by: Marvin Bolt

August 15, 2010

Since 1971 the US dollar has held a privileged position in the global economy, contributing to major imbalances between trading partners. American consumption of foreign goods and services has caused record US trade and budget deficits, and accelerated the export of dollars overseas. The resulting imbalances reached excessive levels in 2001, when the impact on the dollar exchange rate first started to become apparent.

In a series of charts, we illustrate correlations between the US currency and a variety of fundamental factors. Our objective is to investigate relationships between the dollar and,

•net foreign direct investment;

•the trade deficit;

•crude oil prices;

•federal budget deficit;

•allocation of currency reserves by foreign central banks;

•gold prices;

•short-term interest rates; and

•technical analysis of the DXY Dollar Index.

INTRODUCTION

Currency markets have a variety of influences that ebb and flow over time. Consider, for example, how a country’s growing trade imbalance might be the driving force behind its currency movements. The impact can last many years. In the interim, however, a sharp move in interest rates might change the trend for an intermediate period of time. All while short-term fluctuations, perhaps lasting only a few weeks, can stem purely from emotions, driven by news headlines: Will Greece default? Will China revalue? Has the currency moved too far, too fast?

The Current System – A Brief History

Seeds of the current environment were sown at the conclusion of World War II. In an effort to encourage world trade and rebuild economies ravaged by the war, 44 nations met at a conference held in Bretton Woods, New Hampshire in July of 1944. The original goals were well-intentioned. Led by the US, the world would create a fund to provide capital to underdeveloped nations. It was envisioned that countries with temporary trade deficits – lasting perhaps 1-5 years – would finance any resulting shortages in currency reserves by borrowing from the fund. Persistent trade imbalances would be managed through periodic exchange-rate adjustments. Otherwise, all currencies would be backed by gold and exchange rates would be fixed. These were the original concepts.

What eventually emerged from Bretton Woods was somewhat different. The US dollar became the word’s reserve currency. Institutions were formed to manage the new foreign investment and currency initiatives, leading to the creation of the International Monetary Fund (IMF) and IBRD (predecessor to the World Bank). But the new institutions were substantially funded, and therefore controlled, by the US government. Originally, all dollars were backed by gold but that link was severed when market forces took over. By 1971 the US had a severe shortage of gold and could only back one-fourth of the dollars in worldwide circulation. President Richard Nixon subsequently ended the direct convertibility of dollars into American-held gold. Within two years, most major currencies were no longer pegged at a fixed exchange rate to the dollar.

America’s motives after WWII were largely based on altruism and generosity, as demonstrated by the Marshall Plan to help rebuild Europe through grants instead of loans. The US also wanted to develop strong trading partners. But the evolution and eventual collapse of Bretton Woods arguably ended up benefitting the US government more than anyone else. It marked the beginning of the present period that some might consider “dollar imperialism”1. The US central bank has the unique ability to print dollars that are backed only by the full faith and credit of the US government, yet still accepted as a viable currency around the world.

____

1- According to some views (perhaps not mainstream) in the past 30+ years the US government has used its influence over the World Bank to facilitate unnecessarily large loans to developing countries in the name of infrastructure development1. Targeted nations were often considered important allies in the Cold War, or were rich in natural resources. The goals were to award development contracts to US multinational companies and, at the same time, create a level of indebtedness by the borrowing nations that exceeded their capacity to repay. Through such tactics, US officials could dictate terms of loan modifications, thereby giving the US tremendous leverage over the leaders of the targeted nations.

Another component of America’s perceived imperialistic tendencies has been control of the world’s reserve currency. If the US government borrows from foreign lenders but does not make repayment until some future date when the dollar exchange rate has depreciated and its purchasing power has eroded through inflation, then the US enjoys an economic benefit. In effect, the US extracts a tax from the world. While it may not be apparent to the public, it can be argued that US citizens have benefitted from relatively lower tax rates than would have otherwise been required for the same level of government services. In the long run, however, access to such easily available capital, through printing and/or borrowing dollars, has contributed to the growth of an inefficient and wasteful US government.

