The True All-In Cost To Mine Gold: Complete 2012 Figures

Apr 17 2013, 07:27

by: Hebba Investments

.

Over the last few months we have been analyzing and posting the gold industry's true all-in costs for each mined ounce of gold. We have analyzed almost all of the major publicly traded gold producers, with a total production of over 25 million ounces (around 800 tonnes) of gold for 2012.

According to the USGS, the world mined an estimated 2700 tonnes of gold in 2012, so the results of this analysis incorporates 30% of total 2012 gold production. Although we have our doubts about the accuracy of the USGS estimate, we believe our numbers represent a large enough portion of mined production to extrapolate as a general figure across the industry.

Why These Costs Are ImportantAccording to the USGS, the world mined an estimated 2700 tonnes of gold in 2012, so the results of this analysis incorporates 30% of total 2012 gold production. Although we have our doubts about the accuracy of the USGS estimate, we believe our numbers represent a large enough portion of mined production to extrapolate as a general figure across the industry.

For gold equity investors, understanding these costs are important because it gives insight into how much the industry spends to produce each ounce of gold versus a specific company. This allows investors to compare a specific company to the industry as a whole and benchmark its performance.

For gold ETF investors (GLD, SGOL, GTU, and PHYS) this metric may be even more important because it allows an inside understanding of the true costs associated with producing each new ounce of gold.

This is arguably the most important metric in analyzing any commodity because it shows the price where production of that commodity becomes uneconomic, which provides a very strong long-term floor for the price of the commodity. If it costs more to mine a commodity than the market is willing to pay for it, eventually producers will stop producing the commodity and close up shop. This does not mean that the price of gold cannot fall below the cost of production; it means that it would be unsustainable for it to stay there for long periods of time.

Some investors argue that above-ground stocks of gold are much greater than mined production and so any analysis of production costs is irrelevant. While it is true that above-ground stocks dwarf mined production, this argument stems from a lack of understanding about marginal supply in the gold industry.

We hope to release an article in the future that will address this issue in-depth since it deserves more than a paragraph, but in a nutshell mined gold supply from gold miners can be regarded as gold in the "weakest of hands" - they are the most marginal sellers. Gold miners produce gold and sell that gold on the market at the spot price because they have to use the money to meet their production costs.

If gold miners reduce production, then day-to-day demand must be met from other sources that are much more sensitive to prices. The buyers who ordinarily find the 2700 tonnes a year of mine supply to meet their demand will have to make due with 2200, or 2000, and so forth. This differential will have to be made from existing holders of gold, who care much more about prices, and as gold drops they will be less willing to sell at a loss or marginal profit. This supply is not available to the market at any spot price and these sellers would wait for higher prices - which ultimately would significantly constrict supply.

There is more to discuss about this concept, but that will be for a future article. Investors and analysts should note that miners provide the gold market with supply that sells at the market price; without them other sellers who are much more price-oriented would need to make up this supply and buyers would have to offer them a higher price to induce them to sell.

The Industry's Current Calculations Underestimate True Costs of Production

Before we go into the methodology we use to calculate gold costs, it is important to give an understanding to investors why the current "cash cost" calculations are incorrect and give investors a skewed picture of gold costs.

Publicly traded gold companies offer investors a quick non-GAAP formula to give investors a glimpse at their costs per ounce called "cash costs." This measure may vary slightly from company to company (it is non-GAAP after all) but it is generally their "mining costs" (cost to operate their mines, process the ore, pay miners, etc.) divided by the amount of gold equivalent ounces produced.

But unfortunately this measure is misleading, and selectively reports some costs and ignores other, which ends up not giving investors a true picture into the cost it takes to produce an ounce of gold. We are not the only ones to criticize the industry over this, and many investors and funds are also calling for improvements to these measures. Some miners have begun to offer a new measure of costs called the "all-in sustaining cash costs," which includes additional costs used to mine the commodity.

This measure is an improvement on "cash costs" and tends to be significantly higher, but it still does not accurately reflect the cost it takes to mine an ounce of gold. The reason that we do not believe this is an accurate measure is because it usually does not include any costs associated with discovery, the expansion of reserves, or expenditures related to operating sites, which are deemed expansionary in nature.

