April 15, 2012 9:13 pm

.

Global taxation: Fiscal frustrations

.

By Megan Murphy and Jeff Gerth

.

A clampdown on a tax structure used by banks will test US efforts to curb cross-border schemes

.

©Corbis

©Corbis

Developed in the boom years by a Barclays group led by Roger Jenkins and Iain Abrahams, Stars was sold to institutions including Bank of New York

.

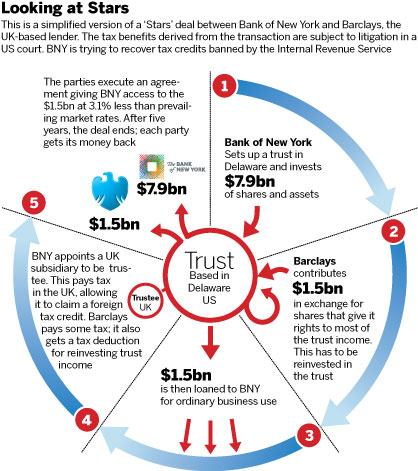

In November 2001, Bank of New York, a mid-tier US bank, transferred nearly $8bn of its own assets to a trust in the small, business-friendly state of Delaware through several layers of newly created companies.

A mixture of home mortgages, shares and other securities, the transfer made up almost 10 per cent of the bank’s total assets of $80bn at the time. In spite of its size, the transaction did not need to be discussed with BNY’s regulators, nor was it noted in the bank’s financial statements or annual report. It had little practical effect on the lender’s day-to-day operations – the assets continued to be managed and serviced by the same group of employees in New York.

.

.

Click to enlarge

But it was a critical first step in setting up a complex structure known as Stars – structured trust advantaged repackaged securities, to give its full, tongue-twisting name – which US tax authorities claim was used by several American banks as an abusive tax shelter that has cost them more than $1bn in tax revenues in the past decade.

Today, BNY will square off against the Internal Revenue Service in US Tax Court convened in New York over Stars and the tax benefits the structure triggered for the US bank and UK-based Barclays, its counterparty in the deal. At issue is whether Stars was set up primarily to generate artificial foreign tax credits, as the IRS contends, or whether it was a legal way for BNY to obtain financing at rock-bottom rates.

The arguments heard this week will pose a crucial test of the US government’s resolve to rein in sophisticated corporate tax planning that has sapped vast amounts of potential revenue. Tax authorities worldwide – notably in the US and UK – are under mounting pressure to show that large companies are shouldering their share of the tax burden as part of a broader political debate about fairness and corporate social responsibility.

.

“We are upping our game in the large business area, particularly as it relates to international tax issues,” Douglas Shulman, US internal revenue commissioner, said in a speech in Washington this month.

For the IRS, losing the Stars disputes would be a serious blow to its strategy in high-value cases, tax lawyers said. For the banks, the risk is financial – $900m is at stake in the BNY case alone – as well as reputational.

An investigation last year by the Financial Times and ProPublica, a New York-based nonprofit investigative news organisation, first detailed how Stars produced tax benefits for US banks. In all, six banks – BNY (now Bank of New York Mellon), BB&T, Sovereign (now a unit of Santander), Wachovia (now part of Wells Fargo), Washington Mutual and Wells Fargo – participated in Stars deals with Barclays between 1999 and 2006. Five of those banks are now challenging IRS rulings that disallowed foreign tax credits generated in those transactions. WaMu has settled a dispute over its own Stars structure in bankruptcy court by agreeing to forgo $160m in claimed tax credits. In total, the IRS says, the Stars deals created $3.4bn in foreign tax credits.

Now, documents filed in BNY’s case in the past few weeks provide unprecedented detail about Stars and how the structure was crafted at a time when banks and accounting firms were offering deals for multinational corporations to take advantage of loopholes in foreign tax credit rules.

At the simplest level, foreign tax credits are designed to prevent US companies being taxed twice on income earned overseas by allowing them to claim credit for taxes paid in foreign jurisdictions.