An eloquent quote2 from former US Secretary of State Henry Kissinger sums it all up quite succinctly,

(He) who controls the food supply controls the people; who controls the energy can control whole continents; who controls money can control the world.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170594336812-Marvin-Bolt_origin.jpg )

{kind=link}

With the power to issue debt and create money at will, it would have taken enormous discipline for government leaders to resist the temptation to abuse the privilege. Then again, at the heart of capitalism is fear and greed, not discipline and constraint. So, with the benefit of hindsight, it seems clear that we would eventually find ourselves where we are today, in a world where the US government has used the power of its printing press to create an enormous supply of US Treasury securities and dollars, perhaps to excess.

With the power to issue debt and create money at will, it would have taken enormous discipline for government leaders to resist the temptation to abuse the privilege. Then again, at the heart of capitalism is fear and greed, not discipline and constraint. So, with the benefit of hindsight, it seems clear that we would eventually find ourselves where we are today, in a world where the US government has used the power of its printing press to create an enormous supply of US Treasury securities and dollars, perhaps to excess.More recently, in an effort to provide fiscal and monetary stimulus in the wake of the global recession, US central bankers and Treasury officials are betting that the global appetite for Treasury bonds and dollars will remain firm. Low bond yields indicate that the appetite for US Treasuries has not wavered. In contrast, the value of the dollar has been trending lower since 2001.

FUNDAMENTAL FACTORS

The amount of government debt held abroad is a good proxy for the global imbalances that drive US currency movements. As illustrated in Figure 1, foreign ownership of US debt reached an inflection point in 1996 and has been rising steadily. Around the year 2000, as foreign ownership climbed past 35%, is when dollar price movements first started to become correlated with the value of gold, oil and the trade deficit. Today, slightly less than 50% of all federal debt outstanding is held by non-US investors.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170597670451-Marvin-Bolt_origin.jpg )

{kind=link}

Foreign Direct Investment

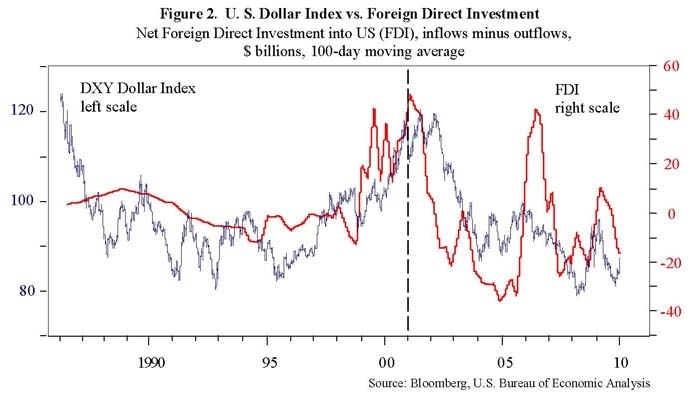

Figure 2 shows a strong link between net Foreign Direct Investment (FDI) into the US and the DXY, Dollar Index. Generally, FDI consists of assets deployed as durable investments – when one country invests to build a factory in another country, for instance. Such an event can have an impact on the currency market. If, for example, a US manufacturer decides to build a plant in Mexico it requires an exchange from dollars to pesos to pay for local construction in Mexico. Consequently, net FDI flows out of the US should have a negative impact on the price of the dollar, and vice-versa, as can be seen in Figure 2.

With all of the relationships we consider in this paper, it is important to be aware that a mutual cause and effect might exist. Does a rise in net FDI lead to a rising dollar? Conceptually, the answer would be yes. However, a rise in the dollar could also be a sign of improving economic fundamentals, which attracts foreign investments into the US. From a statistician’s perspective, the economic fundamentals of the country would be considered a confounding variable, not accounted for when only the relationship between the dollar and FDI is considered. Without question, there exists confounding variables and statistical interactions among all the factors considered in this paper.

Fundamental factors discussed in this paper can impact the dollar in two ways: 1) fund flows directly impact the supply/demand balance of dollars traded in the foreign exchange market; and 2) psychology & perception influences how greedy or fearful buyers and sellers are. For example, the Chinese government’s perception of the stability of the US currency and economy will influence their willingness to continue to hold dollar-denominated securities. Alternatively, FDI or foreign trade would be examples where fund flows are the driving force; a currency exchange is required to facilitate an overriding purpose – maybe the purchase of a foreign car. Here, the perception of the safety of the dollar has little influence on the decision to buy or sell the currency.

