by: Graham Summers

February 24, 2010

There are times in life when one witnesses something so outside the scope of normal experience, that at first you don’t see it.

Captain Cook’s diaries tell us that upon first seeing his ships offshore in Australia, the aborigines expressed “neither surprise nor concern.” Cook notes that it was not until he and his men approached the shore in smaller, more familiar vessels that the villagers reacted, arming themselves as “the sight of men in small boats was comprehensible to them: it meant invasion.”

Well, I had a similar experience during yesterday’s bond auction. Before going into the details, we need to fully explain how a Treasury Auction works.

First the Treasury issues a press release saying just how much debt is being issued (sold) during a given auction. This release also says how much of the Treasuries currently owned by the Federal Reserve are coming due that day, the implication being that the Fed will likely use the funds from their maturing Treasuries to buy some of the new debt issuance.

When it comes time for the auction, investors can either bid non-competitively (meaning they’ll take whatever yield is available based on demand) or competitively (meaning they have a minimum yield requirement and won’t buy the debt if it yields less). Non-compete bids are accepted first. After them comes the competitive bids until the total debt issuance is complete.

So let’s say the Treasury is issuing $10 billion in ten-year notes. On the day of the auction, the lowest competitive bid states it won’t accept anything under a 3% yield. So, the Treasury starts filling non-competitive bids at 3%. Once all the non-competes are filled, the Treasury starts filling the competitive bids in the order of increasing yields (so those competitive orders requiring a 3% yield are filled before those requiring a 3.5% yield) until the total debt issuance is met.

Once the Treasury auction is complete, the Treasury issues a press release stating the highest accepted yield and the amount of Treasuries sold to non-competitive bidders. The Treasury also reveals what percentage of competitive bids occurred with each of the three bidders. These are:

1) Primary Dealers: those banks/ financial institutions that trade directly with the Federal Reserve bank of NY (and so HAVE to buy Treasuries at auction)

2) Direct bidders: those investors who place their bids directly with the Treasury (also the easily track-able orders)

3) Indirect bidders: those investors who place their orders through direct bidders (untraceable orders or orders made by buyers that cannot be tracked)

I realize this sounds complicated. The main issues are that the Treasury issues debt. Some folks take it at whatever price they can. Some folks buy it only if it yields as much as they want.

The Treasury first sells the debt to those who don’t care what it yields (at the lowest yield the folks who DO care what it yields are willing to accept) and then issues the remaining debt to those who DO care what it yields first at the lowest yield accepted and then at higher yields.

Finally, of the folks who buy, some buy right from the Treasury (directs), others buy through intermediaries (indirects). And if there aren't enough of either, the Primary Dealers step in and buy the rest.

Ok, now onto yesterday’s auction.

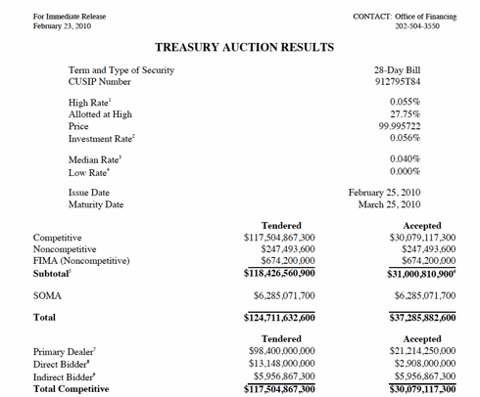

Yesterday the Treasury issued $37 billion worth of four-week notes (meaning debt that comes due in four weeks). The lowest yield accepted was 0.0000% (literally NO yield) and the highest yield accepted was 0.055% (virtually nothing).

(TO ENLARGE CLICK ON : http://static.seekingalpha.com/uploads/2010/2/24/saupload_4_week_thumb1.png

{kind=link}

Roughly, 27% of the auction took place at the highest rate. This means nearly one third of the demand from competitive bidders (those who care about yield) came at the HIGHEST yield that was accepted. In plain terms, this alone tells you that investors want higher yields from Treasuries since nearly a full third of the debt issuance took place at the highest REQUIRED yield.