Simply put, it is all costs related to running existing operations with the goal of never expanding reserves or making any discoveries on new or existing properties. We do not feel like this is an appropriate measure because any mining company NEEDS to expand or maintain its reserves to survive, which is a very real cost of doing business in the mining industry. Investors should not be primarily interested in the costs it takes to sustain a mine, but rather the costs it takes to sustain a mining company. That is why costs related to the expansion of reserves should be included in the estimated cost of producing an ounce of gold.

Finally, the measure does not include financing charges (interest paid on existing debt) or taxes. These also are costs associated with the production of gold and any company who does not pay its interest or taxes will not be in business for very long, thus they should also be included in the calculated production costs.

Calculating the True Mining Cost of Gold - Our Methodology

To calculate the true costs to mine each ounce of gold, we use the total costs reported for the quarter (revenues minus net income before taxes) and then we add taxes to come up with total costs. Finally, we remove gains/losses on derivatives and gains/losses on extraordinary investments, since these really have nothing to do with running and sustaining the company.

Then we calculate the number of gold-equivalent ounces produced by converting all by-product metals (such as silver, copper, zinc, etc) into gold by dividing the gold price by the price of the by-product. For example, if gold is trading at $1650 and silver $30, then every 55 ounces of silver would convert into one gold-equivalent ounce. We like using the average LBMA cost for the reporting quarter or year.

Finally, when doing year-over-year comparisons, we use the same conversion ratio even if the price of the byproduct was different in the different quarter. The reason we do this is because this allows an even comparison when determining the cost of production - we do not want one quarter's jump in copper prices to affect a year-over-year comparison in gold prices.

The final thing that we have to deal with is write-downs. Most silver and gold companies report write-downs from time to time, which can add significant costs to a particular quarter or year. An argument can be made that write-downs are very real costs associated to the loss of investment on a property or mine and should be included in the cost calculations. For our calculations we do not include write-downs, though we do provide the cost of production with write-downs included so that investors can compare.

One thing to note is that if we remove derivatives and write-downs, we also have to remove the associated taxes from our calculations (usually write-downs involve tax benefits so they artificially lower taxes). There is no exact way to do this so we just use a flat 30% tax rate and deduct the appropriate amount from the tax benefit (or charge) that the company received from the write-down or derivative. Not perfect but it does do the job.

What are the Industry's Gold Costs?

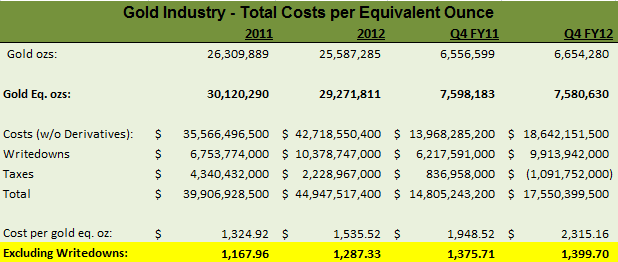

We have compiled all the numbers for gold companies we analyze for 2011 and 2012 and provided them in the table below. The companies included (with links to their associated detailed calculation pages) are: Barrick Gold (ABX), Goldcorp (GG), Yamana Gold (AUY), Newmont Mining (NEM), Agnico-Eagle (AEM), Eldorado Gold (EGO), Gold Fields (GFI), Allied Nevada Gold (ANV), Randgold (GOLD), Alamos Gold (AGI), Kinross Gold (KGC), and Iamgold (IAG).

For our gold equivalent calculations, we standardized the equivalent ounce conversion to use the average LBMA price for Q4FY12. This results in a silver ratio of 1:52.7, a copper ratio of 480:1 (pounds to gold ounces), a lead ratio of 1722:1 (pounds to gold ounces), and a zinc ratio of 1957:1 (pounds to gold ounces). We like to be precise, but minor changes in these ratios have little impact on the total average price - investors can use whatever ratios they feel most appropriately represents the correct by-product conversion.

.