The Dollar-Oil Relationship

It is easy to understand why financial flows based on direct investment or trade can require currency transactions, and therefore impact exchange rates. Reasons for the relationship between commodity prices and the dollar are not as obvious, but powerful nonetheless.

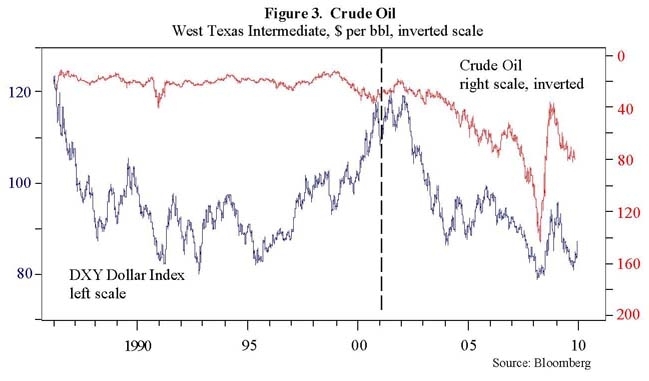

One of the consequences of the US dollar’s position as the world’s reserve currency is that important commodities, such as oil and gold, are priced in dollars. The stability of oil prices during the last two decades of the 20th century helped alleviate any concern about the lack of an explicit backing for the dollar. A one-hundred dollar bill could be exchanged for between 4-6 barrels of oil at any time during the period. Hence, oil served as an implicit backing to the dollar.

Furthermore, it appeared that America’s military and geopolitical stance vis-à-vis Saudi Arabia and the Middle East would ensure the stability of oil prices. But alas, market forces proved to be stronger than American influence, and with the arrival of China’s middle class came a surge in oil prices.

With this as a background we can explain why oil prices have developed a strong relationship with the dollar. Simply put, oil exporting countries have no desire to own additional dollars. Therefore, every $1 increase in the price of oil is one extra “petrodollar” that Iran or Venezuela does not want to hold in its reserves, so the marginal dollar received is sold in the currency market. Rising oil prices lead to a falling dollar.

To make matters worse, in 2006 Iran adopted a policy of not holding any dollars in reserves. In 2008 they launched the Iranian Oil Bourse – a petroleum exchange in which oil is traded in a basket of currencies that excludes the dollar. If Iran is successful in undermining the dollar’s status as the world’s reserve currency, it could reduce the incentive of other nations to hold dollars. As shown in Figure 4, a negative correlation has become apparent since 2001 (note the inverted oil scale).

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170600043926-Marvin-Bolt_origin.jpg )