As you would expect, there were few non-competitive bids (who in their right mind is willing to buy US debt without caring about the yield?): non-competes only made up less than 1% of the bids. In contrast competitive bids made up 97% of the demand.

Now here’s where things get odd.

Of the competitive bids (meaning those bids coming from folks who care about yield), roughly 70% went to Primary Dealers (investors who HAVE to buy the debt and who usually turn around and try to sell it afterwards). To put this number into perspective here is the percentage of competitive purchases made by Primary Dealers in the last four 4-week Treasury issuances:

Date of 4-Week Treasury Auction

Primary Dealers as % of Competitive Buys

January 5 2010

42%

January 12 2010

70%

January 20 2010

60%

January 26 2010

67%

February 2 2010

51%

February 9 2010

51%

February 17 2010

61%

February 23 2010 (yesterday)

70%

You’ll note that during the stock market correction that took place during the end of January/ beginning of February, Primary Dealers didn’t need to buy many Treasuries since investors were fleeing stocks and buying short-term Treasury debt as a safe haven.

You’ll also notice that yesterday’s auction featured MORE buys from Primary Dealers than almost any of those occurring in 2010. Remember, Primary Dealers HAVE to buy Treasuries. So to see them buying a high percentage of Treasuries at debt auctions means that few investors who can pick and choose what to buy are actually looking to buy US debt.

In plain terms, a debt auction that features a high percentage of competitive buys coming from Primary Dealers is BAD NEWS. It means investors generally aren’t buying US debt. It also means that foreign governments (those who have funded US debt auctions for decades) aren’t buying much anymore either.

So the fact we’ve have three short-term auctions in which more than two thirds of competitive buys came from Primary Dealers is worrisome to say the least.

Now here’s where it gets even worse.

Of the remaining competitive buys (about $8.86 billion), only 32% came from Direct Bidders or those who bought debt directly from the Treasury: orders that can easily be tracked. The other 68% ($5.9 billion) came from Indirect Bidders: folks who we cannot track.

Even more bizarre, only $5.9 billion in Indirect Bidder competitive buys were ACTUALLY OFFERED. So we had a 100% acceptance rate for Indirect Bidder competitive buys.

Let’s put this in perspective:

Date of 4-Week Treasury Auction

Indirect Bidder Acceptance Rate

January 5 2010

71%

January 12 2010

22%

January 20 2010

77%

January 26 2010

43%

February 2 2010

63%

February 9 2010

87%

February 17 2010

82%

February 23 2010 (yesterday)

100%

This means that the Treasury took up EVERY single cent of competitive bids coming from indirect buyers. Remember, indirect buyers are usually assumed to be foreign governments (even the Treasury website admits this).

If this was the case yesterday, then foreign governments barely bought much of anything in yesterday’s auction (only 19% of total debt issued). Moreover, it implies that Primary Dealers (those having to buy) had to gorge on the auction to make up for the fact that few if any foreign governments are interested in buying our debt anymore (including even short-term debt).

Or…

One could potentially argue that this indirect buying came from the Fed covertly buying under the guise of an indirect bidder (the Treasury recently changed the definition of what qualifies for an indirect bidder to make it more vague). It IS rather odd that every single cent of competitive bidding coming from indirect buyers was filled. It’s almost as if the indirect buyers knew precisely WHAT yield to accept… OR were simply trying to take up the slack in what was already a VERY weak auction.

I cannot tell you which of the above is true. Heck, neither of them could be and something completely different could be happening. But regardless, something very, VERY strange is going on in US debt auctions.

I wrote earlier this year that bonds, not stocks, would be the big story of 2010. We’re only into February and there are already some very unusual things happening on both the long (30 year) and the short (4 week) ends of the Treasury curve. And with the Fed’s Quantitative Easing Program scheduled to end in March, things are about to get a whole lot more interesting (barring of course an extension of the QE or QE 2.0).

Keep your eye on US Treasuries. Stocks, despite being so popular with investors are usually the LAST to get what’s coming down the pike. And investors just parked $30 billion for a month with Uncle Sam at virtually NO YIELD yesterday.

Put another way, someone(s) is/are willing to not make money just for the sake of insuring return OF capital (the US can always print money to return it) rather than any return ON capital.

0 comments:

Publicar un comentario