In the BNY case, the IRS claims the Stars structure allowed both Barclays and BNY to claim credits for the same “illusory” foreign tax charges, ultimately reducing the US government’s tax revenue by $18.15 for every $100 of income funnelled through the Delaware trust. “The record will establish that Stars was a pricey financing that no prudent banker would undertake but for the tax benefits generated by the meaningless circulation of cash flows,” according to a court filing by the IRS on March 27.

.

BNY has argued in the case that the deal was complex but an entirely legal structure that allowed it access to low-cost financing from Barclays for its everyday business activities.

Like hundreds of other foreign tax-driven transactions sold to companies in the boom years before the financial crisis of 2008, Stars was developed by Barclays’ famed structured finance group, known as Structured Capital Markets. Led at the time by Roger Jenkins, one of Britain’s best-known dealmakers, and Iain Abrahams, the expert behind most of the bank’s tax arbitrage transactions, SCM’s original concept was for Stars to manufacture tax credits for Barclays and a US corporate taxpayer by circulating US income through an entity taxed in the UK, the IRS said in its filing.

Because of the differences between US and UK tax rules, Stars would allow Barclays to reimburse a US taxpayer for half the tax paid in the UK without reducing the amount of foreign tax credits that could be claimed by either party, the IRS said. Barclays is not a party to the IRS dispute with BNY and has not been accused of wrongdoing by the US authorities.

According to the IRS, blue-chip US companies, including software company Microsoft and insurers AIG and Prudential Life, turned down early versions of Stars for unspecified reasons. The IRS said BNY, which bought the deal in 2001, had grown “addicted” to tax-driven transactions, which provided it with an important source of revenue.

Before buying Stars, the IRS says, BNY had entered into more than 100 “lease-back” transactions – known as Lilos and Silos – that produced tax advantages. Shortly after participating in Stars, BNY also purchased from Barclays another foreign tax credit structure, nicknamed Toga, that involved high-grade debt securities, the IRS said.

“Barclays understood that BNY was highly receptive to a wide range of tax-based ideas, and had targeted BNY for an SCM ‘tax product’ after discussions with BNY senior executives,” the IRS said in its filing.

The IRS also described KPMG as a pivotal player to the deal. The accounting firm provided a US tax opinion blessing the structure for Barclays and sold Stars to BNY for a fee of $6m, according to the IRS filing.

David Brockway, then of KPMG, was engaged to provide the firm’s opinion on Stars and is expected to testify at trial, according to the IRS. Mr Brockway, a leading US tax lawyer, left KPMG in April 2005 amid scrutiny of the firm’s previous sales of potentially abusive tax shelters.

.

Raymond Ruble, formerly a partner at Sidley Austin in New York, is another lawyer named by the IRS as a key adviser on the structure. Convicted of multiple counts of tax evasion in a separate tax shelter case involving wealthy taxpayers in 2008, he is incarcerated in a federal prison in Lewisburg, Pennsylvania.

The IRS, Barclays, BNY, KPMG and Sidley Austin declined to comment on the case before trial. Mr Jenkins, now a partner at Brazilian bank BTG Pactual, and Mr Abrahams, still a senior executive at Barclays in London, each declined to comment. Mr Brockway, now a Washington-based partner at law firm Bingham, did not respond to requests for comment.

Both sides acknowledge that BNY’s Stars deal was executed through highly choreographed steps. First, BNY transferred about $7.9bn of income-producing assets to the Delaware trust through layers of newly created subsidiaries. Barclays, as the counterparty, acquired shares in the trust, giving it a right to nearly all the income generated by the assets. In return, Barclays contributed a $1.5bn loan to BNY, also via the trust.

Barclays and BNY then executed a repurchase agreement, or “repo”, under which BNY agreed to buy back the shares in the Delaware trust five years later, in November 2006. BNY appointed a UK company as trustee of the Delaware trust, making the income it produced subject to UK tax.

At the outset of the deal, the trust’s pool of assets were expected to generate about $460m of income a year – of which, at a tax rate of 22 per cent, $100m would be paid to UK tax authorities. When the trust income failed to reach $460m, as expected, BNY injected extra assets, essentially to top up the income stream.