{kind=link}

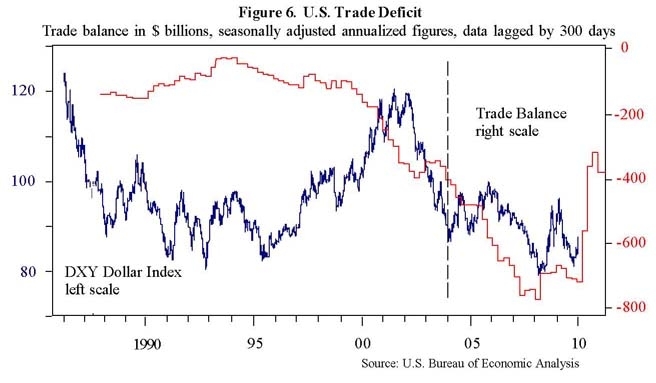

Trade and Budget Deficits

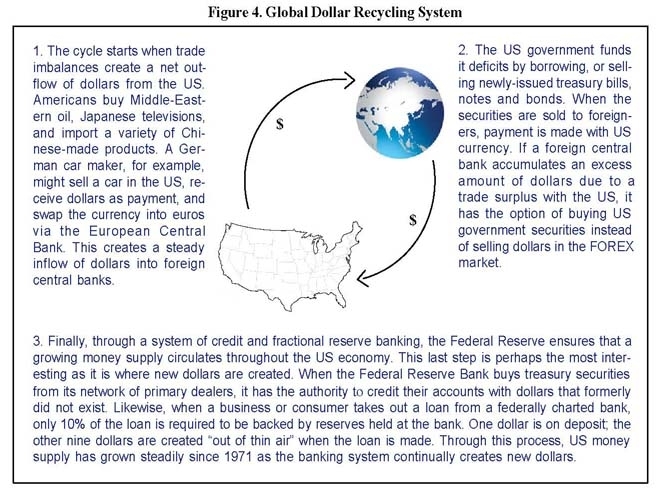

Since the dollar first started trading as a fiat currency in 1971, the US government has operated with a persistent budget deficit. In only one stretch, during the relatively brief 3-1/2 year period starting in 1998, did the federal government operate with a current account surplus. Otherwise, during the past 39 years, there has always been red ink. This highlights the challenge the US faces today in bringing its fiscal house in order. It also encourages us to ask why? Even in periods of prolonged economic stability and growth the US government has been unable to balance its budget. The answer lies in an understanding of the global dollar recycling system as detailed in Figure 4.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170602260851-Marvin-Bolt_origin.jpg )

{kind=link}

A primary cause of America’s twin deficits appears to come from excessive consumption. Over the past several years, until the beginning of the 2008 recession, consumer credit had become increasingly available, primarily through auto loans, mortgage lending, and credit card issuers. A generation of consumers embraced the “buy now, pay later” or “shop ‘till you drop” lifestyle. The US consumer has therefore been the driving force behind the country’s trade deficit. At the same time, China, Mexico, Japan and Germany — the top four trading partners (Table 2) — have eagerly supplied goods and services to America.

To ensure the stability of the currency, the US government needs a mechanism to influence how many dollars end up for sale in the FOREX market, especially with such large trade imbalances that effectively export dollars overseas. That mechanism is the sale of Treasury securities. As shown in Table 1 and Table 2, many of America’s biggest trading partners are also some of the largest foreign holders of US debt, which illustrates how effective the US government has been at swapping trade-related dollars for Treasury securities.

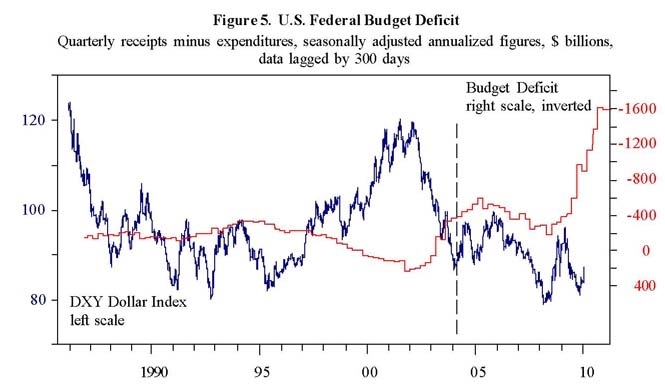

Under the global dollar recycling system, one would expect a rising trade deficit to create a weaker dollar. At the same time, a rising budget deficit creates the need to issue US Treasury securities - a process that siphons excess dollars from foreign central banks, creating a stronger dollar.2 Figures 5 and 6 show that since 2004, when the US trade deficit first surpassed $400 billion, these relationships have indeed existed.

_____

2 - Since 2008 a dramatic deterioration in the US government’s finances, and the exploding levels of government debt, have not led to a collapse in the dollar as might have been expected. Interestingly, a rising budget deficit can have both a positive and negative effect on the currency.

A growing debt burden can potentially undermine America’s debt rating and investor confidence in the currency. In contrast, the issuance of government debt reduces the supply of dollars available for sale in the foreign exchange market. So far the positive fund flows have outweighed the negative psychology. As long as foreign investors are willing to swap dollars for US Treasuries, the dollar does not collapse. One important conclusion is that a dramatic rise in Treasury-bond yields due to waning demand, and a continued rise in the trade deficit, would likely be a toxic combination for investors who are long the dollar.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170624570969-Marvin-Bolt_origin.jpg )

{kind=link}

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170626537902-Marvin-Bolt_origin.jpg )

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170626537902-Marvin-Bolt_origin.jpg ){kind=link}

In 2008, the global financial crisis slowed world trade substantially, as seen in Figure 6. The resulting shrinkage in the US trade deficit has begun to ease selling pressure on the dollar. However, as the world rebounds from the severe recession, world trade will also recover, which is likely to halt the recent improvement in the US trade balance. Furthermore, a distinction must be made between cyclical deficits and structural deficits. The structural trade deficit is more permanent. For example, consider China’s position as a low-wage manufacturer and major exporter to the US, or America’s consumption of imported foreign oil. Neither situation is likely to change very quickly.

