The Fed's Last Waltz

Sep 19 2013, 07:11

It's my usual practice in these market notes to write first about the longer-term implications of recent events, then close with the short-term Outlook. This week I will do the reverse, perhaps in homage to the spirit of yesterday's Fed decision.

Let me say first that I am relieved to have done very little in terms of portfolio adjustments ahead of the FOMC meeting - I espoused a policy of "staying in the middle lane" and stuck to it. As I've been writing recently, guessing policy decisions is a dangerous game, and I for one have learned the hard way to keep my hands away from the stove when it comes to forecasting Fed Chairman Ben Bernanke's decisions. Having concluded over a month ago that the most sensible way to proceed was for a $10 billion cut, as did most of the investment world, I immediately began to harbor doubts Mr. Bernanke would do it. It's gotten to that point for me.The short-squeeze that followed the announcement left the market overbought and traders fuming, and I can't say that I blame them. But the stock market is now as overbought as it was in May, when a 100-point move in the S&P 500 in the space of one month alarmed the FOMC and Chairman Ben into first bringing up the subject of a taper. We're now just shy of a 100-point move off the August bottom in only three weeks, and with Mr. B having just said no taper, I'm not sure what the Fed will do next. Neither is the central bank, apparently.

If history is any guide, the market will probably move up a bit more over the remainder of the week. The day after a market-friendly Fed decision usually sees a continuation move (though it sometimes fizzles by lunchtime), and the third-quarter triple-witching due Friday has been unusually good for stocks in the past. That should help equities.

Working against that are reasons I started taking profits before the close and plan to take more over those same two days. As I've already said, the market is badly overbought. Add on to that the history of the week after September's triple-witch being unfavorable for stocks right through the end of the month. Not every day certainly, but weak overall. A third reason is that once the sheen of the Fed decision wears off, a certain budget battle is going to finally get the market's attention. I don't think the early view is going to be encouraging.

That's the short-term (very short-term) outlook, but what happens after that is clouded, to say the least. Traders are one thing, but the reaction of many others showed a distinct lack of embrace for the Fed's move. CNBC's normally unflappable Steve Liesman confessed himself to be left utterly at sea, a reaction shared by many, while long-term bull (and CEO) Larry Fink of Blackrock was clearly skeptical, worrying about what will happen when the Fed is buying 100% and more of monthly Treasury issuance. It will soon be the case. As for the ever-optimistic David Kelly of JP Morgan, he was positively (and very unusually) irate.

It would be rash to dismiss these reactions as the self-serving tantrums of so many underweight investors; I'd be very surprised to learn that Kelly or Fink are underweight. There are indeed some perplexing aspects to the whole thing. If downside risks have eased, as the Fed claims to be the case, then why is it continuing its utterly unprecedented policy of extraordinary accommodation? Or as Mr. Kelly fumed, with stock prices at record highs, employment at five-year highs, and GDP at all-time highs?

There's also something a bit odd - isn't there - about the storyline, "Fed cuts outlook again, says economy still fragile, stocks roar to new records." It also brings up the conundrum that many were gnawing over in the aftermath, and directly addressed by one questioner at the press conference - if the mere discussion of the taper resulted in too much tightening (as Mr. Bernanke declared), then how can the Fed ever exit its purchases?

I felt neither outrage nor surprise at the Fed's decision, as Bernanke has always been a bit more dovish than the general consensus. But watching the press conference, I also wondered who else besides myself felt a certain uncomfortable sense of unreality about the whole thing. The Fed chairman was blithely dismissive of the notion that there might be any exit problems down the road from its already-massive and steadily growing balance sheet.

Really? I had a brief flashback to six years ago and seeing him with a calm smile repeatedly reassuring questioners that the subprime mortgage problem "appears to be contained."

The prospect of the very dovish Dr. Yellen's succession now seems less sanguine to me, and Rick Santelli's sardonic observation that Larry Summers was the smartest guy of the week for in effect not wanting to take the poisoned chalice may prove to be right.

The current longer-term overbought levels of the market are disturbing, resonating with 2007 and the beginning of 1999. We haven't quite surpassed either of them, which worries me even more, for it very definitely raises the prospect that we have room to go on the upside - and if so, the chances for yet another sharp, painful crash.

Mr. Bernanke also said that the Fed had to act independent of what market reaction might be. That has manifestly not been the case ever since Lehman, and it bothered me that he also said in the same conversation that the Fed would stand pat because rates had overshot - or in other words, because of the market's reaction.

I suppose that he meant the stock market in the first instance and the bond market in the second, but besides the fact the two are intricately linked, it simply has not been true during his tenure.