At the heart of the structure are differences between how it is treated under US and UK tax law. Under UK rules, Barclays was allowed to take a deduction against its other taxable income in the UK on the condition that it immediately reinvested the income produced by the assets in the trust. But it was also able simultaneously to take a credit for the tax paid by the trust.

According to the IRS, those tax benefits were shared with BNY, generating gains for both banks. For every $100 of income circulated through the trust, the US government lost $18.15, which financed BNY’s profit of $7.15, Barclays’ profit of $7.70 and UK tax receipts of $3.30, the IRS claims.

But under US tax law, the deal was considered a secured lending arrangement. So under US tax rules, BNY, as owner of the UK trust, could also claim a foreign tax credit for the UK taxes paid.

.

In 2001 and 2002, BNY claimed nearly $200m foreign tax credits from the Stars structure, which the IRS has disallowed. Including interest, the total amount in dispute is about $900m, according to the bank’s most recent annual report.

“The foreign tax credits that Bank of New York claimed in the US at a 22 per cent rate were far more than the actual UK tax attributable to Stars,” the IRS says in its filing. “In other words, Bank of New York claimed credits for phantom UK tax expense.”

BNY, by contrast, which is challenging the IRS’s refusal to allow the credits, says it entered into the Stars deal to borrow low-cost funds. Because of the UK tax benefits the structure generated for Barclays, BNY claims the British bank was able to provide it with the five-year $1.5bn loan at a cost that was more than three percentage points below the prevailing benchmark lending rate.

“The complication was required by Barclays’ UK tax objectives, not by BNY,” the bank said in a court filing on March 27. “By lending to [BNY] through the structure that Barclays designed, Barclays could offer a very favourable borrowing rate.”

In the coming weeks, US Tax Court will hear from the bankers, lawyers and accountants involved as well as a raft of experts in weighing up both sides’ positions. A final decision is not expected for more than a year.

With much at stake, BNY and the IRS appear to be digging in for a protracted battle. In its latest filing, BNY accuses the government of using “emotionally laden” arguments to try to deliver a “sweet sound bite”. The IRS, for its part, says “no rational person” would have participated in Stars if it did not generate foreign tax credits.

.

Let the war of words begin.

.

Authorities call for joint action – but collaboration has its limits

.

The threat posed by cross-border tax schemes has emerged as one of the biggest problems facing fiscal authorities. “Aggressive tax planning – untaxed income, multiple deductions and other forms of international tax arbitrage – is a growing concern for all governments,” the OECD said last month as it launched a study into ways to tackle the problem.

The Paris-based think-tank called for action on “international loopholes” that put billions of dollars at risk, citing recent cases involving New Zealand and Italy, as well as the foreign tax credit transactions that are the subject of court battles in the US.

The same issue is worrying the European Commission, which recently launched a fact-finding mission into the “undesirable” competitive advantage achieved by companies able to exploit differences in the tax rules of two countries. It is considering proposals for better information sharing and new laws to eradicate mismatches.

Since the 1980s there have been attempts to legislate against cross-border schemes, with mixed results. Information sharing has become more widespread, even though it may require governments to expose schemes that harm other exchequers but benefit their own.

In the case of Bank of New York’s legal battle over the tax credit transactions known as Stars, the US tax authority’s trial memorandum says Barclays convinced the UK Revenue to respect its tax position in the deals, which benefited Britain. “The UK collected more tax with Stars than without Stars,” the filing says. Even so, the UK then joined forces with the US, Australia and Canada in 2004 in a taskforce that set out to unravel these and other cross-border schemes.

But international co-operation has its limits. The most effective reform – harmonising tax rules to eliminate arbitrage opportunities – is unrealistic, according to the OECD. The best bet are specific laws on cross-border schemes. The OECD notes that Italy, the UK and the US have introduced rules for schemes whose purpose is to manufacture foreign tax credits. Canada is also looking at such rules even though – like the US – it believes its general anti-avoidance rule should work against the schemes.

This desire for a back-up plan is a sign of the huge sums at stake. As the OECD puts it: “The magnitude of the problem warranted greater assurance.”

.

Jeff Gerth is a senior reporter at ProPublica

Copyright The Financial Times Limited 2012.

0 comments:

Publicar un comentario