As the US population ages, government obligations for social security and medicare will pressure the budget deficit for years to come. While some might think that the growing US debt burden will pressure the dollar, the best indication of America’s credit rating and ability to issue more debt is the yield for long-term Treasury bonds. As long as yields remain low, rising budget deficits should support the price of the US currency.

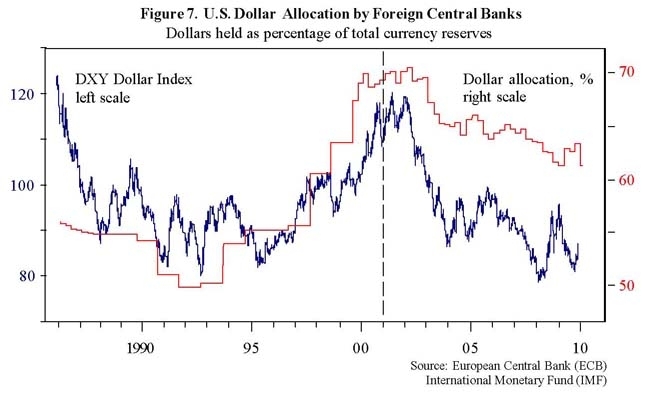

Dollar Allocation by Foreign Central Banks

Net exporting nations have a constant inflow of foreign currency. As shown in Figure 7, it appears that from 1993 until 2003 central banks around the world were satisfied with a steady increase in dollar allocation from their total currency reserves. By 2003 the dollar accounted for 70% of all reserves. However, with the increasing acceptance of the euro, central banks have been diversifying their holdings by selling dollars.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170628908512-Marvin-Bolt_origin.jpg )

{kind=link}

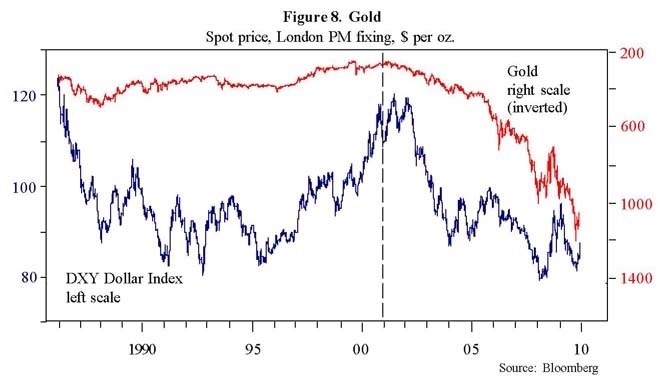

Gold

Two-thousand-and-three marked the year when central banks started reducing their allocation to the US currency. It is also the year when gold started a sustained rally. Coincidence? We think not. Gold’s history as a store of value (i.e. money) has persisted for thousands of years. Figure 8 shows that the relationship between gold and the dollar has strengthened in recent years. One reason is surely due to the diversification out of dollars and into gold. Indeed, the Chinese central bank has been rumored to be buying an excess of several commodities in recent years justified by the idea that, oil and copper for example, represent useful ways to allocate currency reserves into basic materials needed for future growth of China’s rapidly expanding economy. Like many of the fundamental factors discussed in this paper, the dollar-gold linkage has become more pronounced in recent years as the dollar-based global imbalances have worsened.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170630738754-Marvin-Bolt_origin.jpg )

{kind=link}

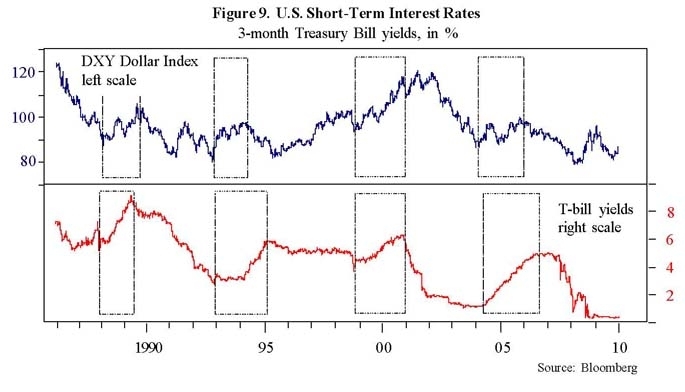

The Carry Trade

The Carry TradeProlonged periods of low or falling short-term interest rates encourage speculators to borrow funds in the country with low rates and invest the proceeds in assets expected to yield a higher rate of return in another country. When carry trades3 are funded by borrowing in the US, with the proceeds invested outside of the US, a currency exchange is required.