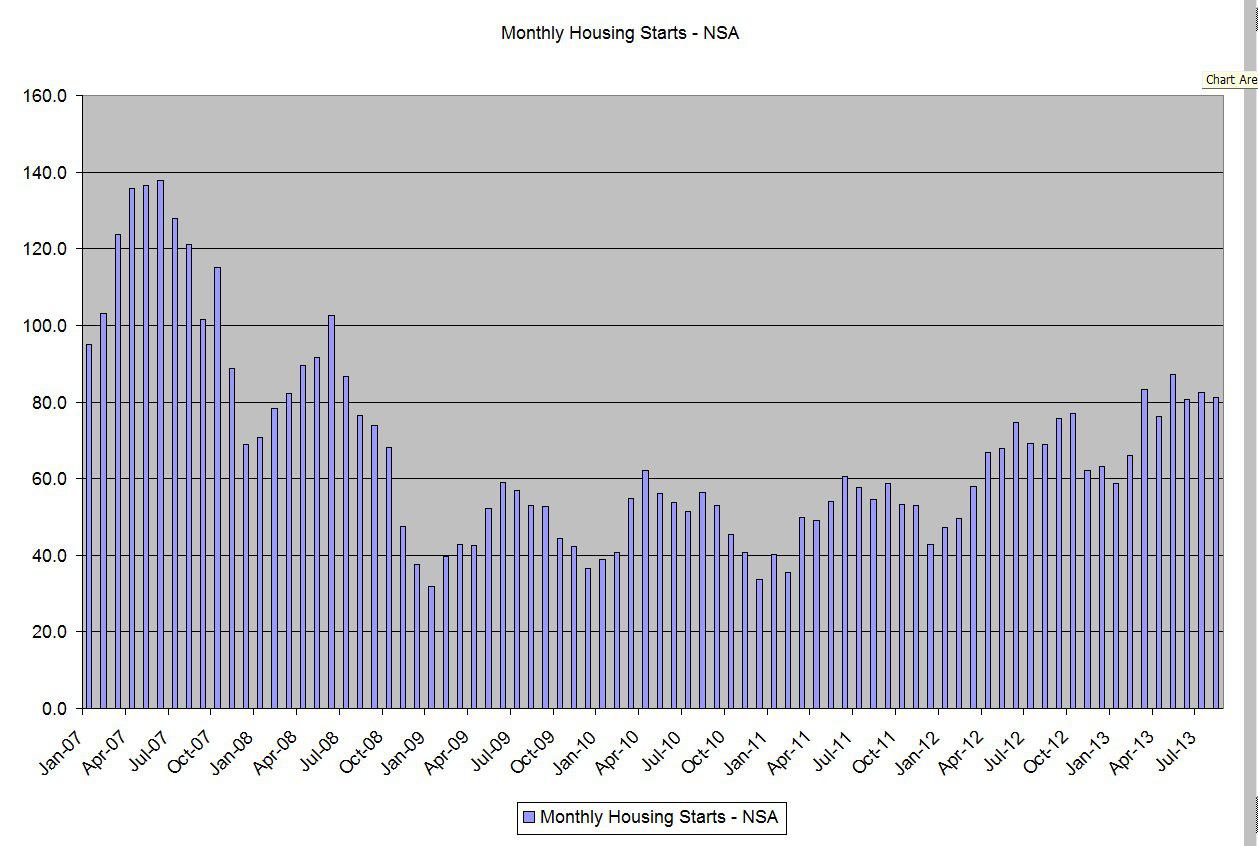

This week's chart is based on the latest batch of U.S. housing starts:

.

(Click to enlarge)

The growth has leveled off, as you can see, and the 30% year-on-year growth of the first quarter has fallen to under 23%. Yet having followed the homebuilders reasonably closely during the year, I don't consider this to be alarming. They've been saying for months that the early growth rates wouldn't last, that they wouldn't sacrifice profits for sales growth. It seems to me that they may now have reached their own comfortable glide path. Auto sales have clearly not suffered from the backup in rates; in fact, it isn't clear who has, apart from existing bondholders.

A look at some unintended consequences before moving on: What might now happen with the price of oil, and the budget battle. The original taper discussion weakened oil and gold and strengthened the dollar. Now it's going to be the opposite - sell the dollar, buy oil and gold. Rising oil prices aren't going to help the economy and by extension, the Fed's goal.

As for the budget battle, I return to my mantra of not guessing policy decisions - I bought into the extremity of Republican rhetoric at the end of last year and erred by predicting an impasse that never came to be. Granted that both sides seem somewhat more intractable now, I will not join either side, neither those who shrug wearily and say not to worry about yet another charade, nor those who again say it's time to start preparing for Armageddon. It's a hurdle to be crossed and I will probably head for the middle again and wait.

In rejoinder to the many who speculate that the FOMC canceled the taper as insurance for what could turn out to be an economy-bruising budget and debt battle, I say this - if the Fed really wanted fiscal action, it should have gone in the other direction and engineered an outsized taper. If the last decade has demonstrated anything, it's that rising financial markets are the nemesis of difficult political decisions. Had the S&P fallen over 5% by the end of this month, the pressure might have been on to settle; as it stands, an S&P over 1700 by month-end isn't going to encourage movement on either side.

All of that said, my long-standing prediction for an October top remains very much within the realm of possibility. If the politicians do manage to pull off another iteration of their pantomime of outraged bluster and last-second compromise, it would lift equities to new highs - probably just before third quarter earnings took them down again. I don't really find the prospect comforting, though. Good markets rise on earnings. Crazy ones rise because everybody knows they will - until they don't. It feels like Chuck Prince time again, doesn't it. So long as the music plays, we're all going to dance.

0 comments:

Publicar un comentario