(Click to enlarge)

Note about taxes: Taxes vary significantly on a quarter to quarter basis, and in the fourth quarter of 2012 the negative taxation value was due to significant write-downs by ABX and KGC, which resulted in a total negative tax rate for the quarter.

Let us first discuss the annual figures and then we will go over the fourth quarter figures. The first thing gold investors should note is that the true all-in costs to produce an ounce of gold (excluding write-downs) was $1287 for 2012, which is around a 10% increase in costs over 2011. The true gold cost of $1287 is much higher than the reported "cash costs" (under $1000 for most miners) and gives gold miners very limited profit at current gold prices ($1400 per ounce as of the publishing of this article). This gives investors a much better picture that aligns with gold miner share prices and earnings, which have both been dropping - when considering margin pressures this makes sense.

Not only are rising gold costs giving miners very slim margins, but they are also still rising (10% year-over-year) which shows how tough of an environment it currently is for miners. In our opinion, this cost pressure is related to the true inflation rate (much higher than the government CPI) and that is why we expect cost pressures to continue into 2013 and slim margins even further without a significant rise in the gold price.

Additionally, investors should notice that production of gold is actually dropping. In 2012 25.6 million ounces of gold were mined compared to 26.3 million in 2011, a 3% drop in production. Even as miners are experiencing higher costs the amount of gold production is dropping, which means that gold is becoming much harder to find and more expensive to mine. Investors should pay close attention to the upcoming quarter's production numbers, but with a dropping gold price and most miners predicting higher costs, we do not see a reason why gold production would increase.

Fourth quarter numbers also seem to indicate that production costs are still rising for miners as they come close to $1400 per ounce in 4QFY12. Though this does not necessarily mean FY13 costs will be close to $1400, fourth quarter's costs were higher and production numbers were down on a year-over-year basis. More proof that we can expect gold production to be dropping in 2013 - which is bullish for gold and GLD investors.

There is much more for investors to gain from the analysis of these numbers (including write-down costs, which put many miners well into the red) which we will offer in the second part of this series.

Conclusion and Investor Takeaways

Using this information offers investors a number of valuable takeaways. For investors in the gold ETFs (GLD, SGOL, PHYS, and CEF), the true cost of gold production continues to rise. This environment makes it very difficult for miners and gold mining investors, but it is actually very bullish for gold investors. As the costs to produce each ounce of gold rise, less gold will be produced and thus less supply will come on to the market. We are already witnessing signs of this in production numbers as miners produced less gold in 2012 than in 2011, and we see no reason why production numbers will not drop in 2013 with gold prices being so low.

Gold mining investors should be very cautious about which miners to invest their money in. It will be a very ugly environment for gold miners until the gold price recovers, and some face significant liquidity pressures and we expect mine closures if gold stays below $1400 for very long. Look for miners that have low cost structures and have a lot of cash on their balance sheets, which can help them weather this storm. Avoid miners that have high production cost structures, low cash, and high debt - these are the types of companies that will struggle to survive.

Gold and gold ETF investors should be accumulating gold aggressively at these levels because the production cost of gold is at or above the spot price. This significantly limits the downside risk for gold - it may fall to the $1200's due to aggressive short-term trading, but it is not sustainably produced at these levels. Analysts calling for gold to fall below $1000 per ounce on a longer-term basis simply do not understand the industry and its cost structure. At those levels only a small percentage of gold mining is profitable and many mines would be shuttered and projects cut.

We believe the current gold price smash offers investors a terrific opportunity to buy gold at a great value. None of the factors that led to the rise in the price of gold have changed (accommodative monetary policy, European financial risk, and a change in reserve currency status of the dollar) and much of this is evidenced in physical sales still being very strong. We encourage all investors to accumulate gold at these levels, and we would strongly advise investors to also own some physical gold to diversify their gold holdings.

More conservative investors may look to buy gold at the $1200 level, which is below the production cost level, but we do not believe it will fall this far. Hold tight gold investors and have confidence that the supply picture is significantly in your favor - we do not believe gold will stay at these levels for very long.

0 comments:

Publicar un comentario