The dollar-based loan will be exchanged into the currency where the investment is made. Normally, carry trades are initiated by a variety of institutional investors over a prolonged period of time, so the impact from selling the dollar is muted. In contrast, the unwind of the trade tends to happen more rapidly.

Even though carry trades might be invested in a variety of ways, virtually everyone’s cost of carry is the same. Consequently, when the trade is unwound it tends to be due to rising short term interest rates and a rising dollar, causing many investors to close out positions at the same time. Closing the trade requires the repurchase of dollars to repay the loans, so a mass rush to exit can create a rally in the dollar.

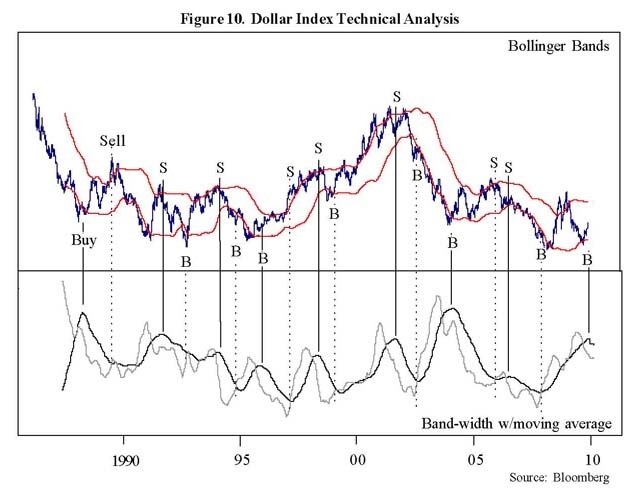

Four times in the past 25 years the US dollar has funded a carry traded. Figure 9 shows the impact of the unwind. In each period, as short-term interest rates rose there was an associated increase in the US currency. Markets have a way of discounting the future, and the carry trade is no different. At times, such as the 1993-95 period, the dollar rally started in anticipation of a rise in rates. At other times, the increase in the currency ended ahead of the peak in rates. This is where technical analysis can play a role. Figure 10 shows a series of buy/sell signals for the DXY Dollar Index resulting from the application of Bollinger Bands. Today it is interesting to note that, while a clear upturn in short-term rates has not yet occurred, investors using technical analysis to anticipate the unwinding of the carry trade will realize that the associated dollar rally appears to have already begun.

_____

3 - The term “carry trade” originates from the concept of the “cost of carry”. If an investment pays current income, such as a Treasury bill, it has a positive cost of carry. Commodities, for example, will typically have a negative cost of carry incurred from expenses related to storage of the asset. For a normal, positive sloping yield curve, short-term interest rates will offer the lowest yields. A carry trade is therefore typically funded by continuously rolling over short-term loans, with a low cost of carry, to invest in assets with relatively higher expected returns. When the cost of carry increases due to rising interest rates, or unfavorable movements in currency exchange rates, the carry trade will be unwound.

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170632563915-Marvin-Bolt_origin.jpg)

{kind=link}

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170634193499-Marvin-Bolt_origin.jpg )

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/8/13/483759-128170634193499-Marvin-Bolt_origin.jpg ){kind=link}

RECENT DEVELOPMENTS

Excess Reserves in the US Banking System

With great crises often comes great change. The global financial crisis of 2008 is likely to usher in significant changes in the investment environment. Clarity, however, is often only in hindsight. One area of interest for the US dollar is the future impact of the Federal Reserve’s enormous injection of liquidity into the US banking system. In the decade preceding 2008, excess reserves in the banking system averaged less than $2 billion. Starting in September 2008, the Fed began liquidity injections that grew to exceed $1 trillion after only 14 months. The primary justification was to maintain the solvency of the system after banks suffered tremendous losses from real estate and mortgage-backed securities. It remains to be seen how much of this liquidity will find its way into the economy through new business and consumer loans.

