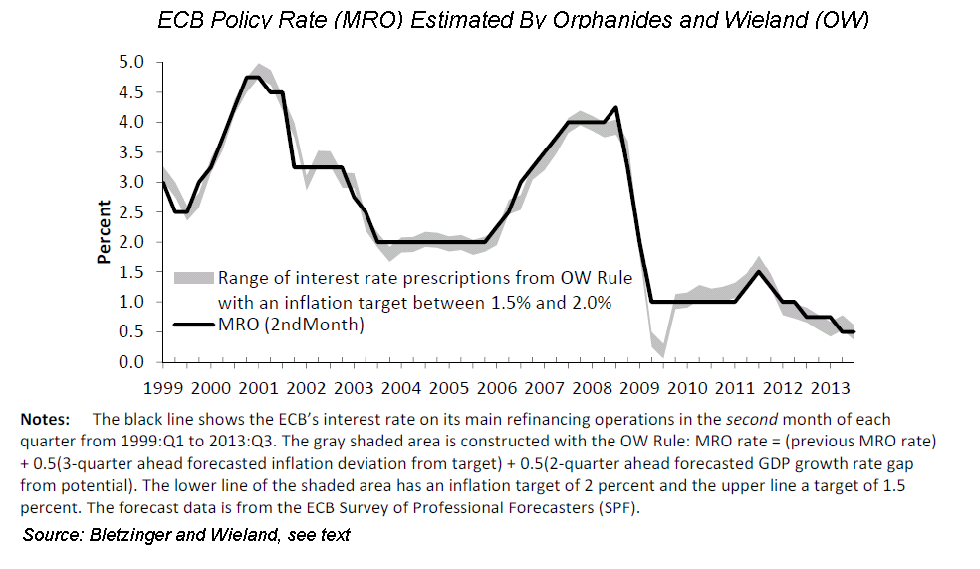

There is no evidence, however, that the ECB thinks that this is necessary or appropriate. One reaction function that is close to the one that the ECB itself probably uses is outlined in this recent paper by Tilman Bletzinger and Volker Wieland at the Institute for Monetary and Financial Stability in Frankfurt. It builds on work done with Athanasios Orphanides, who recently stepped down from the Governing Council.

Their estimate of the reaction function side-steps the difficulty of estimating the size of the output gap by relating changes in policy rates (not levels) to changes in inflation and in GDP growth, relative to potential growth:

As the graph shows, this rule has explained ECB policy changes very accurately in the past, with the exception of a short period after the 2008 crash when the rule suggested much larger policy changes were desirable than those the ECB actually pursued. In recent months, this rule has suggested that policy rates should be edging downwards, but not any more rapidly than has actually occurred.

Menu of Policy Options

The fall in inflation in October, which encompassed both the headline and the core rates, was a fairly sizeable shock. This is likely to lead the ECB to reduce its inflation forecasts for 2014, published in December, by as much as 0.3 percentage points, from 1.3 percent to about 1.0-1.1 percent.

Plugging this into the Orphanides/Wieland reaction function suggests that the policy rate should be reduced by about 0.15 per cent more than previously, a smaller reduction than the 0.25 per cent cut in the refi rate that the market now expects to see in the next month or two.

In addition to this cut in rates, Governing Council members have frequently suggested that other conventional measures are still available to them, such as announcing a new LTRO, or a decision not to sterilize all of the government bonds that have been purchased in earlier support operations. (See Joerg Asmussen here.)

All of these options have one thing in common: they would represent relatively limited relaxations in monetary conditions at a time when something more dramatic might become necessary to pull the euro area away from the risk of deflation. The ECB’s preferred reaction function will only reveal this very slowly, if at all, as inflation persistently comes in lower than the target.

The risk is that, by then, a lot of additional economic damage might have been done.

0 comments:

Publicar un comentario