Recent Fed discussions of an exit strategy are focused on withdrawing the excess liquidity. However, there are reasons to believe that the unusually high levels might be more permanent. Consider how the history of credit and its funding sources have evolved. Prior to the Great Depression, economic activity and banking was local. Deposits were collected from local citizens and loans were made to local businesses. When a bank stumbled and came up short of reserves, deposits would flee causing a run on the bank. The development of a central bank eliminated this problem. Deposits were insured, removing the need for panic withdrawls, and the federal funds system was established. Subsequently, if a bank in one local community had a temporary shortfall in reserves it could borrow from a bank in another community and pay interest on the loan at a rate set by the Federal Reserve: the so-called Fed Funds Rate. By setting the Fed Funds Rate, the central bank could influence the level of economic activity and inflation. Low rates encourage borrowing between banks to facilitate consumer & business loans; a higher Fed Funds Rate slows lending activity.

The enormous levels of excess reserves in the system have rendered the Fed Funds Rate ineffective as tool to moderate lending. With banks holding so much excess liquidity, interbank lending is now less important. As a result, the Fed recently established a new lever to influence economic activity: interest paid on excess reserves is now the new benchmark rate. In 2008, the Federal Reserve started paying commercial banks interest on excess reserves the banks held on deposit with the Fed. In theory, if the economy is at risk of overheating, the Fed will be able to incentivize banks to reduce lending by increasing this rate, thereby allowing the banks to earn more income without assuming the risk that comes from issuing a loan. It remains to be seen how effective the Fed’s new benchmark will be in practice.

National Savings Rate

It is interesting to consider the source of credit for economic activity in the US. One hundred years ago, local deposits funded local loans. Forty years ago, deposits nationwide funded national lending. Today, the banking crisis has highlighted one consequence of the low national savings rate. With the onset of the banking crisis, additional US consumer deposits needed to bolster bank balance sheets were not available, so the government borrowed funds from oversees to inject liquidity into the banks. Now, international capital supports US lending. In addition to funding federal budget deficits, it appears that the world’s excess currency reserves could become an increasingly important source of capital needed to support US economic growth.

CONCLUSION

Bulls vs. Bears

Unprecedented actions by the Federal Reserve provide arguments for both dollar bulls and bears. A negative outcome could develop if the Fed is unable to prevent excess bank liquidity from making its way into the economy. A rapid increase in demand for loans might then lead to a surge in the money supply, debase the US currency, and create rampant inflation. In the bearish scenario, rising long-term interest rates and a waning foreign appetite for US government bonds will cause foreign central banks to sell their excess supply of dollars. China will continue its rapid growth driving the price of oil ever higher. Every dollar increase in the price of oil will be one more dollar earned by oil exporters, which will then be sold in the currency market. The role of the US dollar as the world’s reserve currency will continue to diminish; the currency might collapse.

The bullish argument depends on the world’s willingness to fund America’s need for capital by continued purchase of US Treasury securities. In this scenario, US debt instruments will remain attractive as an alternative to selling dollars in the FOREX market. China’s growth slows; global imbalances become more manageable. The recent positive trend in the US savings rate continues and the trade deficit narrows further; this would be positive for the dollar. Even if the US government makes progress towards balancing its budget, foreign reserves could become an important part of the monetary base of the US banking system, thereby draining dollars from the coffers of foreign central banks and supporting the dollar. These developments would favor dollar bulls.

REFERENCES

1.Confessions of an Economic Hit Man by John Perkins; 2004; amazon.com

2.Crisis of the US Dollar System by F. William Engdahl; October 2006; globalresearch.ca

3.The Fight for Honest Monetary Weights and Measures; six essays by Dr. Lawrence M. Parks; January, 2000; Foundation for the Advancement of Monetary Education (FAME); fame.org

4.U.S. Bureau of Economic Analysis; bea.gov

5.International Monetary Fund (IMF); imf.org

6.Federal Reserve Bank of St. Louis; research.stlouisfed.org

0 comments:

Publicar un comentario